Is the high-tech financial sector any safer than the windblown sands? And how can people's boundless desires be prevented from getting out of control?

The 1990s have been described as an era of high-speed money management. When one opens the newspapers, pages full of financial advice and information on all kinds of mutual funds emphatically tell people the importance of making provision for the future and putting their capital to work: Parents should be worrying about an education fund to provide the millions or tens of millions of New Taiwan dollars they will need for their children's schooling from birth to possible graduate studies overseas, and white-collar workers should be worrying about the huge sums-said to be at least NT$16 million-which they will need for a reasonable pension after they retire in 30 years' time. Ordinary families in which the husband's and wife's combined monthly income is only NT$80-90,000 not only need to meet their mortgage payments, cover their childcare fees and pay for three meals a day; like Kuafu chasing the sun they should also be assiduously pursuing one financial goal after another, each higher than the last. (In Chinese legend, the overambitious Kuafu chased the sun, and after catching up with it died of thirst despite drinking dry two rivers and a marsh). Anxiety about and a thirst for money have become the everyday ailments of the late 1990s.

The magical power of numbers

Early this year, after much badgering from friends about how, if she couldn't manage her money properly, she could just "wait to be poor," hospital technician Ms. Li plucked up her courage and opened a share trading account with a securities firm. She describes her investment experiences of the last six months, which have left her unable to sleep at night: "First I bought financial shares, but then I saw that shares in electronics companies kept on going up, so I hurried to buy into those. Later I heard the NT dollar was going to fall, so I quickly ditched all my shares and bought US dollars instead. . . ." Most extraordinarily, when the price of gold recently kept hitting new record lows, at the urging of a colleague Ms. Li, who normally would never have so much as even thought of buying a piece of gold jewelry, went and opened a gold trading account.

An account book, a few lines of figures and symbols-financial products don't fill your belly or keep you warm, so aren't they far removed from real life? Yet these very same abstract figures relentlessly and concretely control the shifting emotions of millions of investors like Ms. Li. But can owning financial products such as shares, bonds, US dollars or gold really increase their sense of security and guarantee their dreams of growing rich? Following the financial turmoil which has sent foreign exchange markets and stock exchanges reeling throughout Asia over the past six months, it is surely time for investors to think again.

On 2 July 1997, following repeated attacks on its currency by international speculators, Thailand, one of Southeast Asia's four emerging "Little Tiger" economies, announced it was abandoning its attempts to protect the baht, and was adopting a floating exchange rate policy, to allow the currency to find its own level in the market. This sparked a wave of currency devaluations throughout Southeast Asia. At the end of June, the baht had stood at B25.88 to US$1; by late November, it had depreciated to B40 to US$1-a fall of over 50%. None of Southeast Asia's other three Tigers-Indonesia, Malaysia and the Philippines-came off unscathed: their currencies all fell by between 30% and 50%.

The news from the stock markets was little better. Ding Kung-wha, vice chairman of the ROC Securities and Futures Commission, points out that high rates of economic growth over the last decade or more have made Southeast Asian countries continued favorites with international investors; it is estimated that 20-40% of shares in each of the four Tigers' stock markets were in foreign hands. With the recent massive currency depreciations, to cut their losses foreign investors sold off their holdings, which they converted into US dollars to remit abroad. This caused dizzying falls in share prices.

Dragons chasing tigers?

For the past several years, the aura created by the high growth in the four Southeast Asian Tigers had diverted attention from problems such as high foreign debt, large trade deficits, budget deficits and flagging productivity. Thus exchange rate adjustments for their currencies were in fact predictable. But the storm was not discriminating, for although neighboring Singapore is known for its financial soundness and efficient monetary system, and has long ranked high in global competitiveness ratings, it was not spared. By mid-November, the Singapore dollar had lost more than 10% of its value. In a domino-effect sequence, the storm clouds also swept through the forex markets of Taiwan, Hong Kong and South Korea, which with Singapore are termed the four "Little Dragons."

