Case 1: Mr. Chan, thirtysomething, is in the videotape business. Although he is still a "snail without a shell" (a person who does not own his or her own home), he remorselessly pays NT$-17,000 per month to the bank for a car loan. Pointing at his new Ford Scorpia sedan, worth a million NT dollars, he says proudly, "Driving an imported car at 30--that fits with my life plan!"

Case 2: Miss Chang, about 40, works in the Mercedes Benz dealership in Nankang. With a body covered in designer clothes and cosmetics, a trip to Europe costing over NT$100,000 is a de rigueur annual expense. If you ask about her small loan from the bank which will never be paid off, she shrugs her shoulders, unconcerned, and says: "Can I wait until I save up enough money, when I'm so old I can't even walk, before I go travelling again?!"

Case 3: Mr. Chan is a section chief in a government bureaucracy. Five years ago, taking advantage of the vogue for employer guaranteed loans, when interest rates were a paltry six percent, he took out an NT$600,000 consumer loan to play the stock market. When the market took off, he invited his friends out to celebrate, going to luxurious piano bars, and tossing around NT$1000 bills without a second glance. Unfortunately, the stock market later suffered repeated setbacks. Who knows where that NT$600,000 loan went? All that's left now is the monthly payment of principal and interest of six or seven thousand NT dollars, and the day when it will all be paid off seems to be in the very remote future . . . .

The popularization of small loans: Cases like these are occurring all around us every day. Some people are extolling the American style of consumption of "play now, pay later." Some crave money, and are unwilling to bow to the conservative tradition of "slow accumulation of wealth," so they gamble in investments and money management. Whatever the origins, the spirit of "having the courage to borrow from the bank" is the same. In particular, from December of last year to April of this year, 15 new banks opened their doors. This really ignited a war of "personal consumer financial products," such as: the "two-generation parent-child home mortgage," the "double-happiness new bride's low-interest loan," the "just-married new husband's loan," the "tax-time tranquility loan," not to mention all kinds of travel loans, automobile loans, and so on. . . . And these small loans, except for car and home loans, do not require the guarantee of any collateral.

New products have been coming out in a steady stream, and each is highly inviting. With regard to the aforementioned newlywed low-interest loans, a certain bank, to go along with its grand opening, stipulated that any person newly married within a three month period prior to or after the bank's grand opening need only provide verification of continued employment in the same place for three years, a total joint income with the spouse of at least NT$500,000 per year, and a guarantor working in a government institution, and that couple could take out a "marriage transition loan" of NT$300,000 just by showing their marriage license or application form.

You could have a really fantastic wedding with three or four hundred thousand dollars, but with a three year term loan at 9.25% interest, the newlyweds would have to deal with a monthly payment of more than NT$9,000 in principal and interest. For a household for whom everything is just getting underway, this is no small burden.

If you can borrow the money, why not? Even though that's the way it is, within two months of operations this bank gave out 50-6O such loans, indicating that their first-wave assault was rather successful. "Among the applicants were bank employees, reporters, photographers. . ." says the director of that bank's consumer finance department. This product is targeted at major personal events in the course of a life, so it is easily adaptable to "popularization" in a mass market.

"Popularization" permits the broad mass of consumers, who rarely have anything to do with banks except for depositing savings, to get the idea that, "if there is money to be borrowed, then why not borrow it?" And the variety and flexibility of the advertising assault for the new products is a key reason why people are hard pressed not to be seduced.

In terms of the "transitional home loans" which many newly opened banks intend to push, the amount of the mortgage approved by the banks is ordinarily larger than the clients need or apply for. In the value system of the past, one should never borrow money that is not absolutely necessary, "but now things are different, especially for those people who want to invest in financial instruments," says David Han, senior manager of Credit Review at Bank SinoPac. When the investment situation was looking bullish, having a large pile of money on hand that you could throw in at any time was quite convenient. As a consequence, within the approved amount for these housing loans, the client could be given a one-year fund. If the fund remained untouched, it would not be necessary to pay interest, and interest would only be calculated from the time the money was put to use (though the interest rate was always one point higher than the average housing mortgage). Moreover, when you had money and wanted to make a payment on the loan, no matter what the amount, you could have it entered against the balance at once.

