Since the beginning of this year, Taiwan's stock market has been rising dramatically. In the first half of March, the trend continued, only to face a sharp downturn when news came out that an outbreak of foot-and-mouth disease would cripple Taiwan's pork industry. Were it not for the misfortune of the pigs, the influx of money and the succession of ever-higher peaks would have continued as people who had long stayed away from the market returned in droves. But there are a lot of variables at work in this boom cycle that make it different from the last one.

At the beginning of this year, the Year of the Ox, there was unusual activity in the Taiwan stock market. "It's the Year of the Ox, so the market sentiment should be bullish!" An elderly gent in the broker's office excitedly passes along what he has heard. This coincidence is well-timed: Is the Taiwan stock market, in the doldrums for seven years, finally heading for the big wave?

"This time I'll come out ahead."

Turn back to dusty memories of yesteryear, to the last boom in the market. Beginning in 1987, the market rose straight into February of 1990, when it crested at more than 12,000 points. But then-well, how can one explain it? Perhaps "it's number was up." Anyway, with no substantive changes in the political or economic environment, the index plunged steadily. Within eight months it had lost 80% of its value, falling to just over 2000 points. For the next six years, the Taiwan stock market remained slow.

"That was really a 'Cultural Revolution' for the Taiwan stock market," says Faunas Kuan, vice president of Fubon Securities Investment Trust, referring to the devastation. He recalls, his face darkening, how many classmates in those days, just graduated from National Taiwan University, were sent for a tumble or even ended up in jail.

However, "capital is like water; it has no memory and even less patience," says one official at the Securities and Exchange Commission (SEC), and people are again attracted to money games. Those who didn't catch the wave last time are anxious to play this time around. Those who enjoyed the sweet taste of success the time before want even more this time. Those who lost out seek to reverse their humiliation. There are also many people who-despite having a "once bitten, twice shy" attitude and frothing at the mouth at even the mention of the stock market-still can't help but be tempted to jump into the fray whenever they see the index climbing.

"I'm not going to be so greedy this time. When I've made enough I'll 'get off the bus early.' That way I won't end up losing it all!" "Last time I put up all my stocks as collateral for a loan, expanding my credit too fast, so in the end I was forced to sell out at rock bottom prices. This time I've learned my lesson. I'm using my own money, so if the stocks fall, I'll just hang on to them and it won't matter." At brokerage houses, where punters hang around keeping an eye on computer monitors and placing orders, they chat about this and that and everyone has something that they learned that they want to share with others. But can the experience and the lessons learned in the last boom-and-bust cycle really guarantee that the market will not fall this time? Nobody dares to say.

Bull run

Looking at current market conditions, beginning on January 6th, the bourse entered an upswing characterized by surging demand. By March 17, the market had been rising for 10 consecutive weeks. The index had risen by more than 1600 points, or 23%. Compared to the same period last year, the market was up 80%.

Besides rising values, trading volume has increased dramatically. Though trading is permitted only three hours each day, more than NT$150 billion circulates in the market. Sellers have already made money and are taking their earnings. Buyers are optimistic and believe prices will continue to rise, so, with a get-rich-quick dream in their hearts, they put in orders.

Both buyers and sellers are happy these days, and the expression "it looks like it'll have to fall, but still it doesn't" precisely reflects the recent incredible strength of the stock market.

Josephine Peng of Intellects and Co, CPAs, who has long been seen as a key source of advice for small and medium businesses, is a case in point. She says that stocks are definitely overvalued, and are not worth the prices being paid. Yet, after she sold off her agricultural stock at the beginning of March for a price of just over NT$100 or so per share, the price continued to rise. Many of her friends laughed at her: "I told you not to be so timid. Now look, you have tens of thousands less than you could have had!" After hearing a lot of comments like this, despite her own advice to others that "it's not necessary to try to earn every possible penny," she can't help but consider whether or not to get back into the market "to take the opportunity to make up for lost money."

This seemingly never-ending upswing left many experts with their jaws hanging open. However, just as everyone was jumping on the bandwagon, on March 19 foot-and-mouth disease broke out among hogs and spread quickly. The impact included the fall of stocks related to animal husbandry and food processing. Then came rumors that China, dissatisfied with Taiwan's hosting of a visit by the Dalai Lama (who is a symbol of Tibetan independence), would stage threatening new military maneuvers. Investors began to panic.

Beneath it all, however, it is gratifying to know that many professionals have been urging people not to over-react. "In the medium and long term, the trend is still upward. While there will be setbacks in the course of the rise, the market will take a turn for the better later on," predicts Chen Wen-ching of Yuan Ta investment consultants.

The confidence of the experts is based on the powerful underlying factors behind the recent surge.