Looking at Taiwan before the crisis arrived, the island's continuing export growth, successful industrial restructuring and consistently prosperous economy meant that by any criterion there should have been no reason at all for the NT dollar to depreciate. But sadly capital and finance are no respecters of national boundaries. The financial systems of countries throughout the region are closely interlinked, and no single country can close its doors and keep itself aloof.

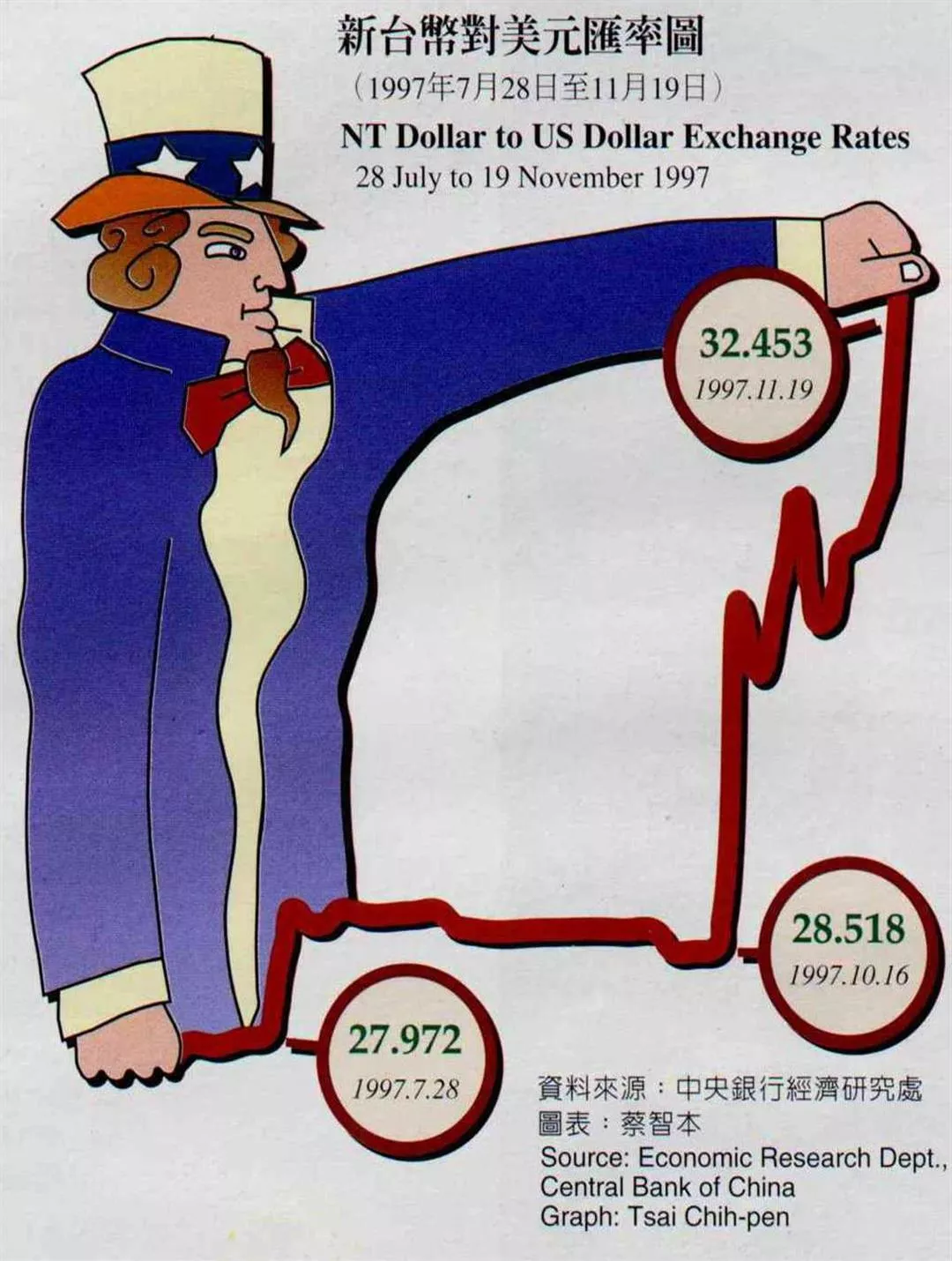

Since July, the value of the NT dollar has fallen by more than 15% against the US dollar. Particularly since mid-October, when the South Korean won became the latest target for devaluation pressure, fluctuations in the NT dollar have been unprecedentedly large, with daily swings of as much as NT$1-2. The currency trend is quite at odds with the real state of the economy, leaving many officials and academics open-mouthed.

"If the Korean won falls, the NT dollar has to move with it," says Philip Peng, Acer Incorporated's vice-president for corporate finance and investment management. He points out that industry in all Southeast Asian countries relies mainly on exports for its earnings, and currency devaluations boost products' price competitiveness in international markets. There is little duplication between the products exported from Southeast Asia and from Taiwan, and many Taiwanese firms have moved their production base into the region, so the devaluations in Southeast Asian currencies did not hit Taiwan too hard. But it is a different matter with South Korea. South Korean industries such as semiconductors, electronic goods, petrochemicals, plastics and steel are very similar to Taiwan's major exporting sectors, so a large devaluation in the won affects Taiwan's export competitiveness. Every country tries to protect its own competitive advantage, and this leads to a "devaluation race."

Looking to the future, the downward trend in the won is not yet over, and the air is thick with speculation and rumor. Of the four Dragons and four Tigers, the only one whose exchange rate is still pegged to the US dollar is Hong Kong. It now stands alone and exposed among East Asia's stricken forex markets, and seems sure to attract repeated attacks from international speculators to test its strength. If the Hong Kong dollar topples, with the territory's status as the monetary interface between the world financial system and the Greater China economic sphere, the risk for Taiwan should not be underestimated.

