What then is the main point? After its passage, in the big picture, what will be the impact on the R.O.C's overall financial environment? In the little picture, what about the ordinary depositor? Sinorama specially interviewed Chen Mu-tsai, director of the Monetary Department at the Ministry of Finance, for a detailed analysis.

Q: It seems everyone's attention has been on underground investment. The Legislative Yuan almost didn't pass the bill over this. Has there been a loss of direction?

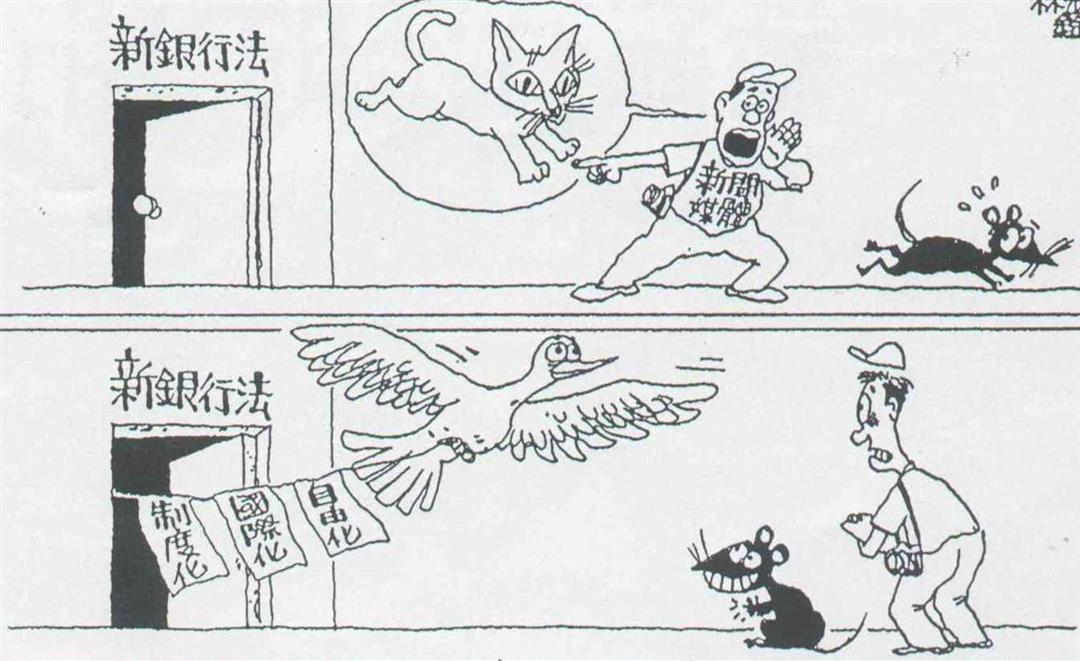

A: The spirit of the amendments was to encourage financial liberalization, internationalization, and systemization. Because underground investment companies touched on the interests of many people, everyone focused on article 29 and buried the main points. In fact, section I of article 29 was only added by the Ministry of Justice after the bill passed the cabinet. With all the uproar, it seems that the amendments were aimed at underground investment. In fact, the amendments have their own purpose. Thus, public opinion is certainly misdirected.

But the effect isn't all bad. It has brought policy on the underground investment companies into the open, and people have begun to take the problem seriously.

Q: In that case, what are the main points? Will there be a major impact on the financial environment?

A: The most important is opening up establishment of private banks. But the amendments also mandate strict management to protect depositors' interests and financial order. For example, Article 25 stipulates that no individual may possess more than 5% of the stock to prevent overconcentration of control, monopolies, or manipulation.

As for banks' capital and financial structure, there are clear stipulations. For example, the ratio of capital and risk weight assets must not be lower than 8%, determined by referring to international practice. On the one hand this can make the financial system sound and on the other match internationalization. Because in the future banks will want to open branches abroad, international standards are necessary.

For a sound financial system, the amendments have also stipulated the requirements for the responsible persons and officials of the bank.

