The game has ended like a fleeting dream. Now that the dream has vanished, these questions are still worth close examination.

In February America's CBS television came to Taiwan to film a program on Taiwan's stock market euphoria. Sure enough, the moment they'd gone the share price index went into a downward spiral and it has now shed 10,000 points. Looks like that program's going to be put on ice for a while!

The sudden rise and fall of Taiwan's stock market has not only given the foreign media a sense of unreality, but Taiwan's shareholders (one in six of the population) feel their fleeting dreams of riches have gone up in a puff of smoke too.

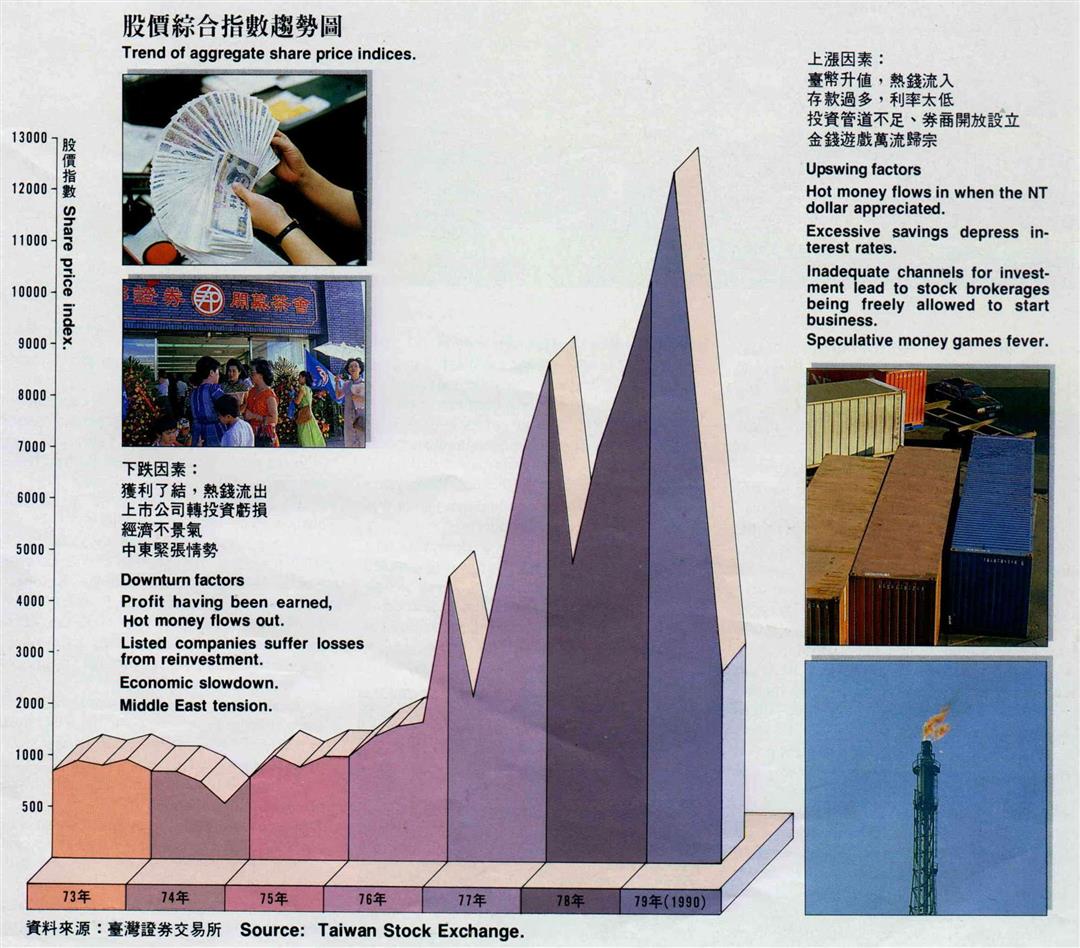

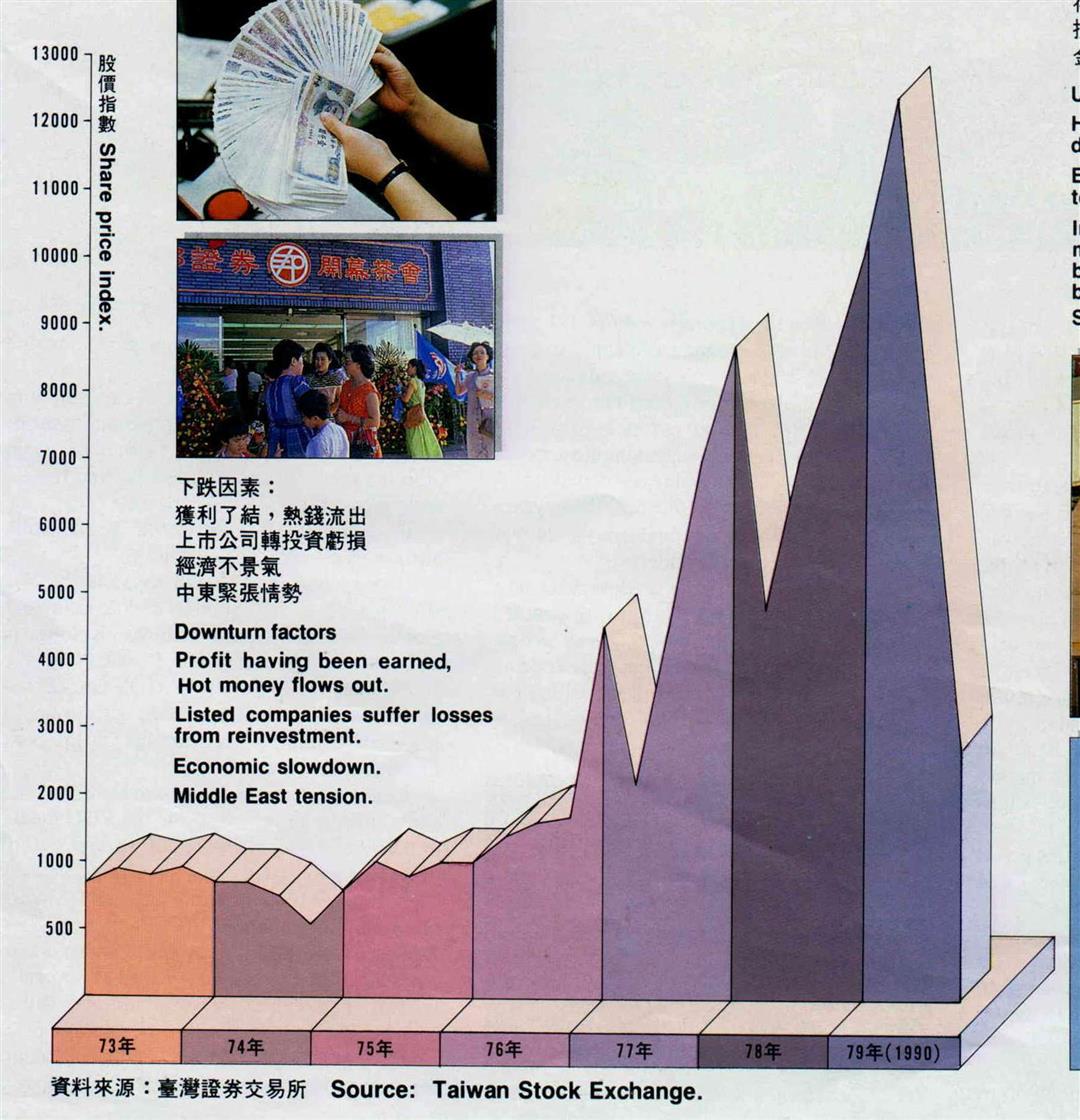

The Taiwan stock market index started climbing fast in 1987, and by February 1990 it stood at an historic high of 12,682 points. Since then it has steadily declined until by mid October shares had lost 80% of their value, and daily transaction volume had plunged from NT$200 billion, third highest in the world, to current levels of around NT$20 billion.