One tightly-knit system

With technological advance and the rise of the modern financial system, the financial network built up on computer networks by corporate entities such as banks, investment trusts and multinational companies is so closely interlinked that any movement affects the whole system. This network not only extends to all countries within the region, it also links stock exchanges, forex markets, bonds, futures and even real estate and other financial products into one tightly-knit system.

To take the Taiwan Stock Exchange as an example, in late July the Taiex index had just broken the 10,000 point barrier, but before the champagne corks had stopped popping the storm in Southeast Asian forex markets broke over it. To prop up the NT dollar, the Central Bank of China sold US dollars and bought NT dollars. This caused a sharp rise in market interest rates, and in effect drew money out of the stock market to support the foreign exchange market. As a result, within three months the stock market plummeted by almost 30% from its 10,000 point peak.

The same scene was played out in Hong Kong. In late October, as the Hong Kong government fought an extraordinarily bloody battle to support the Hong Kong dollar, not only did the Hong Kong stock market nosedive, it even triggered a "global crash" as the New York stock exchange fell with it and markets in other countries followed suit.

Polly Young, vice president in the administration department at foreign-invested Jardine Fleming Taiwan Ltd., which has a large clientele in Asia for mutual funds, says that currently international trusts generally treat a whole region as one unit, so that there are Asia funds, Latin America funds, Greater China concept funds and so on. When alarm signals come out of a region, small investors thousands of miles away cannot judge the economic strength of individual countries. To reduce their risk, they tend to simply pull their money out of the region altogether and move it somewhere safer.

To prepare for this enormous selling pressure, when share prices first start falling the fund managers doing the actual trading have to sell more shares than they would otherwise have done, and hold cash instead. This creates an additional downward pressure on shares which benefits nobody. Furthermore, with other markets collapsing, even if the situation on the Taiwan stock market is relatively optimistic, fund managers have no choice but to take profits to offset their losses in other markets.