Personal clients become the new favorites: Although there seem to be a vast amount of new personal financial products in order to "make the consumer public prosperous," these naturally are inescapably part of a bank's business operations. This can be explained in terms of the modern financial supply-demand relationship.

"In the past banks always thought of consumer loans as being aimed at scattered individuals, with so many people and a complex variety of matters involved, yet with the volume being pitifully small. Also, owing to their status as public institutions, banks could not adjust the interest rates upwards according to the costs involved, so they always felt such loans didn't pay," says Dolly Yang, Senior Vice-President and General Manager of the Consumer Finance Department at the Dah An Commercial Bank. On top of this was the fact that banks did not readily trust individual borrowers, and there was no collateral, so the risk was rather large. It is said that the rate of bad loans for the Bank of Taiwan's "overseas study loans" reached 20%, and many of those in the industry learned a lesson from this.

As a result, "unless one ran across the special situation of a bank's funds being especially soft, so that it was necessary to quickly channel them back out, banks had a very low willingness in the past to undertake personal consumer loans, and most dealt mainly in commercial loans," says one Taipei City Bank section chief frankly.

But today the situation has changed. First, existing large enterprises have established deep relationships with certain long-established banks over a long period, and the new banks are in no position to win them over. Further, after the explosive development of Taiwan's capital market, enterprises could get even cheaper capital from the stocks and bonds market, greatly reducing their reliance on banks. Thus it was even more difficult for new banks to share in this shrinking pie. As for the small and medium enterprises, which have always found a poor reception when they go hat in hand asking for loans, the new banks did not dare to take them on because such businesses were always springing up and failing, and the risk is too great.

So on the one hand it's hard to get businesses. On the other hand, with economic growth and the rise in personal incomes, the ordinary consumer has become a most welcome customer in the eyes of the banks. "This represents a major transformation in the view of banks," says David Han. In the past, the banks mostly had a "pawn shop" mindset. They were only willing to make a loan if the client could offer some collateral. But in these days of fierce competition, they can't help but change their tune -- no matter whether or not there is collateral, the applicant need only have the ability to repay and a good credit history to be a good client. Thus, with the stimulus of the new banks targeting this new market, there have been major gains these past few months.

Rapid increase in credit cards: Another area of great potential, which has already begun to change the traditional consumer habit of "only spending what you earn," is the increasingly popular credit card. The National Credit Card Center (NCCC) of the ROC, which had been established for eight years before finally cracking the "one million credit cards" barrier last October, suddenly surged to giving out 200,000 new cards from January to March of this year alone. "It looks like the two million mark can be reached this year," says Chan-Shaun Chu, Vice-President of the NCCC, with the sense of satisfaction that comes with "water flowing into its proper channels."

The figure of two million credit cards issued by NCCC is, of course, but "a minor wizard faced with powerful wizard" compared to Japan's population of 120 million people who nevertheless own more than 130 million credit cards of various kinds. Credit card issuing banks which thus believe that Taiwan has a great deal of room for growth are using all kinds of discounts and prizes to strongly push the cards and to stimulate consumer desire to keep a credit card in hand for consumption.

At the same time, in order to more broadly promote the "play now, pay later" consumer mindset, some banks are promoting "rollover credit" for credit cards--if the person is unable to pay for one month's purchases when payment time rolls around the following month, the cardholder can pay just five percent, and can allow the remainder to accumulate. In any case, the banks are perfectly happy to collect the interest, which can reach more than 15% per year.

"Rolling credit"? or "rolling debt"? From the consumer's point of view, this kind of rolling credit "service" cannot but cause one to worry whether or not it will become a "bottomless pit of desire," and indirectly encourage people to consume beyond their ability to pay, thus piling debt upon debt. Will people become slaves to their "rolling debt"?

