Amid cries from the business community for the government to rescue the stock market, an opposing view from Formosa Plastics Group President Y.T. Wang appeared in the paper. Wang nevertheless expressed his hope not to talk about the stock market in our interview.

"There are a lot of people who are stuck with worthless stock, so you hear them screaming. But I can't say any more about it: the problem is too great."

Originally, in September, when Y.T. Wang heard that many were crying to the government to rescue the market, he let off steam to the press. If it's as they say, that buying and selling stock is a normal investment channel, and the market is not a casino, then they should respect the market's adjustment function. Some enterprises milked it for all it was worth when the going was good, but new that the situation has turned they want the government to intercede to clean up the mess and prevent their being stuck with valueless stock. It's really shameless!

After these harsh words got out, Y.T. Wang immediately felt the heat from all directions. So he's not willing to express his views about the market anymore. But what about the expechain reaction domestically brought aboutrience of Formosa Plastics and of Wang himself in the market?

"We buy stocks as an investment. Unless the company is in urgent need of cash, we just watch the dividend. Since it is an investment, the rise and fall of the stock price is irrelevant. If you talk speculation, I've lost a lot. With stock prices the way they are now, calculating assets, my loss is huge, but I haven't made one complaint, and invest just the same!"

As for the rumor that employees who jumped to the securities business would like to "get back where they started from," Wang confirmed this point. "I also hope they come back, but the staff at the company are all opposed, so it's impossible."

Why hope that they come back? Isn't there concern that when the stock market takes a turn for the better, they'll take off again? "They have experience! It's helpful for the company. But nobody else agrees, so all I can do is to just live with it." At the same time Y.T. Wang recalls his sentiments when over 100 subordinates resigned in turn: "How could it not hurt? Just imagine, a guy comes to you fresh out of college, you give him years of training, and just when they really understand things, they tell they are leaving. But if you pay him NT$50,000 and someone else offers him NT$100,000, what's the point in blaming him?"

Wang believes that the economic downturn is an environmental problem: with risig prices, rising wages, and decreased export competitiveness, naturally the economy will slip.

He believes that in this recent time period, with more than 300 stock brokerages (even more than Japan, with an economy 30 times as big) and the unreasonable rise in stock prices, it really is a casino. Social habits have become extravagant, and people try to get rich overnight, and take risks, which causes social disorder.

"But now things are slowly coming around," Y.T. Wang believes. The bourse has collapsed, and people are turning their attention back to doing business. "From the point of view of Taiwan's overall economic prosperity, we still have hope."

(interview by Elaine Chen/tr. by Phil Newell)

Y.T. Wang:

If the Stock Market Isn't a Casino, Then You Should Respect Its Market Function

Q: Why have you recently repeatedly called on the government to "save the stock market"?

A: The stock market is an important capital market for the country. If the stock market is not robust, not only will entrepreneurs find it difficult to raise liquid capital or lose an investment outlet, the money tied up in stocks will be sharply reduced following the collapse of stock prices. Lately because the stock market has been heavily set back, the problem of poor circulation of funds among enterprises has become increasingly evident, which has caused the withering of all sectors.

I believe that there is a great gap between the perceived impact of the public and that of the government. I suggested this [action to save the market] for the first time in May, and today it is the sentiment of most businessmen.

Q: It is rumored that your concern for the stock market is connected to your management of Taiwan Cement and China Trust.

A: My great concern about the chain reaction domestically brought about by the collapse of the stock market is the product of accumulated experience. To save the stock market is not to save a certain few enterprises, but to maintain the vigor of the whole economy.

Some people say that it must be that you, Koo, have your capital tied up in stocks that are now worthless. This is ridiculous. The Taiwan Stock Exchange Cooperation was created by me single-handedly. Avoiding getting involved in buying and selling stocks so as not to mislead investors is my principle. The stocks held by Taiwan Cement are mostly long-term investments, and are not lightly moved around with the ups and downs of the market. There is only NT$100 million of idle capital authorized for use by the finance department by the Board of Directors, and the purpose is financial management.

As for China Trust, I have already left the chairmanship for nearly two years, and don't interfere in operational management. To say something that people might criticize me for, I believe that those who run businesses should not run banks, because a bank is a public instrument for society. What if your business is in trouble then the bank has to demand its loan be repayed to protect the interests of the depositors? If you have both a business and a bank, how can you deal with this point? Therefore, it was for this that I insisted two years ago on resigning the chairmanship of China Trust.