Industrial recovery

In fact, "there are discernible reasons for this upswing, so it shouldn't be considered as too far out of the ordinary," argues Thomas M.F. Yeh, director of the Economic Research Department at the Council for Economic Planning and Development (CEPD).

In terms of economic trends-the so-called "fundamentals" of the stock market-Taiwan business has been very vibrant for the past few years. After slipping for a number of years, the trade surplus recently rose sharply. Last year, Taiwan had a trade surplus of US$14.7 billion, almost twice that of 1994. This figure is even higher than in 1989, at the height of the boom period.

The recovery in exports indicates that the threat of domestic deindustrialization has for the most part abated, and economic restructuring has been effective. The rise of the petrochemical, computer, and electronics industries suggests that Taiwan has already staked out a place for itself in the future world economy. As far as the stock market is concerned, the increase in exports means more capital at home, becoming a powerful force reinvigorating the bourse.

In fact, in both late 1994 and the latter half of 1995, the Taiwan stock market index surpassed 7000. Unfortunately, it fell due to a series of events: President Lee's visit to the US, the consequent deterioration of relations between Taiwan and mainland China, China's threatening missile tests, and the turbulent presidential elections in Taiwan. These caused people to buy US dollars, sucking capital out of Taiwan, and stopping the market. Fortunately, by the third quarter of last year the situation had calmed, various industries recovered, capital flowed back in, exports held strong, and overall economic growth rose from 5.1% in the first quarter to 6.6% in the last quarter.

In other words, "the Taiwan stock market accumulated a great deal of energy, and we can see this wave as 'compensatory growth' extending over the last two years," avers Yin Nai-ping, a professor of finance at National Chengchih University. "Taiwan's economy returned to the starting line and took off again."

Years to build, a moment to collapse

Despite the fact that the "fundamentals" can account for the rise to some extent, and, with several crises having been weathered, people are confident that there is little to fear, the real force keeping the market booming has, in the end, been the "capital situation" of accumulated funds.

Looking back, the tension between the two sides of the Taiwan Strait caused the caused the market to fall, but it also brought an unexpected bonus. To stimulate a recovery from the economic downturn of that time, and to stabilize "indicators of economic confidence" like the stock market, since August of 1995 the Central Bank has five times lowered the deposit reserve ratio for banks, causing interest rates on savings to fall. Thus, while in the last boom-and-bust stock cycle, when the market turned down, money fled to savings accounts, recently interest rates have been too weak and people are too unwilling to leave their money sitting around in the bank, so people have been ready to jump back into the "lovable albeit fearsome" stock market.

From last year to the present, the M2 (an indicator of money supply in fixed deposits) has continually fallen. According to the Central Bank, in February alone the banking system saw an outflow of NT$26 billion from fixed deposits. As market fever grows, the amount of money that is "restless at sitting around" will inevitably grow.

Further, when the missile crisis was at its peak, the "stock stabilization fund," an NT$100 billion appropriation managed by the CEPD, entered to support the market. At that time, banks and insurance companies required to participate were sour-faced about it; today, these institutions are flush with cash and there are smiles all around. The stock stabilization committee ceased work in the middle of last year, but its impact remains. Funds at all levels of government, such as those for health insurance, pensions, and even the Straits Exchange Foundation, all are looking to get into the stock market. The fever for "public fund management" is just beginning.

All together now: speculate!

Fubon's Faunus Kuan suggests that this fundamental conceptual change will have a positive and far-reaching impact on the development of the stock market. He notes that in the past government officials thought of the stock market as "cannibalism." It was equated with speculation and a get-rich-quick mentality. However, nowadays, especially with government funds getting tight and interest on government deposits not enough to cover expenditure, the upside of money management through the market has become apparent, and the image of the stock market has been "rehabilitated."

Government institutions are of course still very cautious in their activities. For example, the labor pension fund, with over NT$100 billion, has invested no more than NT$100 million in the stock market. In other countries, institutional investors often have more than half of their funds in stocks. Were all government funds to reach this level, that would mean nearly another NT$100 billion entering the market, which would undoubtedly provide a huge boost.

Besides an influx of capital from Taiwan, in recent years, thanks to the policy goal of "financial internationalization," Taiwan's stock market has been opened wide to foreign investors. Given the current wave of incoming investment, foreign money has pushed the tide even higher.

Thomas Yeh of the CEPD points out that since last year, when the Ministry of Finance allowed direct foreign investment in the stock market, the upper limit on foreign ownership of the market has gone from 10% to 25% of total market value.

