On the eve of the return of Hong Kong, this "brightest jewel in the crown of capitalism," to socialist China in 1997, the territory's status has already been quietly changing: today it has become a "dragon pearl"--a guiding light illuminating the path ahead for the mainland's 1.2 billion "heirs of the dragon." From "bright jewel" to "dragon pearl," will the Pearl of the Orient lose its luster? And how will its radiance change?

In the height of Hong Kong's hot and humid summer, the territory is just entering the final countdown to the 1997 handover. But that is a political matter.

"On the economic side, the 1997 effect has long been apparent in Hong Kong. Economically, Hong Kong has already returned to China," says C. J. Lee, director of the First Institute of the Chung-Hua Institution for Economic Research.

According to statistics, mainland China is now Hong Kong's largest trading partner, its largest export market, and, it is generally inferred, its largest source of capital; as for the funds invested in the mainland from Hong Kong over the years (including some funds from Taiwan and Japan), they are estimated to approach US$100 bn, ranking first among foreign investments in the PRC. Three-quarters of Hong Kong's factories have moved north into Guangdong Province or further afield. So one can say that most Hong Kong businesses have already moved their assets "inland" as they put it, into China, and the structure of Hong Kong's economy has shifted from traditional export-led manufacturing to an entrepot economy serving the manufacturing base on the mainland. It is inextricably linked with the economy of south China's Pearl River delta.

British capital gives way to Chinese

For Hong Kong's economy to be dependent on the mainland seems perfectly logical: over the past decade, the Pearl River delta has quickly risen to prominence on the world economic stage, and when these cousins who speak the same Cantonese dialect become business partners, it is quite natural that close links should grow between them. Furthermore, Hong Kong and Guangzhou are only 160 km apart (the same as the distance between Taipei and Taichung), and with the Kowloon-Canton Railway, the Guangzhou-Shenzhen expressway and the newly completed Guangzhou-Shenzhen high-speed railway, the journey between them takes less than two hours, and the route spans the Shenzhen special economic zone. With Zhuhai's Sanzao International Airport and the Macao International Airport now operational, Hong Kong, Macao, Shenzhen, Zhuhai and Guangzhou are linked into a "Greater Hong Kong conurbation" or "Hong Kong-Guangzhou twin urban area," and it is only a matter of time before the six million people of Hong Kong are absorbed into the 67 million population of Guangdong Province.

Not only that, since China and Britain issued their Joint Declaration in 1984, confirming that Hong Kong will revert to China on 1 July 1997, the internal balance of forces in Hong Kong's economy has undergone a quiet transformation. The old-established British capitalist trading houses such as Jardine Matheson, Hutchison Whampoa, Wheelock, the Hong Kong and Shanghai Banking Corporation and the Swire Group saw a poor future for themselves in Hong Kong without the protective umbrella of the British Empire, so some began to sell off shareholdings and subsidiaries, or even to gradually pull out. At this point, the capital which the PRC had rapidly accumulated since the implementation of its reform and liberalization program flowed into Hong Kong in large quantities to buy up these assets, in order to "put the Hong Kong public's mind at rest and support Hong Kong's economy."

After the Tiananmen massacre in Beijing in 1989, Hong Kong was in a state of general anxiety, and property prices slumped. Chinese capital not only stepped in to fill the gap, but actually drove prices up again, maintaining the appearance of an economic boom. Currently, mainland and other Chinese capital (including funds from Hong Kong and from major Southeast Asian conglomerates owned by ethnic Chinese) is taking an ever-greater share, and the thousands of mainland-invested companies are now extending their activities from service industries such as property, finance and trade, into Hong Kong's large-scale infrastructure projects. Thus the interests of Chinese capital are deeply implanted in the territory of Hong Kong, and will become a leading force in its future economy.

Success or failure will be China's

The influx of Chinese capital into Hong Kong has inevitably brought with it the habitual vices of inefficiency, corruption and waste common among mainland enterprises, thus eroding the base of Hong Kong's reputation for clean government and the rule of law. From 1993, to rein in China's ballooning money supply, Beijing implemented a dracon-ian "macroeconomic adjustment" under which bank lending was strictly limited. This action also brought a slump in Hong Kong's econ-omy, with falling property prices and stagnant consumption, and unemployment rose to over 3% while inflation stayed at the high level of 9% for several years running. Ordinary people felt the pinch, and economic growth dropped below 5%, to take last place among the four "little tiger" economies. At the same time, erosion of Hong Kong's manufacturing base and the drain of middle-class talent through emigration casts the greatest shadow over the territory's economic future.

Judging from various economic indicators, compared with the stable and orderly past, "Hong Kong's economy has been going downhill throughout the last few years." Observing from the perspective of a Hong Konger, Citi Hung, managing chairman of HK Polling and Business Research Consulting Company, is particularly sensitive to this change.

However, although there is no concealing the negative effects of China's growing influence over Hong Kong in the run-up to 1997, the colony has also profited as China has reaped the rich benefits of its reform and liberalization program over the last ten years. Companies around the globe have moved from initial doubts and a wait-and-see attitude to gradual acceptance, and China has come to be widely seen as a place on which the hopes of the whole world for the manufacturing base and consumer market of the 21st century are focused. As China's prospects have improved, in the eyes of foreign companies Hong Kong has gained greatly in value for its convenience as a gateway to China and as a forward base from which to gain entry to mainland markets.