"The only purpose of financial operations is to turn a profit. There's no such thing as moral or immoral, and no such thing as it being fair or unfair to hardworking individual countries or firms," says Ding Kung-wha, highlighting the pragmatic and unsentimental nature of the financial world.

The black hole of "virtual money"

Looking back on this financial earthquake of unprecedented duration, depth and breadth, and facing what Time magazine has described as "a new ugly phenomenon," many people cannot help wondering: What has gone wrong in this profit-motivated financial world? And what is behind the financial bubbles which rise and burst?

US columnist Joel Kurtzman, in his book The Death of Money, writes that the "megabyte money" which flows around the world at almost the speed of light on electronic networks has broken free of the traditional role of money. Management guru Peter Drucker goes further, saying that "virtual money" has no real economic function, and people do not buy and sell financial products in response to actual everyday needs such as investment, consumption or trade. Hence the market law of supply and demand ceases to apply. When it boils down to it, many inexplicable price movements are simply the reflections of the greed, unrealistic expectations and jitteriness of people today.

These insights seem to fit very well with the current out-of-control situation.

Taking the analysis a step further, Professor Lin Jeungyol of National Chengchi University's Department of Financial Management says that in the view of traditional economics, the "real economy" which toils away day by day, accumulating value little by little through production, and the "money economy" which produces no physical goods but works to generate interest and avoid risk by reallocating capital, "ought be entirely complementary, with each reflecting the state of the other." But unfortunately today they have become divorced from each other, and are moving further and further apart.

As Central Bank of China governor Sheu Yuan-dong puts it: "The industrial economy is the root, and the financial economy is the leaves and branches." But planting deep roots does not bring immediate profit, so most people have turned to grafting on leaves and branches to construct the illusion of prosperity. Hence the creeping tendrils and overabundant leaves spread wildly and aimlessly, becoming a cancer on the economy. When a storm comes they not only damage the roots; if the worst comes to the worst they may rip them out wholesale, wiping out years of hard work in a moment.

What is particularly unfortunate is that by the time governments began to take the menace of the ferocious financial monster seriously, its strength and hold over the real economy already far exceeded most people's imaginations.

The relative strengths of the "financial economy" and the "real economy" can be judged from the amounts of money each controls.

To take the ebullient month of July 1997 on the Taiwan Stock Exchange as an example, in just 26 trading days, totalling less than 80 hours of trading time, the total value of shares traded was around NT$5.1 trillion, equivalent to more than four times the annual budget of the ROC central government (something over NT$1.2 trillion for fiscal 1998). In other words, all the central government's expenditure on diplomacy, transport, education, defense and everything else for four years can be traded here in under 80 hours.

How is money "created"?

The torrent of money flowing through the stock market stirs up the impatience and yearnings of ordinary citizens and so incites still more people to try their luck by putting their money into this electronic black hole, thus giving the financial monster even more power to bite back and do harm. But the stock market is only a small part of financial activities. Forex markets, bonds, futures, and a constant stream of new "derivative products" which most people can make neither head nor tail of, keep on attracting people to feverishly invest.

Of the foreign exchange markets, Ding Kung-wha says: "In the 1960s the total value of foreign exchange transactions worldwide was six times the amount actually needed for international trade; in the 1990s, this figure has ballooned to 50 times!"

"Up until the 1960s, the world economy was driven by production; if you could make products, you could make money. In the 70s and 80s, as productive capacity continuously expanded, manufacturing profitability fell and marketing came to play the leading role, with control of brands and distribution channels the key to success. Today, competition is still more intense, and profits from both production and distribution are small. Only the rich earnings offered by financial operations are still attractive." This is how Ding Kung-wha characterizes the global trend.

Many conveniences are provided to make financial operations easier, and because the figures in investors' account books do not represent physical assets they can be moved in an instant. Also, easier and easier availability of credit, in the form of unsecured loans and margin accounts (either for buying on margin with borrowed money, or for selling on margin with borrowed shares), has allowed many people to grow accustomed to conducting transactions worth 10 times the capital they themselves put in.

