"Farmers' Insurance is a policy of 'unbounded kindness'" is the assessment of Kuo Chi-sheng, Director of the Department of Health for Kaohsiung County, which implemented complete farmers' insurance ahead of schedule on August 1.

Kuo says that farmers' insurance has led to a great improvement in medical habits in the countryside. In the past, farm families couldn't afford to go the hospital for modern treatment if they got sick. That either led to bankruptcy or to alternative--and none-too-reliable--treatments. Insurance has led to a greater willingness to go to the hospital, for better treatment and better health-related information.

During its three-year trial period, the program drew many admirers. Some who lived in areas not part of the trial program tried to change their household registration to the areas that were. Others who would have nothing to do with the Farmers' Associations joined since this was a prerequisite for the insurance.

Further, the plan has given farmers, whose incomes traditionally trail urban workers, a basic guarantee of medical treatment, and "a feeling of security," according to Hung You-yi, who heads up insurance affairs for the Ta-liao Village Farmer's Association in Kaohsiung County.

The trial program was announced on October 24, 1985. It involved 41 of the province's nearly 300 Farmers' Associations and covered about 119,000 individuals. At the end of the two-year initial trial period, the program was expanded to 113 associations with 240,000 individuals covered, for the second trial period. Under pressure from farmers' demands, the provincial government announced that complete implementation would begin on October 25 of this year. All 870,000 Farmers' Association members will be covered.

Currently the plan covers illness, injury, and births, and provides subsidies for funerals. Unlike the "comprehensive" plans for labor and public employees, farmers' insurance does not include assistance for unemployment, the handicapped, retirement, or death. This is because the costs of the former are borne mostly by employers; since farmers are self-employed and must bear the costs directly, the coverage is less. Already, the government pays 50% of the costs, the farmers' association pays 10%, and those covered pay 40 percent, yet the plan is in serious deficit; there is no room to expand the types of coverage.

Although farmers' insurance comes much later than that for labor (1950) or public employees (1958), it has generated tremendous interest in the problems of "social welfare" and "social security" and has been seen as "the testing ground of complete national health insurance."

Unfortunately, the program has not been ideal in either structure of management. This has caused many scholars to warn about going deep into debt on social welfare programs, a problem faced by many "welfare states."

During the three-year trial, the program ran up losses of NT$969 million, notes Wu Kai-Shiun, an advisor to the "National Health Insurance Planning Committee" of the Council for Economic Planning and Development. The problems result from weaknesses in the design of the program and the use of Farmers' Association regulations in drafting the insurance regulations.

First, since the association only admits one member from each household (and membership is required for eligibility for insurance), farm families simply enrolled the family member who was oldest, weakest, sickest, or, for women, pregnant. The average age of those covered was 55, compared to 33 for labor insurance. This method led to violations of basic insurance principles that "the number of healthy people covered should exceed that of the ill", and that "the more people who are insured, the more the risk can be spread around" according to Hsueh Li-min of the Chung-hua Institution for Economic Research. The rules instead invited a "concentration of those most at risk," so that the original intent of the program was soon lost.

"These types of things are a normal part of human nature; one can only put the blame on the poorly written regulations," argues Wu Shun-tsung, Director of the Farmers' Association Guidance Office of the Bureau of Agriculture of Kaohsiung County.

To close the loopholes, in the associations which were new participants for the second trial period, it was prohibited to sign up anyone over 70, and others had to have been participants in the insurance program for minimum lengths of time to be eligible. That losses were way down in the second period is due in part to these changes. Nevertheless, the government has decided to lift the upper age restriction when full implementation is begun on October 25. Most scholars are not optimistic about the financial consequences.

Of course there are other ways to balance the books. One would be to set aside a fixed percentage of insurance payment (say 5 percent) as a security fund. "It's like a reservoir. When it reaches an upper limit, rates can be lowered to benefit participants; if it sinks to a lower limit, rates can be raised," says Wu Kai-Shiun.

But since the program is already losing money, where can the extra funds come from? Even more of a problem is that there is no way to raise the rates in the event of losses, so that losses become cumulative.

"In fact, in the initial period it was estimated that the rate would have to be over 8 percent to be reasonable. But later the representative bodies lowered the figure (to 5.8 percent in the first period and 6.8 in the second)," Wu explained. "It's like trying to sell a product that costs one dollar at 80 cents; even a god would still come up short."

Participants now only pay about NT$250 a month (about eight US dollars) into the program, hardly a crushing burden. But some argue that with Taiwan's US$70 billion in foreign reserves, who cares if the program loses a few hundred million? The problem is that the cost is passed on to the general taxpayer, and the insurance loses its character as a means of mutual help (and becomes a simple transfer payment). Participants--and care providers--start thinking only about how to get a bigger share for themselves. One hospital in Yun-lin County began giving away free lunches and transportation as a way to attract business. They handled a record 1000 outpatients in two days.