The spark for the recent wildfire of foreign investment came last April. At that time, the US investment firm Morgan Stanley, guided by the ROC government, announced it would list more than 70 Taiwan firms in their "emerging markets free index," which is provided worldwide as a reference. (It formally did so in September.) Foreign institutional investors, who had previously known little of Taiwan, were drawn in, and the prices steadily rose.

According to the SEC, more than 200 foreign institutions have received approval to invest in Taiwan's stock market. Last year, the cumulative amount of foreign capital poured into the market was more than US$14.5 billion (about NT$400 billion). Indeed, even when the cross-Strait situation became tense, and many Taiwan people were thinking about how to get their money out of Taiwan, foreign institutions, relying on their specialized knowledge, continued to buy big, becoming a major stabilizing force for the market at that time.

Even today, when the stock market looks overvalued and local securities firms are selling out of what looks like a perilous situation, still foreign institutions are plowing in. One fund manager says, "The confidence foreign investors show in the Taiwan stock market boggles the mind!"

Is the pie big enough?

The internationalization of the Taiwan stock market has smashed the previous "mini-mart" situation of the last boom period. Given the expanded size of the market, plus the overall conceptual shift, some local experts have concluded: "Don't worry! The speculative money games of the past will never rise from the grave now."

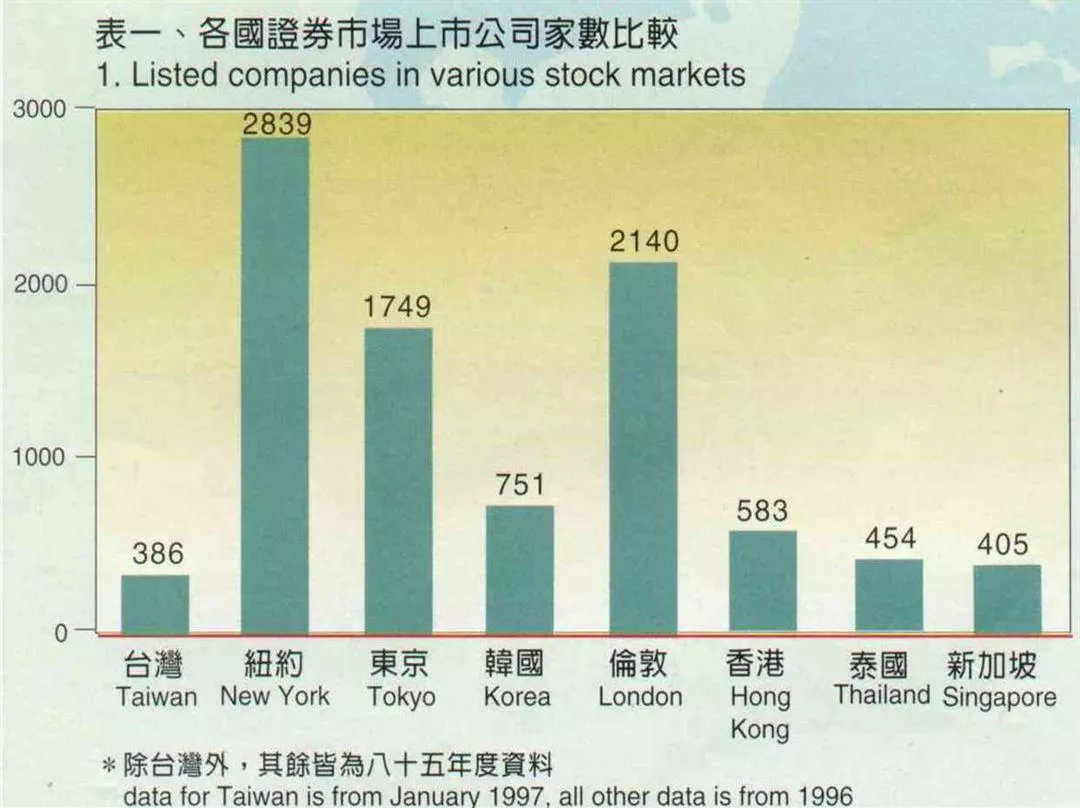

In terms of market size, by the end of January, there were 386 listed companies. This is more than double the 181 there were in the last boom year, 1989. Moreover, there are another 85 firms selling under the newly established "over-the-counter" procedures, whose requirements are less rigorous. With more firms, the stock pie is bigger, and can absorb more people taking a slice. With many more places to put one's money, people no longer chase the few "hot tips" like a swarm of bees.

