Longevity and falling values

The concept behind using reverse mortgages to support the elderly is a progressive one, but calculating the risks is complicated.

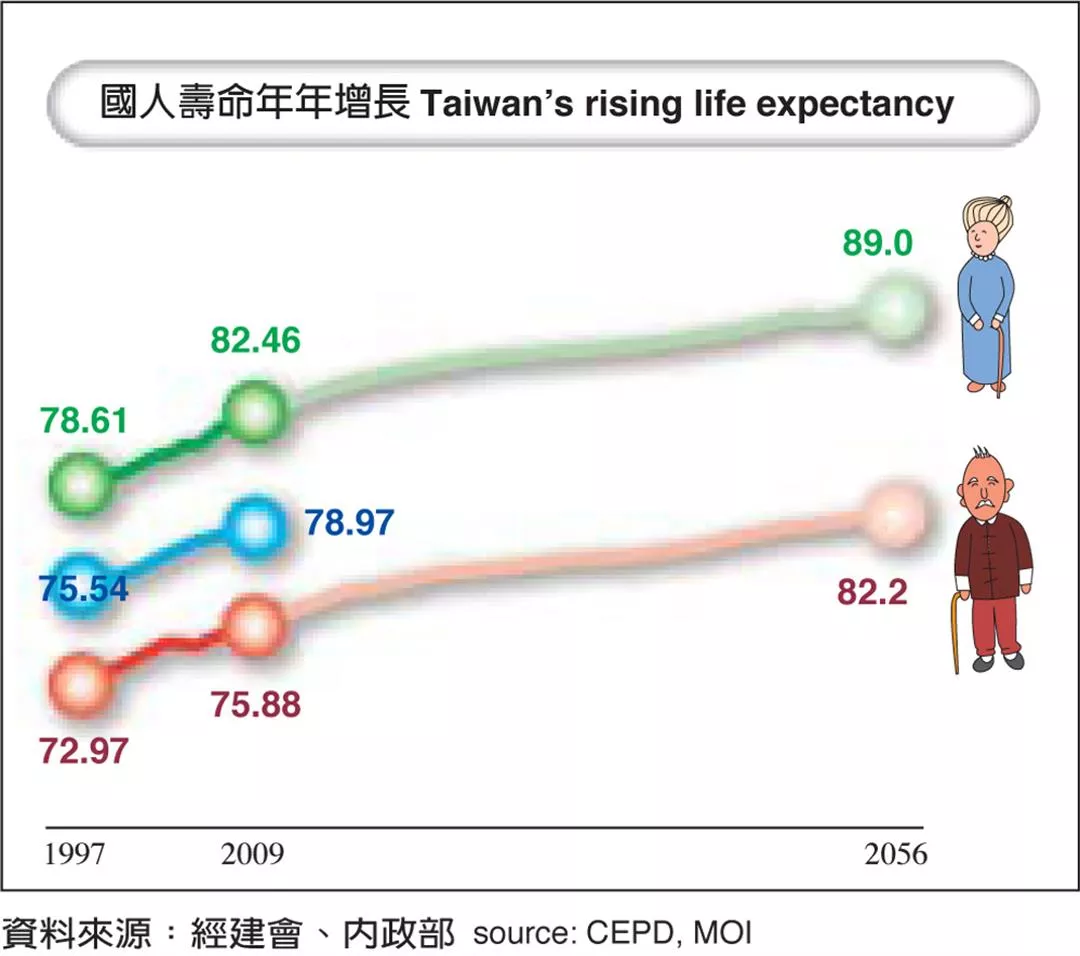

Take, for instance, the situation in Japan. These kinds of mortgages began to be offered 20 years ago. But then the real estate market collapsed, and depressed home values coupled with the high life expectancy of Japanese (83 overall, with men living to 79 and women to 86) has made the government reluctant to take them over and private banks reluctant to continue to offer them. The system has broken down.

When reporting to the Finance Committee of the Legislative Yuan, Sean Chen, the Financial Supervisory Commission chairman, pointed out that government support is the key to why reverse mortgages have worked in the United States but not in Japan.

The American reverse mortgage system also had to undergo reforms before the mortgages caught on. The problem there was that once sponsoring banks had paid out 95% of the value of the homes, they could see that they would be losing money from there on out, but they couldn't force healthy seniors to leave their homes. The government had to take on the risk for this "last stage" and continue to provide the seniors with money for living expenses, while letting the banks withdraw completely.

The February issue of TRR, an American publication focused on the American mortgage industry, noted that reverse mortgages in the US didn't need government subsidies for 20 years "thanks to hefty mortgage insurance premiums, conservative actuarial assumptions, and robust house prices for much of that period." But after the economic tsunami of 2008, when US real-estate values crashed, banks became deeply worried about getting stuck with "junk assets," and they changed tack to ask for government support. But as a result of those falling real-estate values, the US Congress turned down a requested US$800 million subsidy of the Federal Housing Administration (FHA) Home Equity Conversion Mortgage (HECM) insurance program, thus creating an impasse.

Yet the article points out that the US$800 million subsidy was miniscule in comparison to the multi-trillion dollar bailout of the Wall Street fat cats. And it noted that if the US government doesn't help seniors to first get by on their own assets, many of them will end up requiring direct government assistance, which will end up being much more expensive in the long run.

Each nation that has implemented reverse mortgages has dealt with similar variables. The main risks involve mortgage holders living too long, inheritance issues with children, and fluctuations in housing values and interest rates. Generally speaking, financial institutions in Taiwan are showing conditional support for the concept. Because urban real estate has proven resistant to sharp price drops, institutions suggest rolling them out north to south, trying them first in the cities and then in the countryside.

Trial implementation

Chang Chin-oh emphasizes that that the law of large numbers mitigates the risk posed by long-lived seniors, because in large pools of people, some live to a ripe old age and others die young. It's the same principle for private life insurance or national health insurance: Large numbers of participants spread the risk.

"There are always blind spots in the early stages of implementation, and greater risk," says Chang. "The first financial institutions to offer these mortgages worry that there won't be enough applicants and that 'whoever goes first, goes bankrupt first.' Consequently, we recommend that they go slow, starting with pilot trials and gradually accumulating the experience necessary to build a robust system."

James Hsueh notes that in 2009 the Executive Yuan held inter-ministry discussions on reverse mortgages, and included the concept in a package of measures intended to promote an age-friendly social environment. The government has planned a cross-ministry taskforce on the subject, which will get up and running as soon as it receives budgeting. The Taipei City Government has been asked to study and review the concept of reverse mortgages. It's hoped that by early 2011 they will begin to be granted to senior home owners in Taipei who live alone. Issues or potential issues will be identified for further consideration: For example, how can home values be set in a bull market? Should the rates be adjusted every year, or should the two sides gamble and accept the first negotiated rate? Should the money that the elderly pull out of their homes be considered income for tax purposes? Should payment schedules be set for a maximum of 15 or 20 years? Or, alternately, should monthly payments be guaranteed until death? If a married homeowner dies, should the spouse be able to continue to live in the residence? All kinds of issues have to be grappled with before a system can be set firmly in place.

"Reverse mortgages are well suited to future social developments in Taiwan," Hsueh says. "The basic idea is that one should be able to grow old at home. If the government bears the ultimate risk, financial institutions should be quite willing to offer them." Many senior citizens who live alone reside in old districts with deteriorating homes, and they can't afford renovations and don't dare to sell and move. These mortgages may thus help to revive older districts, achieving urban renewal.

If current or future elderly want to avoid regrets about leaving money behind them after living their final years in poverty, then they ought to consider reverse mortgages.

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)