Q: Well, under what circumstances would you describe the stock market as normal?

A: Sudden rises and drastic drops in the market are both abnormal phenomena. A normal stock market moves in step with a country's economic growth.

In other words, only a stock market that reflects a country's economic trends can be considered normal.

As for the reasonable price of a stock, because there are many variables, there is no definitive conclusion. But one can use changes in a few basic indicators, such as trends in the interest rate or exchange rate, the company's PE ratio, and the overall economic development situation as parameters for evaluation.

According to the assessments and studies of authoritative foreign scholarly institutions, if there were not the shadow of the crisis in the Middle East, the index for Taiwan's stock market would float around 5,000, which is by no means too high.

Q: What do you think the government should do under current circumstances?

A: As for economic development, the government has always operated on the premise of growth with stability. Although Taiwan's overall economy is already headed toward liberalization, liberalization by no means implies that one does nothing about wild fluctuations, or doesn't pay any attention to crazy collapses, and just says that these occur on their own.

For the past year or two, the stock market has approached a gambling casino. The risk has been very high. It should have been rectified very early on and right at the start underground investment houses shouldn't have been allowed to get dug in, giving them the opportunity to cook up stock and real estate prices using their vast financial strength.

Nevertheless, normal stock investment has always been encouraged by the government, and is needed for free economic development. You mustn't see all of the people who invest in stocks as gamblers, and still less can you deny that the stock market is a window on the economy revealing its strengths and weaknesses. The government has the responsibility to maintain financial order, and cannot just pass the buck in terms of normalizing the stock market.

Just as globally there are no central banks which do not intervene in foreign exchange markets when it is necessary, there are no financial authorities who do not intervene in the stock market during crisis.

Several policies being currently adopted by the government, such as easing capital for stocks and allowing established foreign investment institutions to enter the market, are precisely those methods to save the stock market recommended by me five months ago.

If in the absence of the Middle East crisis the market continued to decline, the government would have to assess basic economic conditions and the structural strength of those companies on the market, and establish a base line, to prepare when necessary to create a stabilization fund in cooperation with banks, trust companies, insurance companies, and major foundations, and go into the market.

Q: Can the Taiwan stock market ever again have such halcyon days? If yes, what conditions are needed?

A: If only the Taiwan economy continues to grow under conditions of industrial upgrading, improvement in the investment climate, and promotion of public infrastructure, and national income continues to increase, then the Taiwan stock market will once again be prosperous. But never again will it climb crazily--it will simply return to normal.

(interview by Theresa Sung/ tr. by Phil Newell)