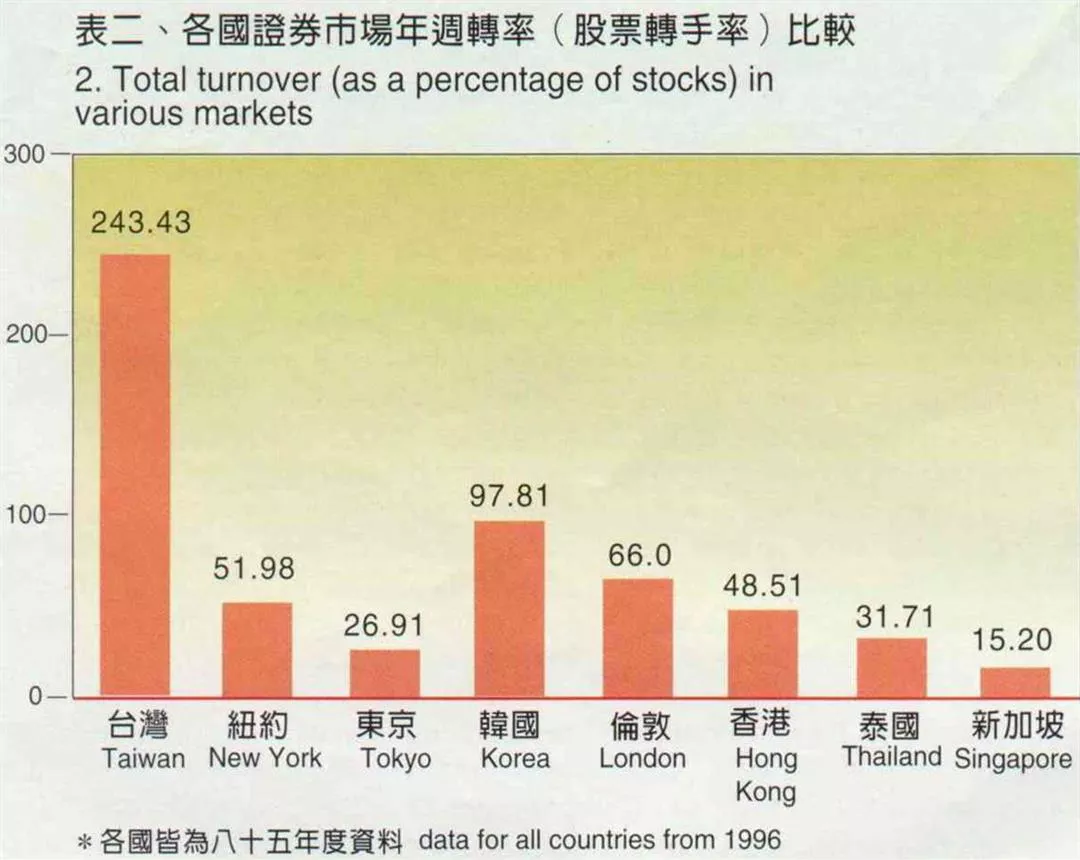

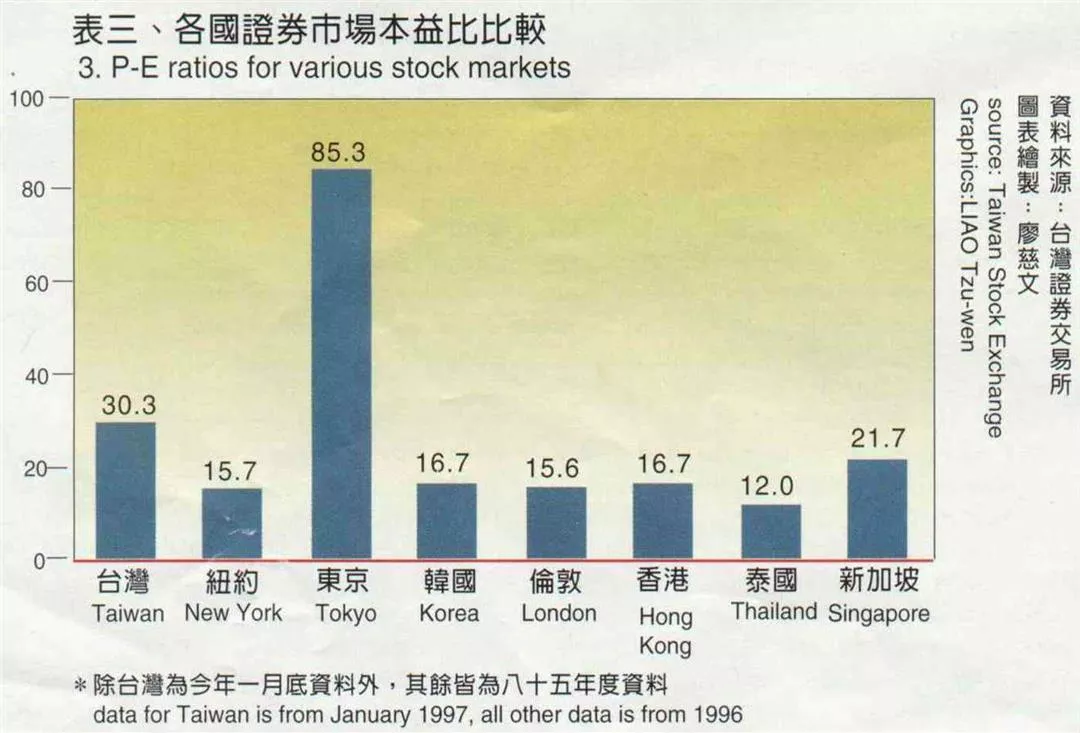

In the past, once a tipped stock started up, investors plunged in, sending it skyrocketing. With more stocks, and money more spread out, this no longer happens. Faunus Kuan points out that right now most stocks have lower values than the last time that the market was at the 8000 level. In terms of the P-E ratio (price to earnings ratio, which measures the year's stock value against the annual dividend), during the 1989 fever it was 56:1. That means that for every 56 dollars invested, you earned one dollar in dividends. Clearly people then were not chasing dividends, but the amounts to be earned in speculative trading.

Today, the average P-E ratio has fallen to about 30:1, though this is still high compared to the average abroad of less than 20:1. (see chart)

"The Taiwan stock market is growing too slowly, and can't keep up with domestic demand to invest," says Yin Nai-ping. There are more than 750 firms listed on the Korean stock market, and more than 580 in Hong Kong. Even in Singapore and Thailand, with smaller economies than Taiwan, there are more than 400 firms in each market. Thus one of the most pressing tasks in Taiwan is to encourage healthy firms to list in order to quickly expand the market. (see the article "Beefing Up the Bourse")

At the same time as there is a strong effort to expand the bourse, the structure of investors is gradually shifting.

Scattered investors

For many years now, the dominance of scattered small investors has been a big headache for the Taiwan stock market. Whenever the market soars, there is a "mass movement"-everybody from housewives to old veterans to illiterate grannies zoom in like a swarm of bees. One fund manager describes them as "an army of ants, completely without discipline." Currently more than six million accounts have been opened; about one adult in every four in Taiwan has an account (an individual may open more than one), the highest ratio in the world.

Generally speaking, individual investors lack expertise, nor do they have deep financial resources. Thus they lack confidence and staying power, are easy prey for rumors, and blindly "chase the market up and slash and burn it as it falls." They are easy targets for speculators; the bourse's reputation as a "cannibal market" was built on the pile of bodies of fallen individual investors. In the recent scare over the pork crisis, most of those selling willy-nilly at cut-rate prices were individual investors.