The vice-president and business manager of a foreign bank, Phee Boon Kang, explains it from the angle of the "rights" of the consumer. He believes that if the consumer has the ability and the desire to engage in "planned consumption," then the many types of loans and credit cards are merely "tools" provided by the banks, giving the consumer more choices. Consumers in advanced nations throughout the world have long enjoyed having these choices, and Taiwan consumers should naturally also have the chance to enjoy these services as early as possible.

"Those who become like 'drug addicts,' scrounging for a credit fix, and 'addicted' to rolled over debt, are really a small minority," points out Phee Boon Kang. For example, in 1990 the American VISA card had only a 1.2% rate of bad debts, well within the "tolerance range."

From another point of view, of course these services may be satisfactory for a time. But in the so-called advanced countries, including Britain, the US, Japan, and Australia, because the governments, banks, businesses, and individuals have all been encouraging each other to expand credit (loan volume) and have been consuming intensively, this has led to an exhaustion of financial capacity. The defects which were revealed in the current period of economic recession cannot but make one sit up and take warning.

Don't follow in the dust of the US and UK: Take Britain for example, in the 1980's, which was seen as the "decade of greed." With the economy performing well on the surface, housing prices took off. With everyone under the optimistic assumption that "tomorrow will be even better," huge home mortgages and car loans became topics to be proud of in social life.

Little did people expect that the economy was brittle, and an unprecedentedly severe recession set in. The unemployment rate, including that for high level positions, rose dramatically, and housing prices collapsed. Many people who had had stable incomes were laid off or took paycuts. Moreover, bank interest rates showed a large increase, and monthly payments thus began to exceed people's budgets. With the general stagnation in the housing market, it also wasn't easy to unload property.

The result of rolling debt over into more debt, according to statistics in The Economist, has been that the banks, in the capacity of the creditor, repossessed more than 80,000 homes in 1991, and the new poor are filling the streets. Going from luxury to poverty, not to mention being left with a pile of debt and accumulating interest, the public mood turned sour and the government was forced to design an "emergency relief plan." Thereafter, when banks advertised housing loans, by law they had to add an announcement warning of the risks.

The situation in the US is quite similar. People unable to repay their mortgages had to sell at a large discount to repay their debt. And banks suffered large losses because the properties they repossessed in their status as creditors dropped in value as collateral because of the overall collapse of housing prices. In the last ten years, nearly 2,500 financial institutions in the United States have gone out of business, of which many were brought down in just this way. Indeed, even world-conquering Japan has been troubled of late by the increase in the number of young people who have gone "credit card bankrupt." With instructive examples so close at hand, if Taiwan consumers blindly follow along, will they end up in the same ruts?

Some recently released statistics are worrying enough: According to the Bureau of Auditing, Statistics, and Accounting, in the five years from 1987 through 1991, the domestic savings rate fell 8.5%. In the last two years it has fallen even more dramatically, to below 30% (last year the savings rate was 29.88%). Moreover, in January of this year the total value of imported consumer products was more than NT$24.95 billion, surpassing the total value of imported capital equipment (NT$24.3 billion), indicating that people's interest in productive investment can't keep up with eating, dressing up, and playing. Finally, though the new banks have been open no more than four or five months, they have already issued more than NT$70 billion in loans, which is really amazing firepower.

Taiwan's situation is not the same: Do these signs mean that Taiwan's consumer structure is changing? "Accumulating wealth through hard work" is nothing but an anachronistic virtue. Even terms like "spending only as much as you earn" show "a lack of skill at financial management." In their stead, are we going to have "play now pay later" wisdom like "if I like it, what's wrong with it?" or "borrowing money shows that you know how to get things done"? In regard to this, people in financial circles generally express optimism, and say that Taiwan, whose main problem is having too much money in foreign reserves, is in a completely different situation from the West.