In this wealth redistribution process, education or position is of no avail. Everyone from manufacturers, businessmen and big shareholders in quoted companies, as well as enterprise managers, have fallen victim to the same fate.

A survey of managers in local large-scale industries carried out in September showed that, of those who had invested in Taiwan stocks only one in ten had shown a profit, three in ten were even, and the rest were losers.

The steady fall in share prices due to continued bearish sentiment has led many investors simply to put share prices out of their mind. Brokerage trading rooms and VIP saloons are largely deserted, "and you're less likely to encounter taxi drivers listening to stock market reports as they tear through the traffic," quips one newspaper reporter.

But the stock market is still in business and there are people who turn up on the dot day by day.

"One woman client told me she wouldn't know how to pass the time otherwise; she'd feel guilty just sitting there without placing an order," sighs Core Pacific Securities Senior Vice President K.M. Ling with a shake of the head.

"The winners have carried off the booty," maintains Wealth Magazine editor in chief Hsieh Gin-ho. As economist Wang Tso-jung says: the big players have been cut down to size, the small players have been cut to pieces. Every day Hsieh Gin-ho passes a brokerage and feels "they're like a cinema audience who won't go home after the film has ended."

And no wonder, for the last three years when buyers made money and everybody was a winner were just too wonderful.

The question is, will the stock market take off like that again? This is not just of concern to those lingering in the brokerages or people stuck with overpriced shares, but is even being quietly mulled over by newcomers waiting for the index to fall to 1,500 points before buying in.

To find answers, why not first examine the reasons for the last boom.

Was it just the indelible Chinese gambling instinct? Some prefer this simple reason; and in some foreign media Taiwan has been pilloried as an "island of greed." And there's something to it.

But those more experienced in economic history aren't content with this.

"America in the '30s and Japan in the '70s both played money games, and Britain and France had share price bubbles as long as 300 years ago," points out President of the World Economics Society Bert J. Lin. From an historical viewpoint, money games are a stage any country passes through on the path to prosperity.

Celebrated American economist J.K. Galbraith, in an interview for the ROC media in October, also attributed it to the nature of capitalism. "This is a recurring cycle of capitalism, and in America we've had ten years of speculative euphoria."

So in the '90, it was the Taiwan stock market's turn to heat up--with the world's highest per capita account holder ratio, cost/benefit ratio and share circulation rate.

Norman Yin, chairman of the banking department at National Chengchi University, states even more directly, "Taiwan's latest wave of money-game fever was the result of economic successes and problems accumulated over the past 40 years."

From 1952 to the present, Taiwan has had an average economic growth rate of 8.7% per year, and with the population's cautious mentality its savings rate has been the highest or second highest in the world.

Most of this money entered the financial system via banks, credit companies, the post office and credit cooperatives, causing aggregate national savings to reach NT$2,930 billion by November 1986, equal to one year's gross domestic product. This was also the first time the share price index reached 1,000 points, and from that moment it began to shoot up.

Meanwhile Taiwan's expanding trade surplus helped ROC foreign exchange reserves to rise sharply from US$2.2 billion in 1980 to US$76.7 billion seven years later; of this, some US$20 billion was hot money flowing in in anticipation of NT dollar revaluation.

During this period money was steadily accumulating but without sufficient investment channels. Bank interest rates also sank to historic lows, "money had no value," and so sizeable investment funds flowed into the Tachialo and Lucky Six lotteries, underground investment houses, real estate and the stock market, boosting share prices.