To change this image, the government has been actively opening the way for establishment of group financial services. There are now more than 100 funds. Although it is still difficult to change the common attitude that "it's my money, why should I give it to someone else to invest?," the ratio of total investment made by institutionalized financial services has been rising. In the last cycle it was only 4%; it has now risen to 10%. However, this is still far less than the 50% in the US and the 75% in Japan.

Unlike the individual investors, stresses Thomas Yeh, "the larger companies have financial resources, information, and the ability to make expert judgments, and they are versed in the adjustment mechanism for market stabilization of 'buy low, sell high.'"

Further, increasing weight for big investment institutions can also promote a more rational investing attitude. "In the past, people avoided big corporate stocks and blue-chips because these were least vulnerable to speculation and manipulation," notes Yin Nai-ping. However, in the middle of last year "Morgan perspective stocks" were popular; these were all stocks from big corporations or high-tech firms with strong potential. In the past speculators focused on small companies and "asset stocks" (firms with a lot of property); the fact that these cannot make it on to the global stock stage is a good lesson for local investors.

Of course, there is intense competition among the investment firms. To keep up sales and attract investors, there is insider trading and cut-throat buying and selling, things market experts frown upon. However, generally speaking, "when the investor service groups choose a stock they dare not depart too much from the fundamentals. Otherwise, if they lose money speculating, how will they explain that to their investors?" explains Faunus Kuan.

Will there be another bust?

Facing these risks, naturally some investors understand that they should play it safe. "When the P-E ratio gets too high, it would be better to cash out than to try to squeeze every last dime out." Thus does CPA Peng Yun-kun caution her friends. She concludes: "If people were not made blind by their greed, and everyone got off the train early, there would be much less chance that it would become a runaway train and crash. That would be better for everyone."