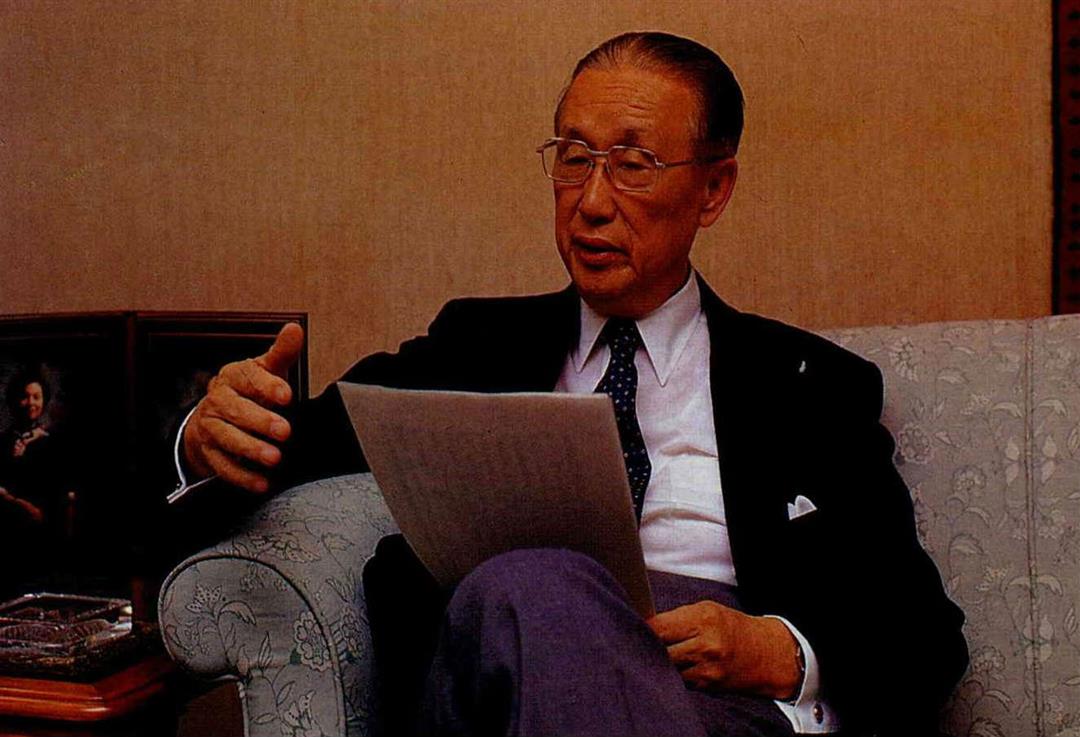

Koo Chen-fu:

It's Not Saving the Stock Market; It's Saving Overall Economic Vitality

Q: The Minister has said that of the main focus of Ministry of Finance work, the stock market problem is what worries most sectors. Therefore, how a minister can make the market healthy will be the basis of his "grades." What would you call a "healthy" stock market?

A: Briefly, you want that the market can't be manipulated by a small number of people, that there is no insider trading, and that investors believe it is a safe investment location, then you can call it a healthy stock market.

The impact of securities markets on the national economy is enormous. Because it is an important channel for concentrating capital, if it can develop soundly, not only can everyone invest with peace of mind, businesses can get the funds they need for operations in a normal way.

Q: To make the stock market healthy is of course the goal of government policy. But the current low ebb affects the overall national economy. So some believe that the MoF should take extraordinary measures to rescue the stock market. For example, there's lowering the stock transaction tax for immediate impact. What's your view?

A: Whether the stock transaction tax should be lowered or not is the most hotly debated topic now. I insist that it can't be lowered, because the tax is a necessary measure to prevent short-term trading and to stabilize the market.

Last year, each stock was traded on average six times. Whereas in the US or Japan normally each is traded less than once per year. If our stock circulation rate is so high, can the stock market really be stable?

Currently the calls to lower or even eliminate the stock transaction tax are not without suspicion that a few "big players" are taking advantage of the situation to create the erroneous consensus that the low ebb in stocks was created by the stock transaction tax. In fact, when the stock transaction tax was implemented in January of this year, according to that logic, shouldn't stock prices have dropped sharply? But they didn't. Most ordinary products have sales taxes; when you make money you have to pay income tax; and stocks are already tax free--if you eliminate the stock transaction tax, how can you talk about fairness in taxation? Moreover, compared with countries around the world, our tax is not the lowest, but it is also not high. For example in Holland it is .12%, and in Korea it is .2%, both lower than us. But in Norway or Italy, it is 1%, in Sweden it is 1% imposed on both the buyer and seller, and in Belgium it is as high as 3.5%, which is a lot higher.

Moreover, the tax is borne by the seller. For every NT$1000 sold, they must pay six NT dollars. How can you call this high? If investors buy and sell every day, then of course the burden will be heavy. So I have proposed the idea that "keep stocks in hand, but don't always have the stock price in mind." This is to encourage everyone to make long-term investments. I don't want to have everyone devoting all their attention to the rise and fall of stock prices, which would affect their work and families.