"The share price index reaching 12,600 points was due to a massive influx of investment in search of profits since other money games were coming to a halt or being out-lawed," Yin says. The well-known British weekly The Economist observed: "Taiwan is choking on its own success."

Well, will the stock market ever regain its 12,000 point levels of the past? And if so, how much longer must we wait?

Some estimate late 1991 at the earliest, others say another three years at least, while still others put it at five years. Take your pick.

"If we take the example of advanced countries, following West Germany's stock market crash in 1968 it took 14 years to reach a new high; Swizerland's stock market crash took 24 years to recover; so I think Taiwan will need 10 years minimum," says Hsieh Gin-ho.

This may sound unbelievable to a lot of people. Didn't the Taiwan stock market crash in July 1987 and September 1988, yet recover right away both times?

"Both those crashes were occasioned by external stimuli," Norman Yin observes. The first crash came as the Ministry of Justice Investigation Bureau had its first talks with underground investment houses, and also coincided with Wall Street's Black Friday; the second crash came when the Ministry of Finance announced the reimposition of stock transaction income tax. But since Taiwan's trade surplus was still expanding and the NT dollar still appreciating, there was no slackening in the cash inflow sustaining the share market. Once the storm had passed, share prices rose to new peaks in the next few months.

The current market setback, on the other hand, is due to internal economic factors. For instance, the April 7 fall of over 600 points, the index's biggest single-day loss ever and the last goodbye to the 10,000 point level, came one day after investors learned Taiwan's trade balance in March had shown negative growth for the first time in 6 years. The 510-point drop on May 18 also came a day after the NT dollar was devalued by NT$1.1 against the US dollar, causing a massive out-flow of hot money.

The main reason why bourses in advanced countries take so long to recover to new highs after a crash is that, following the damage done to the whole market by a euphoric rise, governments establish new codes of practice and enforce new regulations to deal with shortcomings, thus bringing the stock market to maturity. In a mature stock market share prices generally reflect long-term benefits to shareholders, and rarely give rise to euphoric bubbles. A new peak is only reached after years of economic growth when the shares of quoted companies have really reached that value; or else, as in the case of Japan this last time, when share prices are sustained by an inflow of hot money on the international market.

"Between its initial establishment and reaching full maturity, any stock market must pass through the phases of manipulation and market fragility," Frank Yeh observes on the basis of the normal market development model. "Last year and the year before, the Taiwan stock market was going through the manipulative and market fragility phase, but now that ought to be a thing of the past."

As he makes clear, the NT dollar's exchange rate has stabilized against the US dollar, and the Ministry of Finance is shortly going to revise the Securities Exchange Law and put a stop to insider trading, while allowing foreign institutions into the stock market; all this reduces the chances of artificial pumping up of share values and makes the stock market healthier. After this lesson, investors will act with greater caution. "The Taiwan stock market is unlikely to see the speculative euphoria of the past two years again, and it will become a mature market along the lines of London and New York," Yeh states.

But at the same time, others take a different view.

"The Taiwan stock market's settlement system is unhealthy, and unless it is improved, share prices may rise sharply again next spring," says Eiki Kiu, assistant to the director at Taiwan Security Company.

In contrast to the system in Japan, he notes, where share purchases are usually based on "full settlement," the Taiwan stock market has adopted an "excess settlement" system. Under the first system you are only entitled to buy shares you can actually pay for in full, but under the latter system, during a combined selling and buying transaction you only need pay the difference in price. "This allows people to buy and sell shares without making full payment, and thus acquire a large share-holding for very little outlay." Eiki Kiu believes that reforming the settlement system is essential for a healthy share market, otherwise "even if the bubble has burst today, more deluded speculators will come along later," he says.

Norman Yin also thinks that unless we can remember the lessons and thoroughly revamp the stock market we may very well face a third or fourth market slump, and as it veers from one giddy rise to the next crash, the market may never achieve normal operation.