The Taiwan stock market has certainly changed in both physical and psychological aspects. But is it changing fast enough? Can the market cope with a new wave of incoming cash without crashing? No one can say for sure. Regrettably, over the past year or so, uncertainties in domestic and international politics have caused confusion in the economic and financial situations. It was unexpected that after the sharp fall in money flow there would be a sharp increase, and at such a rapid pace to boot. It looks like the hopes for a healthy stock market are in a race against time, and are falling behind.

Tseng Chu-wei, chairman of the Department of Public Finance at National Chengchih University, says: "Today the Taiwan stock market has a bigger stomach, and can digest a lot more. But even so, if it tries to swallow a huge portion all at once, it will still feel bad and throw it all up again!"

"Once the trading volume becomes huge, then the number of people taking the opportunity to speculate will also be large," says one manager at a securities company. There is an expression used in the market: "In a fall, emphasize quality stocks; in an upswing, go with the trend and buy anything." Looking at the new upswing, if in choosing stocks at this time one were to be mired in P-E ratios, company profitability, and so on, then "you would be working against your own money!"

Speculation replaces investment

As the index soars, and expert judgment seems increasingly inapplicable, old hands in the market are getting wary that the time of transition, when "investment pulls out, while speculation moves in," is sneaking up. The atmosphere of speculation at brokerage houses is beginning to overwhelm rational money management.

With the situation heating up, everywhere in the streets and marketplaces one hears conversations about speculative buying. There are again special kiosks of bourse books in the bookstores. It has even happened that a government agency had to ask higher-ups whether or not it was permissible for staff to take "personal time off" to play the market. One factory manager says that the search for labor went into a deep freeze right around the Chinese New Year. He is very worried: Will the work ethic again be sacrificed to money games?

With the situation having gotten his far, Tseng Chu-wei raises a warning signal: "Once speculation gets rolling, the stock market loses its function as a window on the economy. The government should take this opportunity to act."

Tseng argues that, after the harsh lessons of the last boom-and-bust cycle, people should have faith in the Central Bank's expertise and experience. What's frustrating is that the stock market is very politically sensitive. The biggest worry is whether or not the Central Bank has the "policy courage" to do anything.

Heading for a fall?

Tseng points out that at the beginning of March, Central Bank vice-governor Hsu Chia-tung merely said one simple sentence-"Investors should keep risks in mind when the market is on the high side"-and he was immediately assailed from all sides. He was even called up before the Legislative Yuan for a tongue lashing. In the United States, in contrast, Alan Greenspan, chairman of the Federal Reserve Board (comparable to the Central Bank in Taiwan), has on several occasions said things designed to cool off the market, and the market has obediently fallen each time. Though investors are naturally dissatisfied, they are not able to challenge his authority. This distinction can have a crucial impact at key moments.

Currently the Central Bank is forced to adopt a low-profile policy of "do but not say." It is quietly issuing more public debt to soak up floating capital. But it does not publicize warnings to investors, and has even denied that there is any policy to rein in on money supply, so as not to cause a panic. For the time being, however, the hog disease scare has solved the problem for the Central Bank of how to slow the market.

Looking at the past, the last wave of stock fever-with its tidal wave cresting past the 10,000 mark, then falling with devastating force-ended up in a massive redistribution of wealth in Taiwan. When the market is unhealthy, it can be manipulated, and naturally the rich ended up richer and the poor, poorer. Moreover, the huge financial losses of the last cycle disrupted countless families and bankrupted many businesses. Finally, the last cycle had the side-effect of contributing to property speculation, leaving many people who were not quick enough to get in at the beginning unable to afford homes. The accumulated grievances and wounds of that period have yet to heal.

"He built a great building, the building collapsed." Will this summary of the fate of stock players six years ago be replayed? It's too early to say. But as the money tide again builds up steam, and the dream of overnight wealth again begins to bubble in people's minds, perhaps investors should take a moment and think: If we don't abandon our greed, and change our habits, when the bubble bursts again, what will Taiwan be like then?

P.31

After years in the doldrums, the Taiwan stock market was again over 8000. As investors looked forward to higher returns, who expected an outbreak of foot-and-mouth disease would send stocks tumbling? How should investors see the market?