Another important point is to encourage liberalization. Thus, Article 41 eliminates all upper and lower controls on interest rates for deposits and loans, and only stipulates that these must be clearly posted to allow customers to compare, increasing competition among banks.

This time the amendments also broaden the scope of banking service. There has been added that "other related services may be undertaken after approval from central-level governing institutions." Flexibility has been greatly increased; the government can give the banks authority to develop new services and increase financial products. Expanding the scope of services is not just for commercial banks; it includes savings banks, investment and trust companies, and foreign banks. The latter can now under-take personal savings, long-term loans, and trust services. This is also to accommodate liberalization and internationalization.

The last main point is to straighten out financial discipline and maintain order. The most important in this area, I think, is "emergency punishment powers." According to Article 61, these powers indicate that when a bank's services or financial situation deteriorate, and they cannot pay debts or are damaging the interests of depositors, the Ministry of Finance can order a full or partial halt in operation or send people to supervise or take control or take other steps, even restrict the directors from leaving the country.

Q: At the time of the Tenth Credit Cooperative scandal, didn't the government have these powers?

A: That's true. But the method was different. The government could order a halt in operations, but if it wanted to supervise or take control it needed the approval of the stockholders or the members of the society to empower the Ministry of Finance to empower a banking group to take over. The process is difficult and can lead to delays.

Therefore, after the amendments were sent to the Legislative Yuan this time, the following was added to Article 62: "When the central governing bodies send persons to supervise or take control, it is necessary that the powers of the stockholders, directors, or supervisors be entirely or partly terminated." In this way the Ministry of Finance's power's are clear and we can dispense with the relevant stipulations of the company law.

Therefore, though it seems that with the opening of the establishment of private banks, things are free, there are explicit rules of the game. If management is inappropriate, the Ministry of Finance must protect the interests of the depositors.

On the other side, the depositors must be aware. Like the underground investment companies, people have to keep in mind that if they take the risk they must suffer the consequences. If a bank goes under, the government will not support it 100% as in the past. Deposit insurance systems across the world only compensate to a certain degree. If the given bank has taken insurance, then the compensation is up to NT$1 million at most.

That which most concerns people is probably the problem of the underground investment houses. Basically, we clarify the nature of the illegal acceptance of deposits by these companies, and make the punishment for violation much heavier. In the past, Article 29 clearly stipulated that "non-banks must not undertake banking services." But as to what "taking deposits" constituted, that was unclear. So the Ministry of Justice suggested we make Article 29 more clear.

Punishment was changed from "less than five years in prison and/or a fine of NT$750,000" to "between one and seven years imprisonment and an NT$3 million fine."

Q: Is this strong enough?

A: Of course opinions differ. In ROC criminal law, aside from bodily injury, most punishments are not heavy. The longest for most economic crimes is seven years. Not to mention that the director of the banned institution must be personally responsible for all its debts.

Q: Many fear that government-run banks will be too uncompetitive vis-a-vis private banks, and will be the first to collapse. What is your view?

A: The government banks have polished their functions with Taiwan's economic development. Their bases of service, experience, and scale are considerably large, and will not collapse at the first blow. Naturally, under competitive conditions, state-run banks must change to survive. While permitting private banks, the government must promote privatization of existing banks and establish a "public financial institutions management law" to increase flexibility in salaries, personnel, and structure.

Q: I've heard this is the largest scale change in 14 years. Why do some criticize the law as obsolete already? And what areas are left to be considered in the next revision?

A: This time a total of 28 articles were amended and five added. All were fundamental, key amendments. I don't believe it was obsolete. Naturally, there is a need to endlessly evolve.

We've considered that next time the scope could be even larger. The structure of the banking law was set in 1975, combining commercial banking, savings banks, speci alized banks, and investment and trust companies in a single law. This is quite complex, and not easy to clarify. The law rigidifies and new changes can't be put in. We hope that the law can be separated into different laws in the future.

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)