He points out that from an efficiency angle he wouldn't completely agree with adopting the full settlement system, but shares must be traced back to their owners. "When shares are transacted they should be given a code number so that we can trace which shares each person holds," he maintains. In the past when the market was bullish, directors of quoted companies would hand over their shares to agents to sell on the side, then buy them back when the price dropped. If such a system were adopted, it wouldn't be possible to get away with that sort of thing.

Prosecution of insider trading, tracking down rumors, and supervision and management of brokerage houses must all be strictly enforced; the scale of the stock market--the number of companies quoted on the stock exchange--must also be further increased for the market to become healthy.

"The government should take advantage of the slowdown over the next two years to consolidate the stock market and set up proper regulations." Norman Yin suggests that whereas consolidating the stock market when share prices are high could depress market sentiment and easily cause a backlash from investors, to do so now would be like an enterprise improving its organization at a time of economic slowdown in order to be ready to meet the next upturn in the economy.

What of the present? The government has already taken action. Premier Hau Pei-tsun has stated that the government wants to ensure a healthy stock market, not rescue it. The Ministry of Finance has also firmly turned down suggestions from certain deputies and businessmen to lower the securities transaction tax so as to stimulate a recovery in share prices. Instead, regulations are being revised to encourage financially sound companies to list their shares on the market and to allow foreign institutions to enter the market, as a viable means of nudging the local stock market towards full maturity.

These days no one hangs around the stock exchange any more, businessmen have returned to their long neglected work, office workers have gone back to their offices and workers to their factories. People seem to have woken from their common delusion of instant riches.

Like a dream, the money game has ended and we are coming to our senses again. Despite the fact that some people are still clinging to hopes that the next stock market boom will set a new high, the majority of one-time investors are rapidly adjusting and returning to their own business. To their reserves of energy, dedication and flexibility that created the "economic miracle" and the "Taiwan experience" they now add the financial experience and investment lessons gained from the stock market's ups and downs, as they once more get their noses back to the grindstone.

The traces of our dreams can guide our way towards adulthood.

[Picture Caption]

Was the stock market's dizzy rise and sudden crash just a fleeting dream of riches? (photo by Diago Chiu)

When the stock market was bullish, the brokerages were packed and everyone climbed aboard the money-making bandwagon; even college students held club meetings to discuss the state of the market. (upper photo from Sinorama files; lower photo by Vincent Chang)

After the stock market crashed money was scarce and real estate prices felt the pinch. (photos by Huang Lili)

Trend of aggregate share price indices.

Downturn factors Profit having been earned, Hot money flows out. Listed companies suffer losses from reinvestment. Economic slowdown. Middle East tension.

Upswing factors Hot money flows in when the NT dollar appreciated. Excessive savings depress interest rates. Inadequate channels for investment lead to stock brokerages being freely allowed to start business. Speculative money games fever.

Aihsin instant lottery tickets take Taipei by storm in the latest manifestation of money games. (photo by Shao Jui-chin)

Will the stock market rise to new peaks again? Doubtless only the Prosperity Deity knows the answer. (photo by Vincent Chang)

When the stock market was bullish, the brokerages were packed and everyone climbed aboard the money-making bandwagon; even college students held club meetings to discuss the state of the market. (upper photo from Sinorama files; lower photo by Vincent Chang)

After the stock market crashed money was scarce and real estate prices felt the pinch. (photos by Huang Lili)

Trend of aggregate share price indices.

Downturn factors Profit having been earned, Hot money flows out. Listed companies suffer losses from reinvestment. Economic slowdown. Middle East tension.

Aihsin instant lottery tickets take Taipei by storm in the latest manifestation of money games. (photo by Shao Jui-chin)

Aihsin instant lottery tickets take Taipei by storm in the latest manifestation of money games. (photo by Shao Jui-chin)

Will the stock market rise to new peaks again? Doubtless only the Prosperity Deity knows the answer. (photo by Vincent Chang)