"If the symptoms in the West are that secular overspending has exhausted the financial lifeblood, then Taiwan's problem is high blood pressure," metaphorically explains Liu Shou-hsiang, an associate at the Chung Hua Institution for Economic Research.

"Many people look at the debilitating results of long-term over consumption in the West, and are afraid Taiwan will take the same path," elaborates Mckinney Y. T. Tsai, Director of the Division of Planning and Regulation of the Bureau of Monetary Affairs at the Ministry of Finance. "In fact, the US savings rate is less than five percent, while ours is still 29.88. Also, the US has a huge trade deficit, while Taiwan has an enormous surplus."

Besides different economic situations, economists argue that the habits of local banks, social structure, and traditional values are all different from the West. This means the new consumer values will not smash the old for the time being.

Earning money is still more interesting than spending it: "Looking at the short term, the new consumer values have not come into vogue," points out Hou Yung-hsiung executive vice-president of the I-shan Bank. Although the new banks are all anxious to "recirculate" the NT$10 billion they have in hand, they are still reserved when it comes to consumer loans, and do not yet dare to play it too loose.

It's hard to change banking habits. And the same goes for mass consumption habits. "Don't look at how fast the number of credit cards is rising--more than 50% of those are rarely used," says Chan-Shaun Chu. Many people only use their credit cards when they go overseas to make things easier for themselves. As for the number who might want to use "rolling credit," the proportion is still very low at less than five percent.

"Consumer behavior cannot stand alone, and you have to see whether the overall social environment is accommodating," notes Bank Sinopac's David Han. Under the current limitations of the domestic traffic conditions, public construction laws and regulations, and the housing situation, the consumption quality of the people has not necessarily gone up, and the scope for consumption is really limited.

Further, people in the banking industry say that many people in Taiwan apply for loans under the rubric of "consumer loans," but in fact they really spend very little on consumption. Most of it--more than 50% -- is invested in financial markets in the hope of making a quick killing.

"Chinese still have a strong 'sense of crisis' when it comes to money," says Professor Chang Chun-hsiang of the Banking Department at National Chengchi University. Taiwan's retirement, unemployment, health, and handicapped welfare and insurance systems are not as comprehensive as those in the West. So most people put aside a little "old age capital." This attitude of putting a little away for a rainy day cannot be changed overnight, and "very few people are likely to blow their old age money by anticipatory spending," he concludes.

Don't forget to "keep aware of danger in a time of tranquility": Nevertheless, when you factor in the craze for money games which has been rampant these past few years, one can't help but--besides rolling one's eyes and clucking one' tongue--adopt a wary attitude of "closing the window before the rain" of persistent gambling, bottomless desires, and a lack of self-control "floods the room."

Mckinney Tsai says that, while being happy about the new consumer financial products that banks have been putting on the market in an endless stream, people must not forget that pearl of Chinese wisdom: "Keep aware of danger even in a time of tranquility." Economies have weaknesses, and personal income will not necessarily be eternally stable. Now the US, Europe, and Japan have all set up institutions to educate the public about appropriate concepts of consumption and borrowing. For the consumer public in Taiwan, poised on the edge of "anticipatory consumption," this is a topic which deserves a great deal of thought.

No matter what, in the face of consumer seduction, the public can always remind itself: Although banks are categorized as a service industry, they are definitely not "charitable organizations." As you look at the wave after wave of enticing loan ads from the new banks, as your desires are peaking, be sure to factor into consideration your own abilities and unknown future risks. and leave yourself a little room to maneuver.

In the end, the real modern person who is truly good at financial management and enjoying life will keep a close eye on the purse strings and make careful plans. Isn't it a rare pleasure indeed for the modern consumer to be able to say, "there's no debt hanging over my head."

[Picture Caption]

Fifteen new banks opened within four months, providing consumers with many new channels through which to borrow money. Have you felt the seduction? (drawing by Tsai Chih-pen)

The ribbon cutting ceremonies at new banks have been a focus of recent news reporting.