Tsai Han-sien, Director of the Office of Social Affairs in the Ministry of the Interior, who handled planning for farmers' insurance legislation, says that what is needed is education to build up an insurance ethic. But education can take a long time; the immediate problem is how to stop the waste.

The best method is still cost-sharing, so that the patient would pay a part of the costs for hospital visits for minor reasons, an idea universally endorsed by scholars in the field. Currently many people go to the hospital for any minor problem. But some people's representatives have put the idea on hold: "Let's wait until the financial situation of the Labor Insurance Bureau improves," they argue. But how can it improve if cost-sharing is not implemented? Ask the General Manager of the LIB, Lin Chang-feng.

Other ideas are to separate different degrees of illness to receive different coverage, or to require those who want to go to major hospitals to first get authorization from local medical facilities. It was originally planned to set up a network of physicians in health offices in the countryside, but the fact that care in the major hospitals is covered causes participants to head off to the big city for treatment. Meanwhile, small clinics and rural doctors not authorized to receive farmers' insurance are losing patients rapidly and will face bigger problems when full implementation goes into effect.

Clearly the program faces many problems. But since it is a focal point of public attention, every aspect is open for discussion, and we believe that improvement is virtually well ensured.

[Picture Caption]

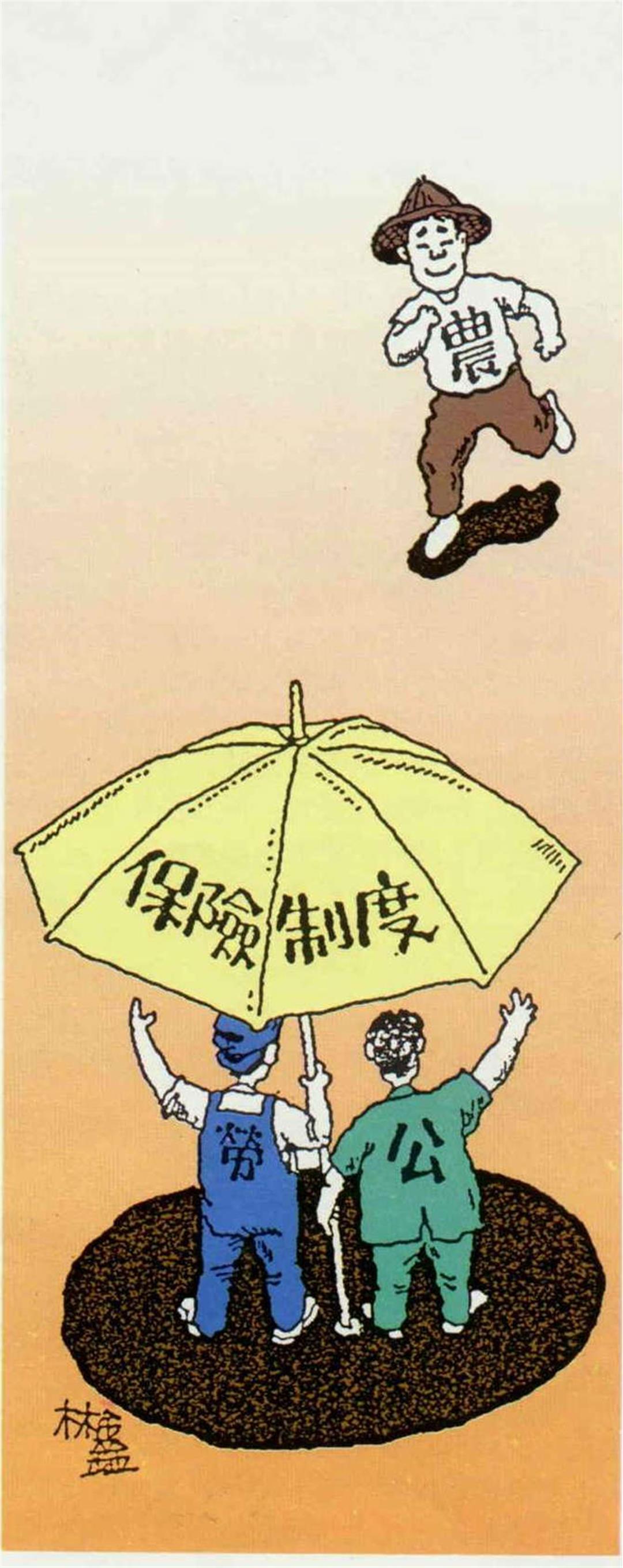

Farmers can get good treatment through Farmers' Insurance; though the government absorbs half the costs, it's worth it. (illustration by Lin Hsin)

Chronic disease brought on by exposure to poisons and chemical pesticides is one of the "occupational hazards" facing farmers.