P.32

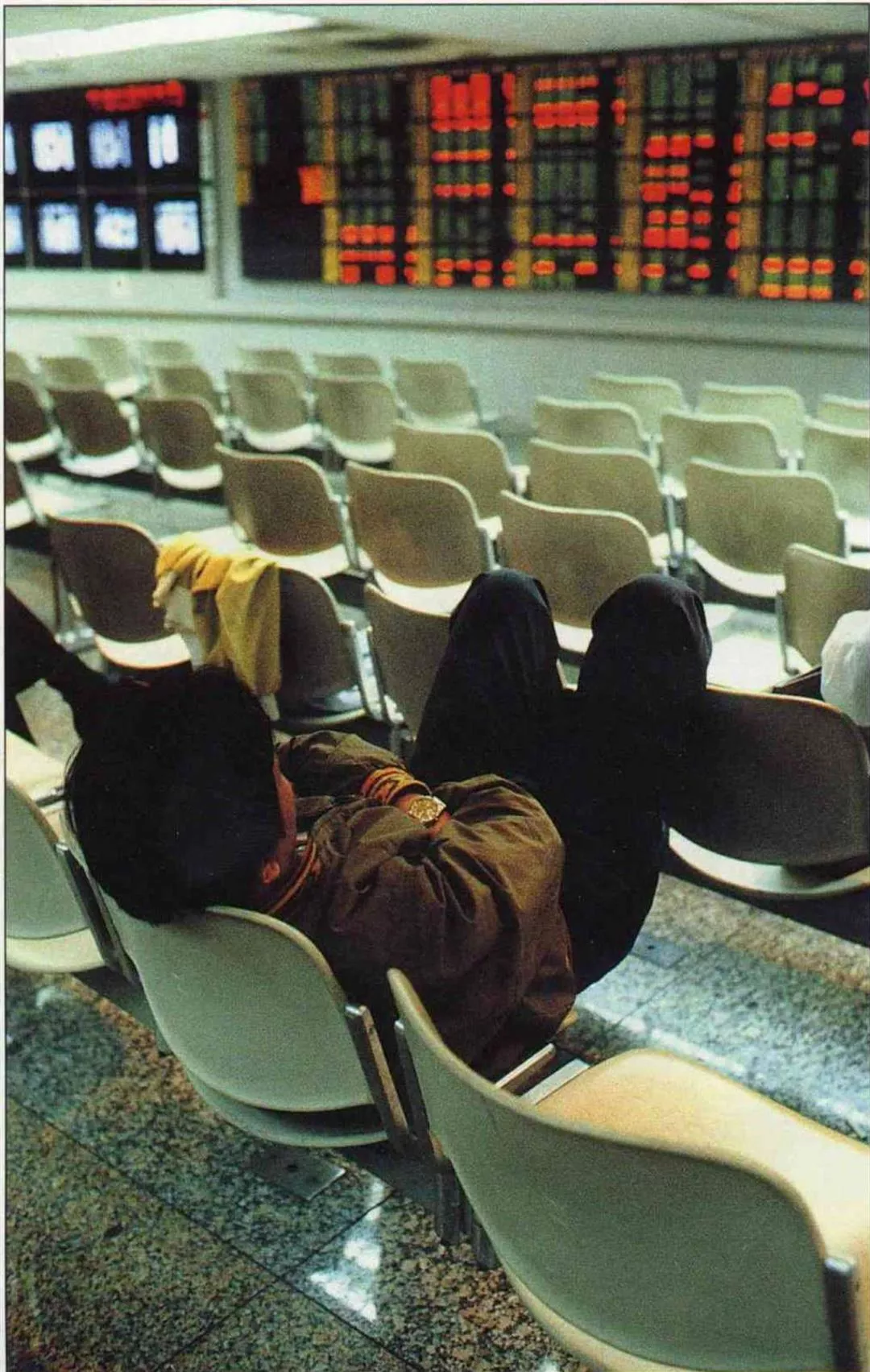

In 1990, the market crashed, investors scattered, securities firms went belly-up, and brokerages were deserted. (photo by Huang Li-li)

P.33

Stocks and property are two major targets of local investors. During the last stock boom, property prices followed suit, and builders overbuilt. When stocks fell, so did property demand; many apartments stand empty. (photo by Vincent Chang)