In The Death of Money, Kurtzman uses the example of bank lending to explain how money expands. If a customer deposits $100 with Bank A, after deducting the reserve assets which government regulations require it to keep on hand (around 8% on average in Taiwan) the bank can lend out over $90; after this money circulates through the market, it is deposited in another account in Bank B, and Bank B can again lend it out in the same proportion. Simply by being deposited twice in this way, the original $100 has already grown to more than NT$200; and the same process can be repeated many times over. So much money "created" by lending means that investors can pay in advance for all kinds of luxuries, share prices and foreign exchange rates can go through the roof and property prices can rise by hundreds of percent, creating a mirage of prosperity. But it is a characteristic of the expansion and mobility of money that it inevitably vastly increases instability in the electronic economy; in other words, if the day comes when all accounts around the world have to "squared"-if all the debts of every person and every enterprise around the world had to be paid off immediately, the financial monster would shrink into a little mouse, and the illusion of prosperity would disappear in an instant.

Opportunities for speculators

Perhaps the mystifying instability of the financial world can be traced back to 1971. In August of that year, US president Richard Nixon was forced by a mountain of overseas debt, which made it impossible to maintain the value of the US dollar, to announce the abandonment of the Gold Standard. This broke the dollar's long-standing link to gold, by which US$35 could be exchanged for one ounce of the metal. Once the value of money was decoupled from the commodity on which it had previously depended, how should it be measured? How could reasonable exchange rates between different currencies be determined? These uncertainties, which have continued for many years, sowed the seeds of later global exchange rate fluctuations.

Unstable exchange rates have forced countries' central banks to make increasing use of interest rates to adjust and stabilize exchange rates: By raising interest rates they attract money into the country and so shore up the value of the currency, while by cutting interest rates they suppress rises in exchange value. Balancing exchange rates and interest rates is a delicate tightrope act.

But a change in a country's interest rates affects the allocation of all its resources: if interest rates are too low, money will flow out of the banks and into the market place where it will trigger price inflation; if rates are too high they raise the cost of borrowing for firms and depress the economy. Hence how far to raise or lower them is a great headache for central banks in all countries.

Whether for business people who have to continuously follow exchange rates to calculate their import and export costs, or retired people who live off the interest on their investments, movements in interest rates and exchange rates are a great source of extra worry. But such movements are just what speculators like best, for with luck and a sensitive nose for the market, even tiny movements in market rates can give them the chance to turn a profit by buying low and selling high.

Strange to say, for the market to operate efficiently requires the existence of speculation. As Professor Chiu Shean-bii of the Department of Finance at NTU's College of Management explains, the original meaning of "speculate" is "guess." Whether it be interest rates, exchange rates, share prices or the prices of any of the internationally traded bulk commodities, there is usually some difference between their current level and the level they "should" be at. People who are able to spot that difference and correctly predict trends can reap profits. Seen from this perspective, speculation is the lubricant of the market, which helps attract people into the market place, and also allows the price of any given product to quickly reflect its "true value." In this way it enhances the market's efficiency.

The black hand of speculation?

But where the danger lies is in the fact that the "true price" is often abstract or even non-existent. For example, from February to May of 1997, the Thai baht was under pressure from selling short by international speculators who expected it to depreciate. But at that time many economists supported the official position of the Thai government that the baht was not overvalued, and that the Thai economy was strong enough to support it. If the speculators had not gratuitously stirred up waves and persistently attacked the baht it might have come through, and the East Asian financial crisis might never have happened.

Lin Jeungyol comments that the most dubious aspect of international speculation is that speculators start by selling short, then put out rumors through the international media or multinational financial institutions. This is clearly a form of "insider dealing." He reveals that about a week before the NT dollar began to fall, people started putting out rumors on the Internet that this was about to happen, and this increased the sense of panic among the general public. The final outcome did indeed fulfil the predictions-or should one say "calls"-on the Internet, leaving people with the feeling that "there seemed to be concerted manipulation behind the scenes."