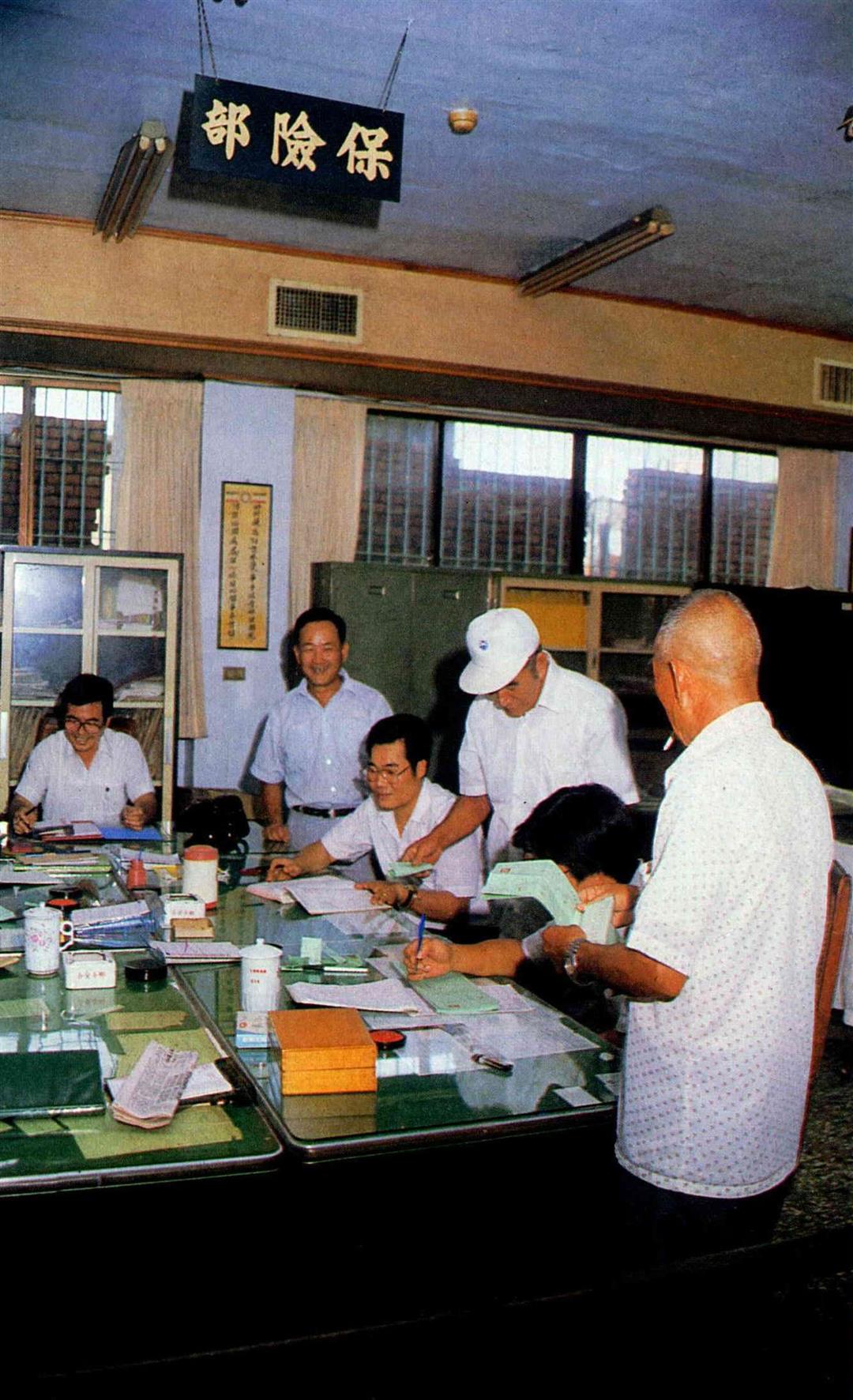

The farmers' associations have been instrumental in implementing the program.

The rapid aging of the farm population--and the high rate of sickness that goes with aging--is a lurking threat to the program's financial stability.

Animal husbandry, cultivating fish and shrimp, raising fruits or flowers . . . all come within the scope of farmers' insurance. (photo by Vincent Chang)

The implementation of farmers' insurance can aid social stability in the countryside by reducing out-migration. (photo by Vincent Chang)

Incomes for rice farmers are relatively low; farmers' insurance has been long looked forward to.

Group medical centers are the first line of defense against illness in the more remote areas.

Chronic disease brought on by exposure to poisons and chemical pesticides is one of the "occupational hazards" facing farmers.

The farmers' associations have been instrumental in implementing the program.

The rapid aging of the farm population--and the high rate of sickness that goes with aging--is a lurking threat to the program's financial stability.

Animal husbandry, cultivating fish and shrimp, raising fruits or flowers . . . all come within the scope of farmers' insurance. (photo by Vincent Chang)

The implementation of farmers' insurance can aid social stability in the countryside by reducing out-migration. (photo by Vincent Chang)

Incomes for rice farmers are relatively low; farmers' insurance has been long looked forward to.

Group medical centers are the first line of defense against illness in the more remote areas.