(photo by Pu Hua-chih)

The new banks have been frantically putting out new ads pushing their special incentives and policies, stealing a lot of customers away from the older banks.

(photo by Diago Chiu)

Citibank offers drive through automatic tellers for the convenience of automobile drivers.

Buildings are getting taller, and real estate prices are correspondingly higher. The new banks are actively pushing home mortgage loans. Will this further stimulate housing prices?

(photo by Vincent Chang)

Many people want to sell homes, and even more want to buy. But when you think of how high prices and interest rates are, it's still better to wait and see!

The density of Taiwan's imported foreign luxury cars is among the highest in the world. But the number of people who are carrying loans to own one is not small. (photo by Diago Chiu)

Overseas travel is all the rage. Would you borrow money from the bank for a trip to Europe? (photo by Diago Chiu)

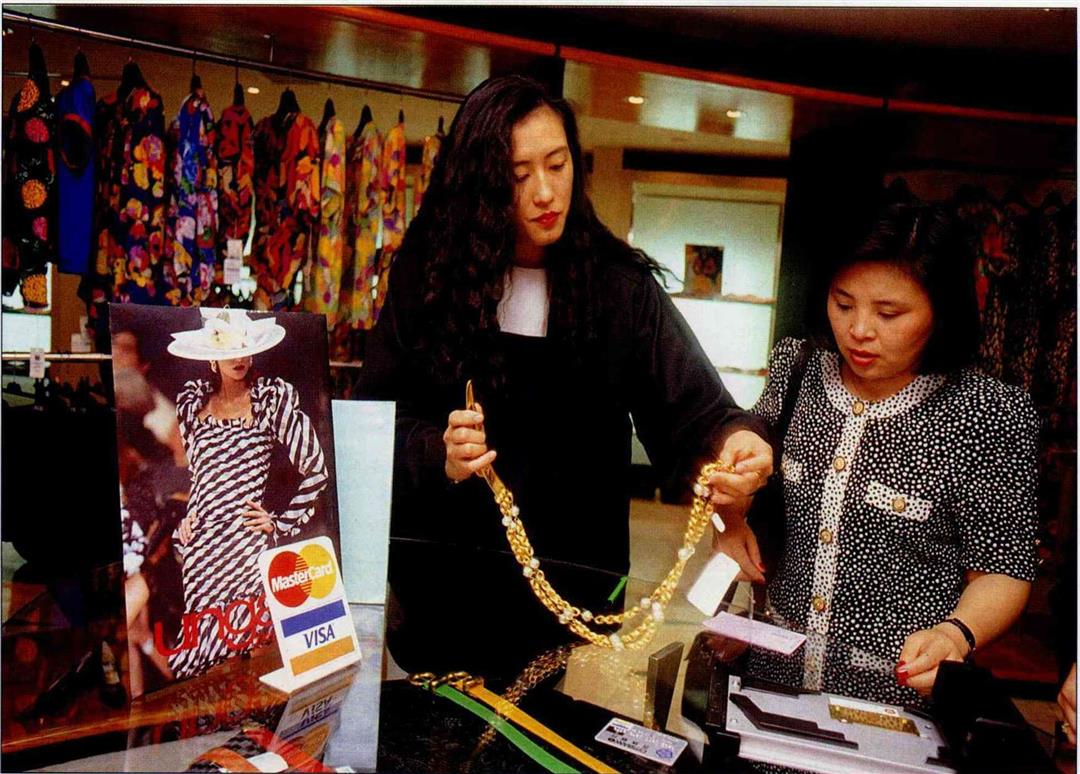

It's uncommon for shops to accept credit cards; most that do are elite boutiques. There are few channels to use them for consumer purposes.