In a financial world without borders, in which "megabyte money" can be moved in an instant, such suspicions are extraordinarily difficult to substantiate. It would require close cooperation between all the countries involved, transparency of account movements and so on. The fact that there is only a very fine line between investment and speculation, and that motives are very difficult to discern, would make investigation even more difficult.

But whatever the motives, Lin Jeungyol notes that as soon as a large institution makes a comment, the information itself has a very strong suggestive effect, so that individual "hunches" (or malicious distortions) spread like wildfire and are transformed into shared market expectations. When panic in the market sparks a rush in one direction, no-one has the power to stop it-all one can do is to wait to pick up the pieces.

Mass hysteria?

Unfortunately panic and blind reactions are a major feature of the money economy. In The Death of Money, Kurtzman notes that the transfers of "megabyte money" around the world and the computer networks which transmit it are extremely "nervous": the slightest rumor may spark off a wave of hysteria. Peter Drucker also takes the view that compared with traditional money, whose value is clear, "virtual money" is not linked to anything real, so it is even more prone to fluctuations due to rumors and unexpected events.

The 27 October crash on the New York stock exchange is a case in point. Chiu Shean-bii observes that as the leading US stock market passed 5000 points, then 6000, then 7000, many people had been worried for some time, and were getting ready to sell and take their profits safely. But seeing so many more cautious investors who sold too early lose out on the continued substantial rise in the market, they had not yet taken the plunge.

But then the jitteriness prompted by the tenth anniversary of the 1987 "Black Monday," plus the massive falls in Asian stock and currency markets, caused huge numbers of investors to decide it was time to sell. This common frame of mind in the market caused a tumultuous day's trading, sending the Dow Jones index plummeting more than 500 points and creating a huge day's trading volume of 1.2 billion shares. In other words, although the US economy is currently in good shape and a far cry from its depressed state of 10 years ago, as panic spread through the stock market, irrational overreaction caused the "prophecies of doom" to be fulfilled.

But incredibly, just as when stock markets around the world were in a state of panic and consternation after New York's massive fall, the next day the New York market leapt by over 300 points, clawing back 60% of the previous day's losses. Even greater swings were seen on the Hong Kong stock exchange. On 28 October it fell by 13.7%, but the next day it recovered by 18%! These frantic movements which no stock exchange guru can satisfactorily explain seem to be adequately described only by the phrase "mass hysteria."

A vicious virtual world?

But if it was hysteria, can we look on it as a nightmare from which we awake to find the horror gone as if nothing had ever happened? From the point of view of the electronic networks which transfer billions around the globe, yes. But for the millions of individual investors who panicked and dumped their holdings, it may have caused real and irreparable harm.

Mr. Chang, who works for a state-oowned telecommunications company, is an example. Encouraged by a cable TV stock market investors' club, in August when the Taiex stood at over 9000 points, Mr. Chang took all his hard-earned savings of the past five years and bought 6000 Taiwan Semiconductor shares at the high price of over NT$150 each. When the market slumped in mid-October, seeing that the Taiex was set to fall below 7000 points, Mr. Chang admitted to himself that he "didn't have the stomach for this," and simply to escape from the throes of daily anxiety, sold his shares at NT$120. Thus all his savings of the past year were lost.

"Luckily my savings weren't that substantial, so my losses were limited," says Mr. Chang. He consoles himself with the knowledge that he did not fare as badly as his next-door neighbor, a teacher named Yang. She put in NT$4 million, including the whole of her lump-sum retirement payment. Chang saw her face go from bright and smiling to drawn with worry in just a few short months, as she lost NT$1 million. She had been unassuming and honest all her life, but now she could not bear the reproaches of her husband and children, and was on the verge of a nervous breakdown!