According to research by Professor Y. C. Jao of the University of Hong Kong's School of Economics and Finance, the number of international manufacturers setting up an "Asia-Pacific regional operations center" in Hong Kong as a springboard for investing in the mainland has not declined, but has actually grown. In foreign companies' minds, it is only to be expected that after 1997, administrative efficiency in Hong Kong will decline and that clean government and the rule of law will suffer--this is a necessary evil of any dealings with China. But foreign businesses worry less about the 1997 effect than about Hong Kong's rising prices and operating costs.

Li Chang-yi, director-general of the ROC Ministry of Economic Affairs' Medium and Small Business Administration, who worked in Hong Kong for many years, has also observed that Hong Kong and foreign business people are actually very sure that after 1997, Hong Kong's own economy will indeed continue to go downhill. But the pace of modernization and regularization in the mainland economy is accelerating, and between these two opposing forces, "business people are betting that the mainland will come up faster than Hong Kong goes down. Finally both will hit an acceptable point of balance, and the Hong Kong and mainland economies will really merge."

The efforts of 100 years

Hong Kong is valued as a gateway to the mainland, and the mainland will also be enriched by Hong Kong: after China takes back Hong Kong and these two great economic entities combine, the PRC will have the world's second largest foreign exchange reserves (some US$130 bn), will have a total trade volume in excess of US$600 bn, and will leap into fourth place among the world's exporting nations (behind the USA, Germany and Japan). The honor of Hong Kong's position as the world's largest container port and Asia's greatest financial center outside Japan will also accrue to the ancient imperial land of China.

Of course, with the development of mainland cities such as Shenzhen, Zhuhai and Shanghai, in the future Hong Kong will face stiff competition from within China itself. But Citi Hung believes that with its world-class financial, transhipment, telecommunications and information infrastructure, its tradition of the rule of law with clear allocation of powers and responsibilities, and its highly entrepreneurial spirit, Hong Kong is not likely to be outstripped by Shanghai or other cities within the next five to ten years. Furthermore, a liberal, international environment is the secret of Hong Kong's success, so that after 1997, the Chinese authorities will do their best to maintain these advantages, and will not put this highly westernized golden goose in the same coop as their own home-grown fowl.

"Previously, as residents of a British colony, Hong Kongers were the people in the capitalist world with the best understanding of mysterious China; after Hong Kong returns to China, they will be the group among the Chinese who best understand the outside world." C. J. Lee earnestly hopes that Beijing will cherish and use wisely Hong Kong's position as a "dragon pearl" and avoid squandering the fruits of its hundred years of toil as a colony.

[Picture]

The Cities of the Pearl River Delta

[Picture Caption]

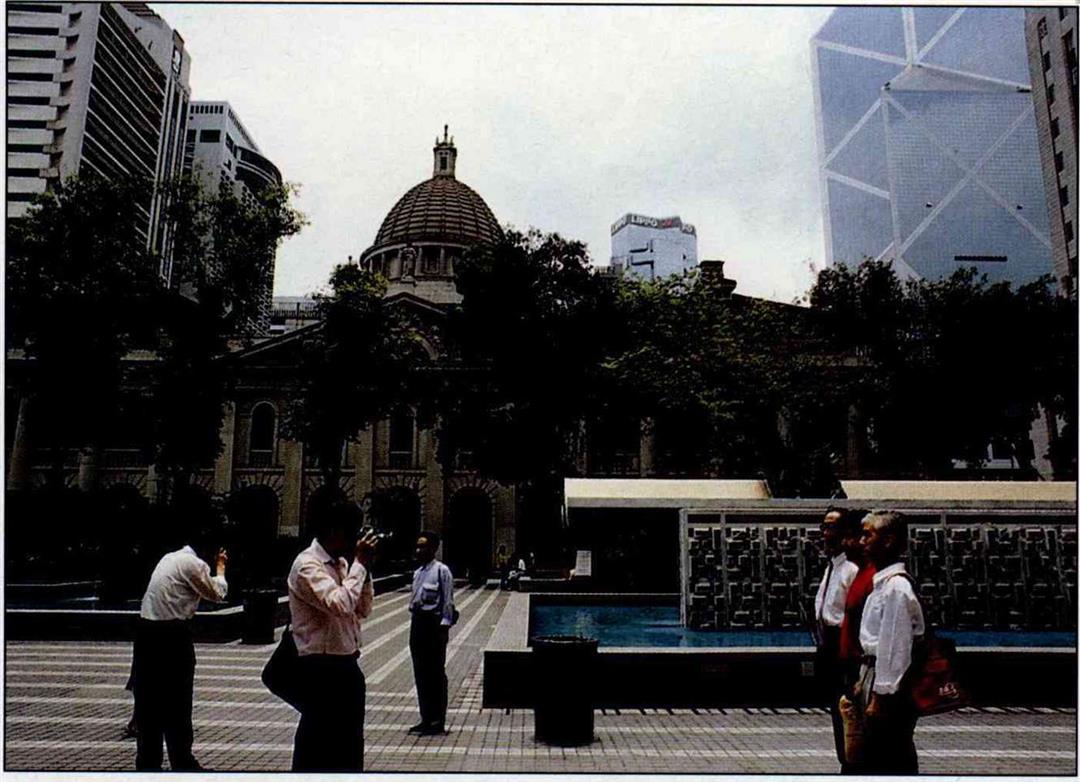

Visitors to Hong Kong from Beijing always remember to have their photo taken in front of the British-style Legislative Council building in Statue Square. (photo by P u Hua-chih)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)