Carrot and stick

From the point of view of tax theory, says Sun Keh-nan, a fundamental function of any state is "concentrating the power of taxation." Also, finance theory emphasizes "deciding revenue based on expenditures"-the state should decide what public services and economic infrastructure it wants to provide, and then tax the population for this amount. But most citizens want the government to provide "free lunch," and any politician who proposes raising taxes is committing political suicide. For example, Margaret Thatcher, the Iron Lady of British politics, was brought down by her advocacy of the poll tax; George Bush lost his bid for reelection after breaking his "no new taxes" pledge; and the cabinet of former Japanese prime minister Ryutaro Hashimoto was undone after he proposed raising the business tax rate.

It is precisely because Sun Keh-nan knows that raising taxes is poison to voters that he expects the experts to be especially careful in drafting tax increase proposals. For example, broadening the tax base could be tied to a lower tax rate, or tax increases in some areas could be offset by tax reductions in others. You always have to use the carrot along with the stick so that citizens feel they have not been treated unfairly.

A case in point is the recently much-discussed question of whether the land value incremental tax (LVIT), which was cut in half provisionally a couple of years ago, will be restored to its former level.

Tsai Chi-yuan of the Institute for Social Science and Philosophy at the Academia Sinica relates that Taiwan's LVIT is from 40-60%, and that the longer a property is held, the higher the tax rate on it when it is sold. This encourages investors to unload properties as soon as possible after acquisition, which aggravates the tendency toward short-term speculation in the real estate market. Two years ago the government announced that it would halve the LVIT for two years in order to jump-start the sluggish property market. Today there are signs that the market is coming back, but the preferential tax policy is scheduled to expire next January. What to do?

If the original tax rate is restored, the market could be immediately suffocated. But if the preference is extended, people will suffer from the false impression that "whatever the government gives, it can never take away."

Therefore the best approach would be to undertake a coordinated reform of the LVIT and the land value tax, cutting the former from 60/50/40% to 40/30/20%, while raising the latter. This will cause a slight increase in the cost of holding property (because the land value tax is assessed annually), but sharply reduce taxes when it is bought and sold (because the LVIT is only paid at the time of sale).

That looks straightforward enough, but in fact the situation is still more complex. Tsai Chi-yuan, who served formerly as chief of the Bureau of Finance of Taoyuan County, says that while the LVIT is high on paper, there are many ruses to avoid it. Most county and city governments, trying to reduce the tax burden on their citizens, have always low-balled their assessments of property value (on which the tax is based), so that a piece of land really worth NT$2000 per ping is assessed at, say, NT$200. Another approach is based on the fact that transfer of farmland is not subject to the LVIT. So one hears from time to time of big corporations avoiding taxes by buying land using farmers' ID cards. The way to solve all these problems at once would be to reduce the LVIT, broaden the tax base, raise assessments, and raise the land value tax in one big package.

Frustratingly, given the total lack of cooperation between ruling and opposition parties in the legislature, amending the law is agonizingly slow, but the preferential rate period is fast nearing its end, so action is urgently needed. Lately, some executive branch officials have bruited the idea of first lowering the LVIT in isolation, and then figuring out the rest later. But what does this mean in practice?

"If you give away the carrot first," wonders Tsai Chi-yuan, "who is going to dare pick up the stick? They'll be lucky if they aren't beaten to a pulp by voters." The phenomenon of reducing all taxes that should be reduced, but never getting around to raising those taxes that should be raised, so prevalent in the last few years, really is morale-crushing for people like himself who have long been fighting for tax reform.

Paying the piper

Besides creating packages in which the tax base is broadened while tax rates are reduced, another key concept in tax reform is to transform the system from one in which direct taxes (mainly income tax) play the main role to one in which consumption taxes (mainly the value-added tax, or VAT) is central.

Tsai Chi-yuan points out that in the past the tax system emphasized the idea that "where there is income there should be tax." But given the rapid decline in the birth rate-which means that in the future there will be proportionately fewer young people working, while the main body of society will increasingly be elderly people who consume but who do not earn-reliance on income tax alone will not do the job. It will be necessary to draw more government revenues from consumers. Shifting the tax burden toward consumers will have the added benefit of reducing disincentives to work among income earners.

Currently the VAT in Taiwan is 5%. This is the same as in Japan, but there is still a lot of room to increase it if you compare this figure to the 25% in Northern Europe or the 15% in Western Europe. Shen Fu-hsiung, who advocates raising the VAT to 10%, relates that each percentage point rise will add an estimated NT$35 billion to the nation's coffers; if the rate were raised to 10%, this alone could almost fully deal with the projected budget deficits of NT$200 billion per annum.

But will the need to pay a higher tax affect people's willingness to consume? Finance scholars generally conclude that it will not. For one thing, as Tsai Chi-yuan points out, not all products have VAT levied on them. For example, it does not apply to food, agricultural products, or basic necessities. As for conspicuous luxury goods, if a little extra VAT can reduce their attractiveness, so that the money that would have been spent on them ends up in savings, this could achieve the hidden objective of using the tax system to direct citizens' economic behavior, and would be a good thing.

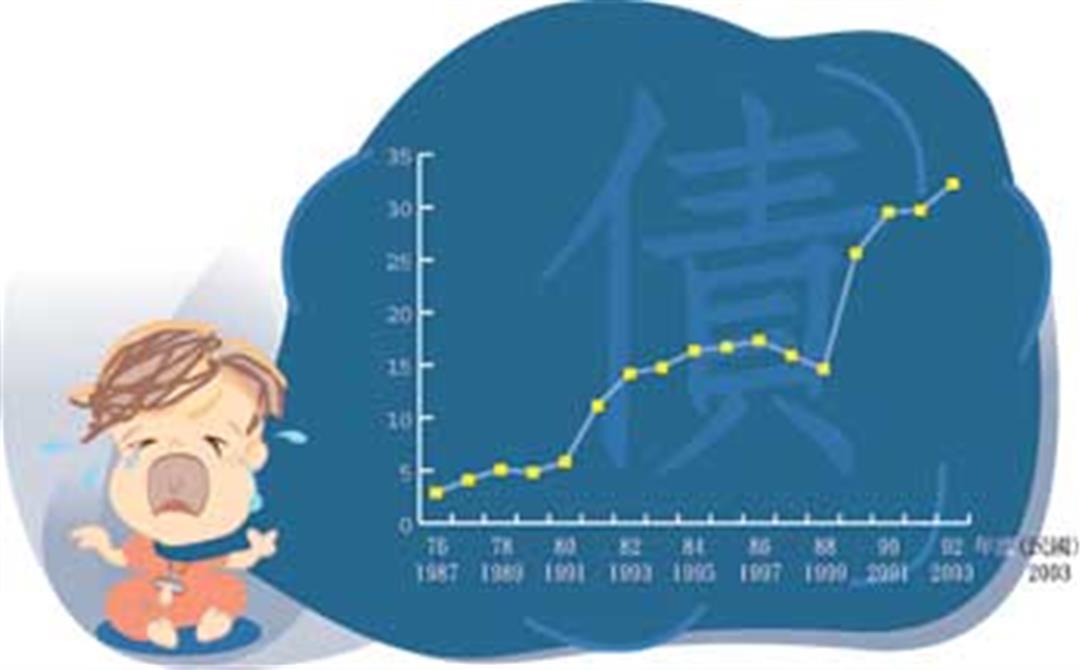

National debt as a percentage of GDP (%)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)