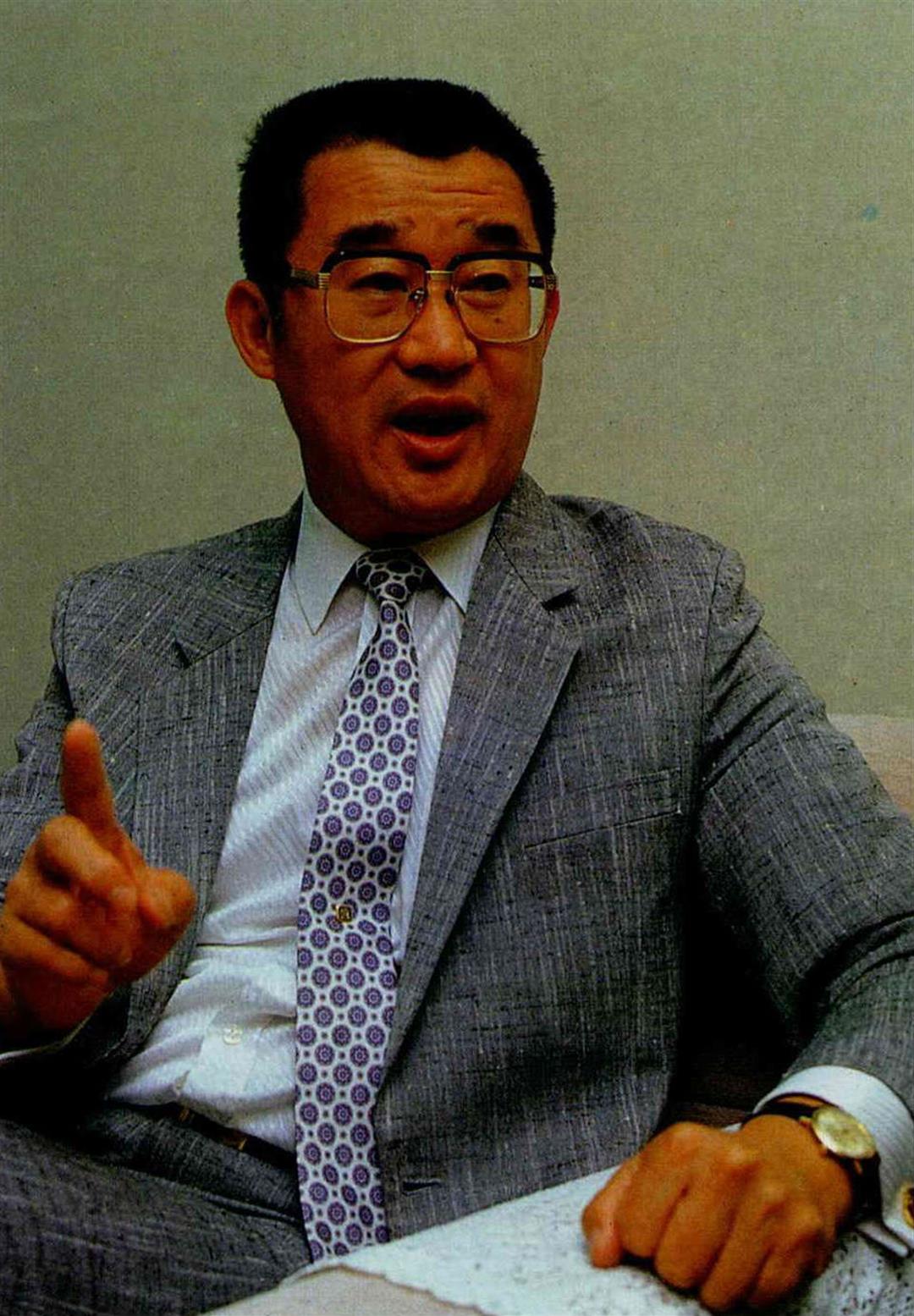

Wang Chien-hsuan:

Making the Stock Market Sound Is the Aim of Government Policy

I insist on not lowering the tax. Some people say this is because of "face," that one is afraid to admit a mistake. In fact, as a government official, anything can be changed as long as it is beneficial to the country. But lowering or eliminating the stock transaction tax will stimulate an increase in short-term trading, which is not beneficial to the country, so it naturally can't be done.

Q: Besides short-term trading proliferating excessively, what other problems does our stock market have? How can you treat them?

A: There are too many small investors and too few institutional investors, and the scale of the stock market is also too small. . . These are all major defects. Recently the MoF has administered some treatment including allowing foreign institutional investors and labor pension funds to enter the stock market, liberalizing financing and financing securities, as well as planning to release stocks from state-run enterprises. These are all practical steps to make the market sound.

Q: What kind of proportion do you think institutional investors should constitute? What kind of bad impact results from too many small investors?

A: In stock markets abroad, institutional investors ordinarily constitute about 80% of the market. We're just the opposite. As of the end of September, there were more than 5 million accounts, with about 3,130,000 account-holders (some people have opened two or more accounts). Of these, legal entities only accounted for 6,400 plus.