Are financial markets cruel and inhuman? As a regulator of the ROC's securities and futures market, Ding Kung-wha does not think so. Over the past few years, in response to pressure from inside and outside Taiwan, the island's financial markets have been moving quickly in the direction of diversification, liberalization and internationalization. For instance, after Taiex index futures were launched on the Singapore stock market last year, the long-delayed law on futures trading was finally passed in Taiwan. Although Ding Kung-wha is well aware of the high risks and high loss rates of futures operations, rather than leaving Taiwan products at the mercy of speculation on foreign markets, he would rather Taiwan should enter the fray itself to keep a measure of control.

The Securities and Futures Commission is planning to vastly increase the depth and breadth of the Taipei stock exchange. In the future, any approved foreign company will be able to issue Taiwan depository receipts (TDRs), and its shares will even be able to be listed on the Taiwan market, so giving local investors a greater diversity of choice.

Keep a cool head

In Ding Kung-wha's view, financial transactions do indeed have their irrational and speculative side, and can lead to the ruin of countless investors. Nonetheless, regulators "must not consider things only from the point of view of individual investors, but must consider the efficiency of the allocation of resources within our economy." He states that in a free, open market, capital will automatically flow into the most competitive sectors. High-profit, high-technology industries will attract investors, while the market will naturally turn its back on unprofitable, inefficient enterprises and industries, leading to the more efficient use of capital.

Furthermore, as investors grow more sophisticated and experienced, "direct participation" in financial markets, in which individual investors take risks themselves and can earn higher profits, is playing an ever greater role in advanced Western countries: shares, bonds, mutual funds and even options have all become part of the everyday life of white-collar workers. By contrast, "indirect participation" (e.g. by holding bank deposits which banks invest as they see fit-the depositor has little risk but also no chance of premium profits) are steadily losing ground.

"This is the worldwide trend, and we can't buck it." Ding Kung-wha says that most people can still choose to remain aloof and not go playing the numbers game, but if the financial sector continues to expand, and with possible inflation, in the end they will find themselves with inadequate spending power.

Looking at it that way, will people finally have no choice than to get involved in the precarious and irrational financial markets? Perhaps the answer is a reluctant yes. However, faced with a market filled with greed and inflated expectations, it is those who keep a cool head and resist rash impulses who will make the greatest gains.

Chiu Shean-bii, who subscribes to this point of view, comments that financial operations are nothing bad of themselves, but one has to maintain a calm and rational attitude, and rationality is built on knowledge and understanding. For instance, shares are a financial product requiring long-term investment to yield profits. As long as investors do not expect to get rich overnight, and are not swayed by short-term fluctuations, but make it their goal to accumulate high-quality shares, they should generally gain good yields over the long term. But people who worry at every change in the market and keep buying and selling, switching from one company's shares to another and from one financial product to another, will in the end not only earn little, but, more importantly, will also have wasted their precious time and effort and diminished their pleasure in life.

In an uncertain age, we could do worse than to remember the wisdom of the philosopher. In The Prophet, Gibran asks: "What is fear of need but need itself? Is not dread of thirst when your well is full, thirst that is unquenchable? "

Don't be afraid, don't be greedy-isn't that what the basic outlook of a modern investor should be?

p.34

In the wake of the financial crisis, the sun seems to be setting on the celebrated "Asian economic miracle" of the last two decades. How could this fail to be a worry? (photo by Diago Chiu)

