Do you still remember those crazy days of three years ago? At that time thirty-year-old Mr. Chang, seeing his colleagues one by one happily making a fortune in the stock market, said to his wife, "Without a house, how can we have children? Up until then the sort of person who did things by the book, against the protests of friends and relatives, he suddenly left his job and put his savings of NT$600,000 on the stock market, becoming a full-time member of the "stock market clan." Not without apprehension he surveyed the scene, delved into foreign currency, buying and selling shares, lotteries, and so on . . . . Everyone has a way of making money he bragged: "Let house prices go up, in two years I can buy one!"

In the end such bragging cannot be long-lived. Once the peak of the fever had passed, there followed a cruel slump ending at a fraction of its high 12,000 points; the windows of new buildings were festooned with advertisements seeking cheap sales. Mr. Chang returned to his nine-to-five life and playing by the book. The only difference is that, apart from having a babbling baby daughter, he is also more than NT$2 million in debt.

Dangerous Factors at the Ready?: Since the curtain fell on the scene of speculative fever, a year of peace has fleetingly passed. After the shattering of that dream of riches from the period of massive foreign exchange reserves, a soaring Taiwan dollar and the pouring in of hot money, at a time when the market was already being full of people's surplus cash, people have recuperated by burying themselves in their work. What money they had left they have placed in bank deposit accounts.

Nobody wants to get burnt again.

However, it seems that factors of disruption in the air might be stirring again . . . .