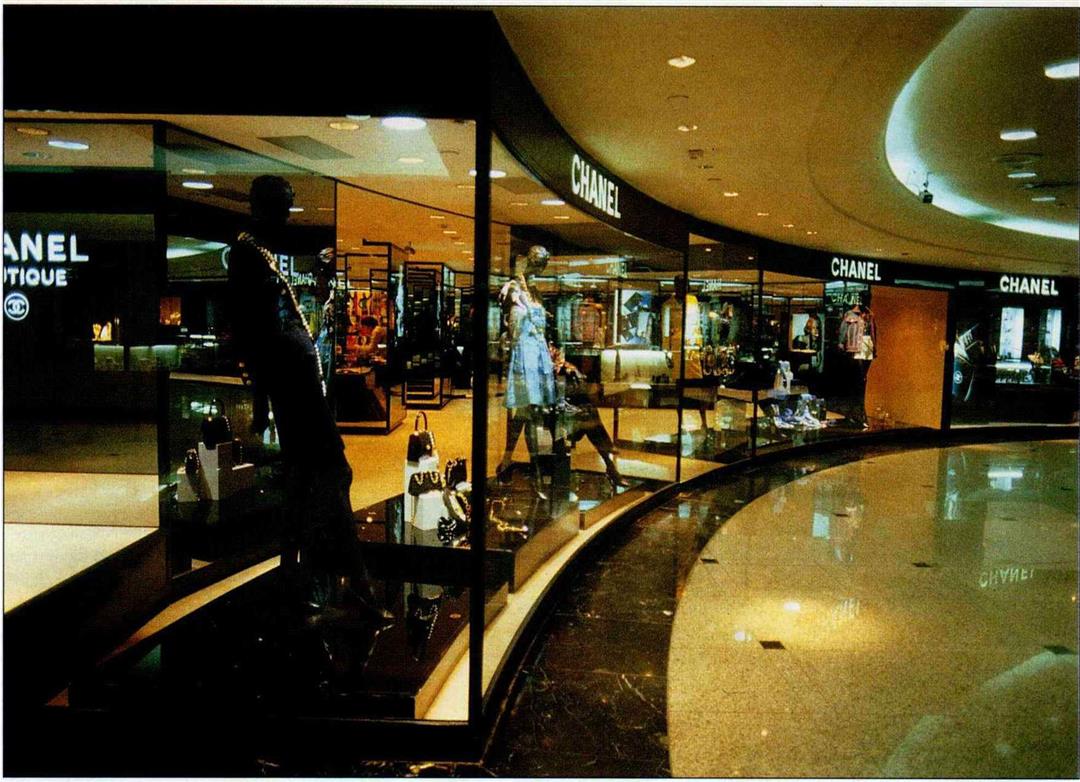

Taiwan has become a gathering place for name brands from around the globe. Some people are worried that the "new poor," clothed in designer duds but without a penny in their pocket, will grow out of this.

Getting rich the old fashioned way--by earning and saving: This has always been a virtue praised by Chinese.

The ribbon cutting ceremonies at new banks have been a focus of recent news reporting. (photo by Pu Hua-chih)

The new banks have been frantically putting out new ads pushing their special incentives and policies, stealing a lot of customers away from the older banks. (photo by Diago Chiu)

Citibank offers drive through automatic tellers for the convenience of automobile drivers.

Buildings are getting taller, and real estate prices are correspondingly higher. The new banks are actively pushing home mortgage loans. Will this further stimulate housing prices? (photo by Vincent Chang)

Many people want to sell homes, and even more want to buy. But when you think of how high prices and interest rates are, it's still better to wait and see!

The density of Taiwan's imported foreign luxury cars is among the highest in the world. But the number of people who are carrying loans to own one is not small. (photo by Diago Chiu)

Overseas travel is all the rage. Would you borrow money from the bank for a trip to Europe? (photo by Diago Chiu)

It's uncommon for shops to accept credit cards; most that do are elite boutiques. There are few channels to use them for consumer purposes.

Taiwan has become a gathering place for name brands from around the globe. Some people are worried that the "new poor," clothed in designer duds but without a penny in their pocket, will grow out of this.

Getting rich the old fashioned way--by earning and saving: This has always been a virtue praised by Chinese.

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)