p.36

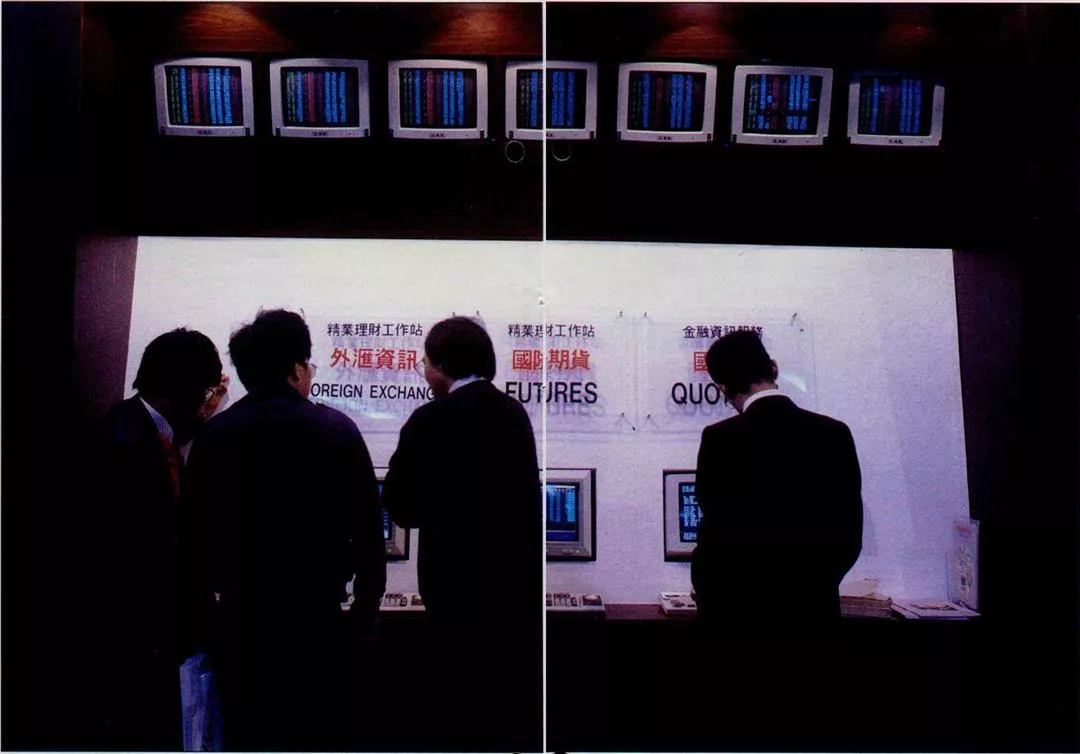

"Buy!" "Sell!" Financial markets are places where fortunes can be made and lost overnight. Their high risks and high potential profits attract people's basic gambling instincts. Pictured here is Hong Kong's futures exchange. (photo by Tsai Hsiu-ying)

p.37

Though huge, the financial system is fragile, with the slightest rumor sometimes enough to spark a crisis. Here account holders wait to withdraw their money during a run on local credit cooperatives two years ago. (Sinorama file photo)

p.38

The enormous sums they will need for their children's education are a worry to parents, and a focus of mutual funds' advertising campaigns. (photo by Diago Chiu)

p.39

NT Dollar to US Dollar Exchange Rates

28 July to 19 November 1997

Source: Economic Research Dept., Central Bank of China

Graph: Tsai Chih-pen

p.40

Credit cards of every description allow purchases to be made with just a swipe through a reader. The rise of such "quasi-currency" has further expanded the financial sector.

p.41

In the world of electronic financial trading, money has become something formless and intangible. Today it may be invested in US bonds; tomorrow it might be used for speculation in East European currenc

Credit cards of every description allow purchases to be made with just a swipe through a reader. The rise of such "quasi-currency" has further expanded the financial sector.

In the world of electronic financial trading, money has become something formless and intangible. Today it may be invested in US bonds; tomorrow it might be used for speculation in East European currencies. At the click of a mouse button it can be sent flitting all over the world, leaving little trace of its passage. (drawn by Pu Hua-chih)

The expansion of the money economy is bleeding the "real economy" dry. The hard-earned wages of farmers and factory workers are a pittance compared with the massive profits which can be earned in financial transactions.

When stock market bubbles burst, the property market, another major outl et for investment, is usually the first to be affected, leaving luxury mansions standing empty and unwanted.

An insatiable desire for money and property have made investment and money management a "necessary evil" for people today. How to avoid becoming obsessed with the ebbs and flows of the financial tide is a lesson everyone needs to learn. (photo by Diago Chiu)