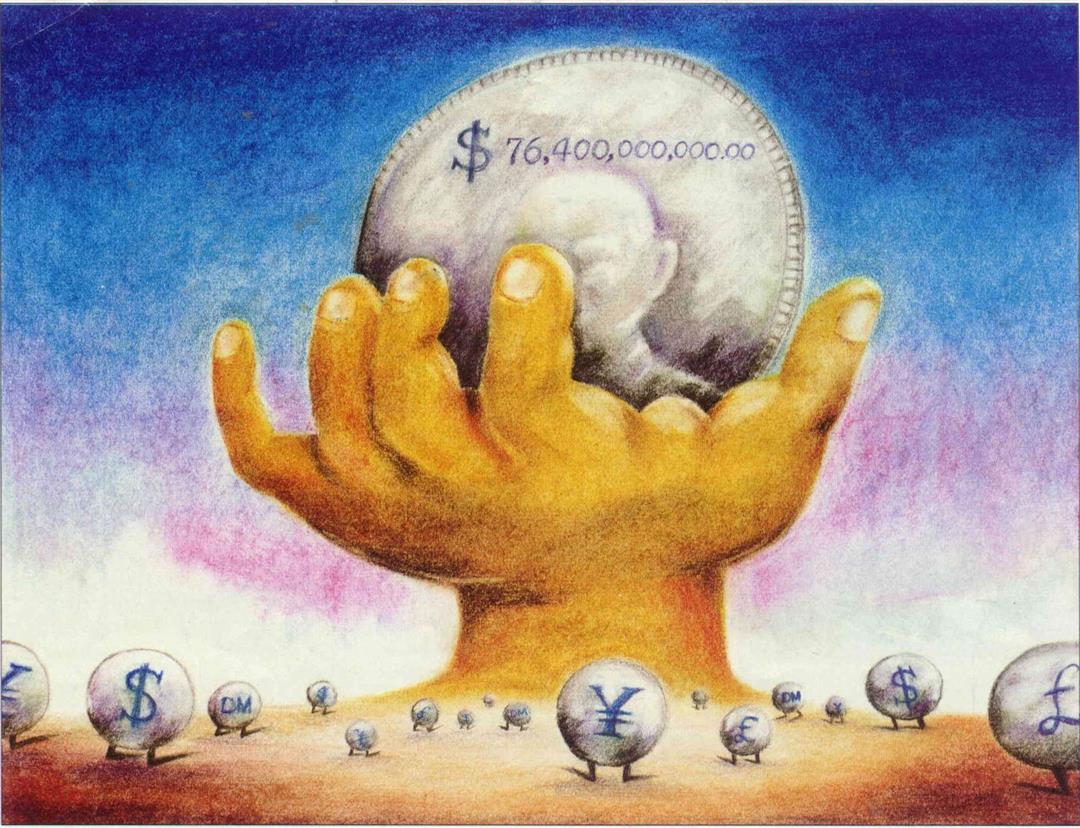

Looking back over this year, at the end of September Taiwan's foreign exchange reserves were again the world's highest at US$76.4 billion. This figure is even US$12 billion higher than that of last June, when there was a massive outflow of money, and is not far from the historical high point of US$77.4 billion on the first half of 1989. And this does not include the US$7 billion, DM500 million and the US$5 billion in gold that the Central Bank has as in supplementary reserve at the TIBOR. Apart from this, following stabilization after a slight fall against the US dollar, the Taiwan dollar has begun to appreciate again, already breaking through the US$1 = NT$26 threshold in November. Entrepreneurs in real estate have also made moves, actively putting out massive advertisements, and news of new projects is incessant, giving rise to a heated atmosphere around land prices.

The main reason for the large reserves of foreign exchange is that this year exports are up again. For example, exports in July and September were at their highest levels since monthly records began, so that exports for the first three quarters of this year have already come close to overtaking US$10 billion. And hot money, one of the two main factors leading to the disaster of speculative fever (along with surplus money in circulation), has come back to Taiwan. People are just waiting for the opportunity to have their golden dreams again by taking advantage of currency exchange, the stock market and real estate.

How much hot money has actually come in? No one can be certain. We can only pick out clues from the available statistics. To give an example, October last year saw foreign exchange deposits of US$2.166 billion, while there were only applications for the purchase of a mere US$421 million dollars on the foreign exchange market that same month. Taking into account about US$500 million in interest, the rest was all more than likely accounted for by hot money flowing in from overseas.

Cash Waiting for Action: From all these clues it would seem obvious that the monetary tide is again high. Nevertheless, in recent months there has been no apparent reawakening in the property market. Although property prices have not fallen from the high point to which speculation drove them in the last wave of madness, on the whole the market is dead; and the stock market is lingering around the 4000 mark.

The many punters who stuck out their necks and got caught out by the market are still on a road to nowhere, waiting for the return of the days when prices only rose and every purchase was a winner.

Regarding this phenomenon, the International Commercial Bank of China's director of international finance, Chen Chi-chu, says: "Perhaps the Taiwan dollar will go up, but the rate of climb is already limited; moreover, shares and real estate are at present still weak. Hot money will not find any rewards so there is still no great influx."

Just as there is no great influx of foreign money, there is also no active speculation with the domestic cash in circulation, the main reason being that most people are once bitten twice shy and have taken to putting their money into bank deposit accounts. This in turn has led to fixed-term deposits in all of Taiwan's banks standing at the alarming figure of four-and-a-half trillion Taiwan dollars. Added to this, the NT$100 billion submitted as security by the fifteen new banks when they were established, which is also temporarily frozen. In addition, in the last fiscal year the government issued 100 billion government bonds which have all been snapped up, so that this year the number will be increased to more than 250 billion; and the government is preparing for issues of more than one trillion bonds over the coming years to finance the Six-Year National Development Plan. All this means that people's capital will all be accounted for and that there will be an increasingly small amount of money in circulation.

Various Financial Measures Adopted: Even more important is that past experience has made both government and people wise after the event. The new managing director of the Bank Sinopac Wang Kuang-sheng, expresses his feelings as "cautiously optimistic . . . The speculative madness of three years ago should not be able to happen again."

"In fact the appreciation of the Taiwan dollar and high foreign exchange reserves are not directly or necessarily linked with speculative fever or inflation. What is important is looking at how policy in the financial markets is carried out and supporting their stability," says Lu Fang-ching, deputyexecutive secretary of the Commodity Price Supervisory Board at the Ministry of Economic Affairs examining the problem from another angle. "The point is that the central bank, compared to five years ago, is more experienced and very cautious."