Institutional investors have numerous channels for information, They have specialists to analyze the impact of various situations on the companies on the market. Small investors mostly lack information, and easily follow rumors. In our stock market these small investors constitute the great majority, and the market is thus relatively unstable. Therefore an urgent task is to increase the proportion of institutional investors. The MoF has decided to permit labor pension funds to enter the market and to permit foreign institutional investors to invest in the market. Not only can these relieve the problem of the current low willingness to buy, they are even more important for achieving the long term goal of a stable healthy market.

Q: But there are many objections among scholars to labor pension funds entering the market. They believe that should there be a collapse, this would harm labor interests. Moreover, this seems like the government intervening in the market. Whether or not this can increase investor confidence is still unknown. What do you think?

A: It is estimated that 20% of labor pension funds will enter the market. They have about NT$8.6 billion. Each time they buy stocks, it probably won't be more than ten or twenty million at a time, and it won't be committing everything at once. From the perspective of the current market, the degree of intervention is limited.

This step is absolutely not harmful to labor interests. This is because the regulations for use of labor pension funds point out that they must guarantee a return at least equal to a two-year time deposit account. If the profit from the market investment does not reach this figure, then the difference will be subsidized from the national treasury. Moreover, pension funds will be making long-term investments. In the long run, the odds can be predicted.

According to regulations, pension funds can assist major national construction plans, can buy public bonds, certificates of deposit, or, as in the past, put the money in the bank. In fact, abroad, using pension funds to buy stocks has long been common practice. For our funds to go into the market to buy blue chip stocks will make the operation of the funds even better. As for what should be designated blue chip stocks, and how to buy them, the Central Trust of China will define these things.

Q: Besides raising the proportion of institutional investors and improving the willingness to buy, is there any other purpose to permitting foreign institutions to invest in the stock market?

A: Since it will help invigorate the market, raise the recognizability of our on the board companies internationally, and raise alternative channels for our industries to acquire capital from capital markets, the entry of foreign institutional investors will be extremely positive for our national economy.

Even more important is that Taiwan sooner or later will become one of the major financial centers in Asia, so the securities market must first liberalize and then internationalize. Besides allowing foreigners to enter the local market, we will later permit our people to invest in stocks abroad.

Q: As for releasing stocks of state run corporations, the main purpose is to broaden the scale of the market. When will steps be taken?

A: The most direct method in the MoF plan to expand the stock market is to encourage even more top companies to go on the board. Releasing stock from public corporations is one part of this. However, public corporations are enormous. For example, the number of stocks from the one company China Steel would be equivalent to ten or twenty companies now on the market. And with willingness to buy less than enthusiastic, increasing the supply could push the current low mood even lower. So now is not the time to issue.

Q: When will be the time?

A: After stock prices stabilize, that will be the time to release the stocks. Although in my own mind I have an idea of what it means to have stable stock prices, in order to avoid disputes, I will not specify any figures at this time.

Q: What plan does the MoF have to eradicate it?

A: Currently, the tax bureau and the Securities and Exchange Commission are already working together to check in detail into 100 companies on the market. They are checking to see if the directors have not manipulated stocks. Once they discover proof, they will move to stamp it out.

Nevertheless, inside trading lines are extremely difficult to uncover. The SEC has no judicial power of investigation. Therefore the MoF has chosen a two track policy: one is to amend the law, and two is to work with Bureau of Investigation to establish case units to strictly handle illegal trading. Further, we are in the process of selecting personnel from the major units which the MoF can use to oversee the securities market. These personnel will first receive on the job training here, and then be sent to the US, Europe, Japan, and Singapore to study. Similar training will begin continually in the future. These people are my "seeds." If the seeds are well planted, then securities market oversight will naturally get on the right track.

Q: A substantial amount of floating capital and inadequate investment outlets are the factors creating the wild rise in the stock market in recent years. What methods to cope does the MoF have?

A: Strictly speaking, the securities market can be divided into the stock market and the bond market. But people here mostly have concentrated attention on the stock market. In fact, the bond market has considerable room for development. The bond market often constitutes 70-80% of the overall securities market abroad. But for us the stock market constitutes the majority. Taking the US for example, government-issued debt is 40% of the bond market. The room for flexibility for us to issue public debt is still very large. In the future the government will strengthen the use of issuing public debt for public construction, which on the one hand will stimulate economic growth, and on the other will accumulate strength for building a bond market to allow investment channels to become even more diversified.

[Picture Explain]

(Photo by Lin Jun-hong)

(Photo by Huang Lili)

(Photo by Diago Chiu)

(Photo by Diago Chiu)