For example, in the 1976, the central bank's foreign exchange policy was completely used for coordinating imports and exports, and this has not changed much over the last twenty years. Because of this, under pressure from the United States to raise the value of the Taiwan dollar, so as to maintain the vitality of Taiwan's exports and small and medium-scale enterprises, the central bank has submitted itself to a beating like a mother hen protecting her chicks. Keeping a constant eye on the depreciating dollar, it has made large purchases of U.S. dollars to prevent the Taiwan dollar from heading skyward in one jump. The result was that during the process of the Taiwan dollar moving from NT$40 to one to the U.S. dollar to NT$28 to US$1, the rate of money supply to the market at one point reached 51 percent, becoming a prime cause of the disaster of the speculative fever. In comparison, the central bank has now taken measures to cut the money supply so that there was negative growth in the eleven months between March 1990 and February 1991. Over the past six months, although the Taiwan dollar is again climbing, the central bank has kept the supply of money under tight control so that it will be hard for it to exceed its upper limit of 20 percent.

A Change of Times: With the tide of money under control and the money supply not as before, another aspect is that speculation has also been made even less easy by an increase in the number of channels requiring the money that is around. Taking the stock market as an example, in 1986 there were only 130 companies on the market with a total capitalization of around NT$230 billion. At present, this has expanded to 250 companies with a capitalization of NT$610 billion. Moreover, the fall in real estate values has restricted the number of punters entering the battle field.

To direct any possible resurgence of surplus capital, the government has speeded up the pace of internationalization and the liberalization of the domestic capital market in recent years so that the small investor has greater options for investment. Notable examples are the Overseas Common Fund, the recently produced law on trading in perishable goods, and the just passed foreign exchange guarantees. "Although at present the opening up of these channels is still too slow and the restrictions are too many," says Wang, "already the first steps have been taken towards consensus at the higher levels and towards greater knowledge among the people."

The problem is just that the pain last time went too deep and people have still not relaxed. Moreover, so as to prevent an influx of hot money, the central bank has lowered interest rates in line with the US$ and Japanese yen, although the rate is still "not good enough"; however, to have a low adjustment leads to another concern that is hard to resolve.

"People deposit their money in banks on the one hand because they are still afraid after the last bout of speculative fever, and on the other because they want the highest profit from an annual interest rate of 1 percent," points out one bank manager. "If interest rates should keep going down, as soon as these people find their fixed periods of deposit have reached an end, they will not put their money back into the bank but will want to try out other investment opportunities. That is when the danger of speculative fever will arise again!"

Has that time arrived? How long have we left? Nobody dares say. Yin Nai-ping points out, "The effects of most changes in monetary policy take about ten to eighteen months to gradually become apparent. Because of this, we can only watch closely with baited breath."

The Worries of Too Much Money: Of course, blocking and guiding can only be considered as treatment of the symptoms. The way to tackle the underlying problem is still to reinvest the money that is building up from the trade surplus and thereby create an even more efficient economy.

Wu Hui-lin, a long-time believer in economic liberalization, feels that the government should let people participate more in large investments. He points out that there are in fact many entrepreneurs with both money and guts. Communications, telegraph, television, oil, electricity, and so on, should all be open to investment by the public.

If this money cannot be attracted into economic investment, it is not only unfortunate to have it in circulation, but it is also dangerous. "Perhaps investors lost enough on stocks and real estate for there to be no resurgence within a short time, but people only want a bit of spare money and they might still go in search of some novelty to play with." Wu Hui-lin takes the example of the great Dutch tulip bubble in sixteenth- and seventeenth-century Holland. It just needs one "believer" to fan the flames and it is most probable that everyone will rush blindly in.

Is it bad to have money? Of course not. The international status of Taiwan has soared over the years and there have been new diplomatic gains. People can also travel anywhere with confidence. This is all thanks to our high reserves of foreign exchange and the strength of the Taiwan dollar. How to have the benefits of this and yet to avoid the disasters -- in a world worried about poverty, this is still Taiwan's special problem.

[Picture Caption]

Will foreign exchange reserves building up to US$76.4 billion by the end of September rekindle speculative fever? (graphic by Tsai Chih-pen)

The establishment of new banks will absorb a lot of capital and contribute to reducing the amount in circulation; public listing will also give people a new channel of investment. (photo by Diago Chiu)

The establishment of new banks will absorb a lot of capital and contribute to reducing the amount in circulation; public listing will also give people a new channel of investment. (photo by Diago Chiu)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)