P.34

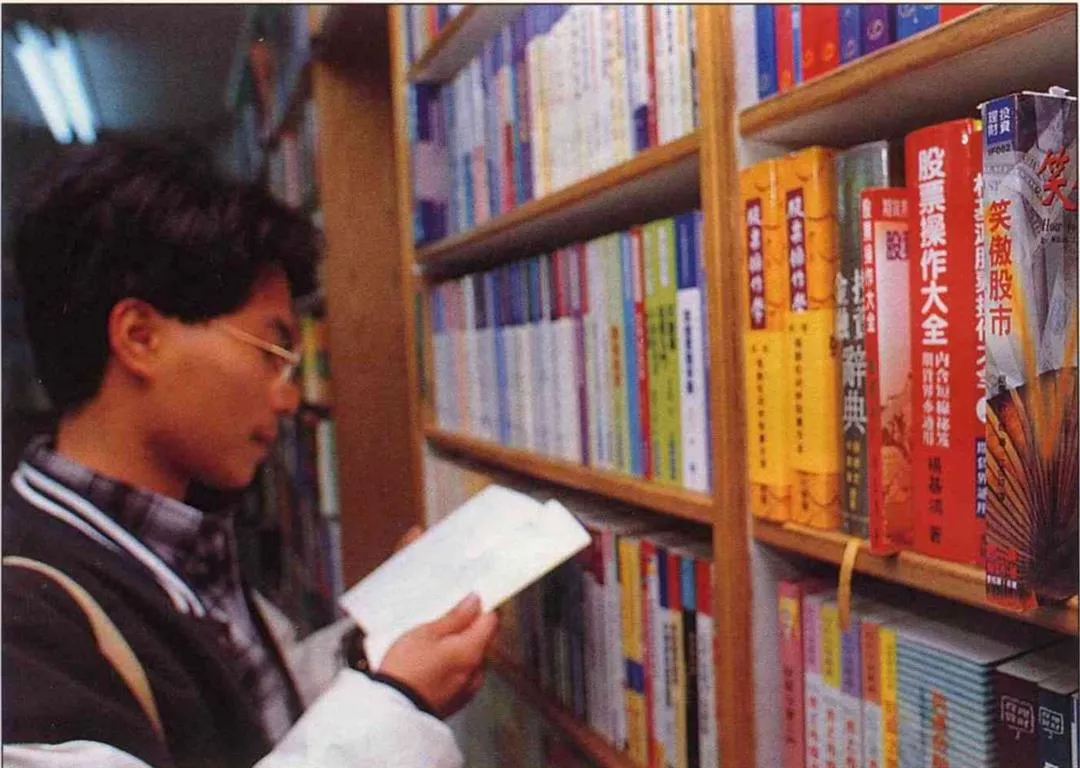

With the bourse booming, bookstores are getting on the bandwagon with specialized shelves of stock-related books. This gives some insight into a special feature of Taiwan's market-the large number of independent, individual investors.

P.35

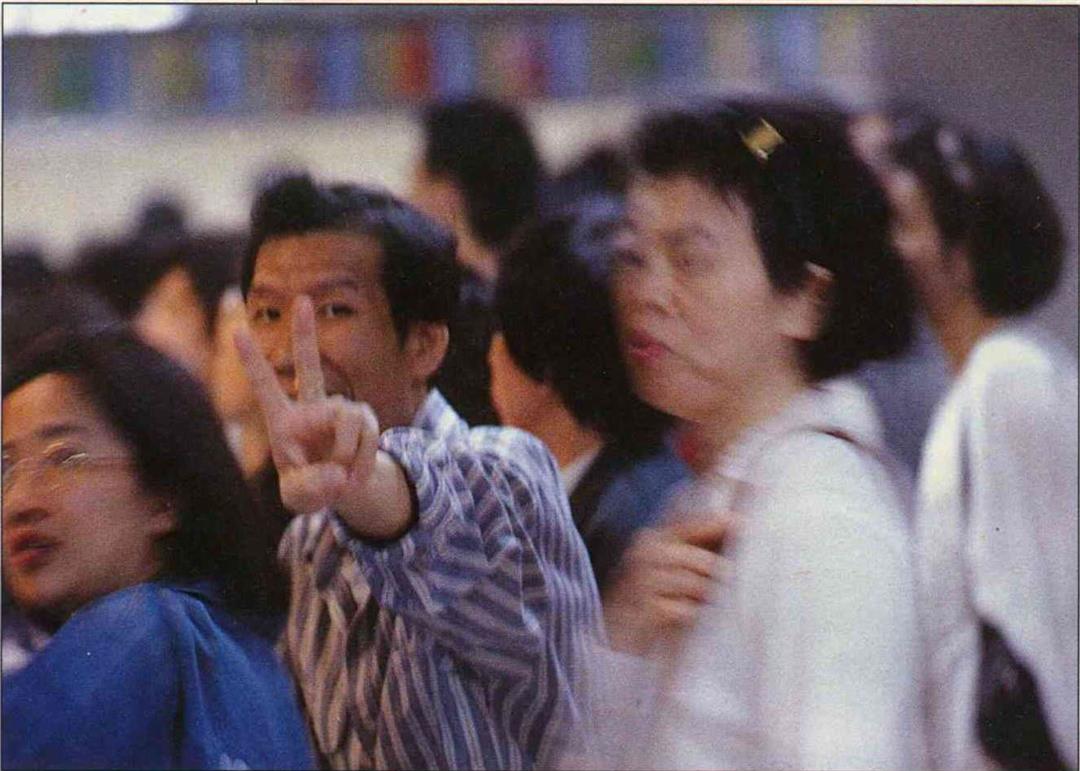

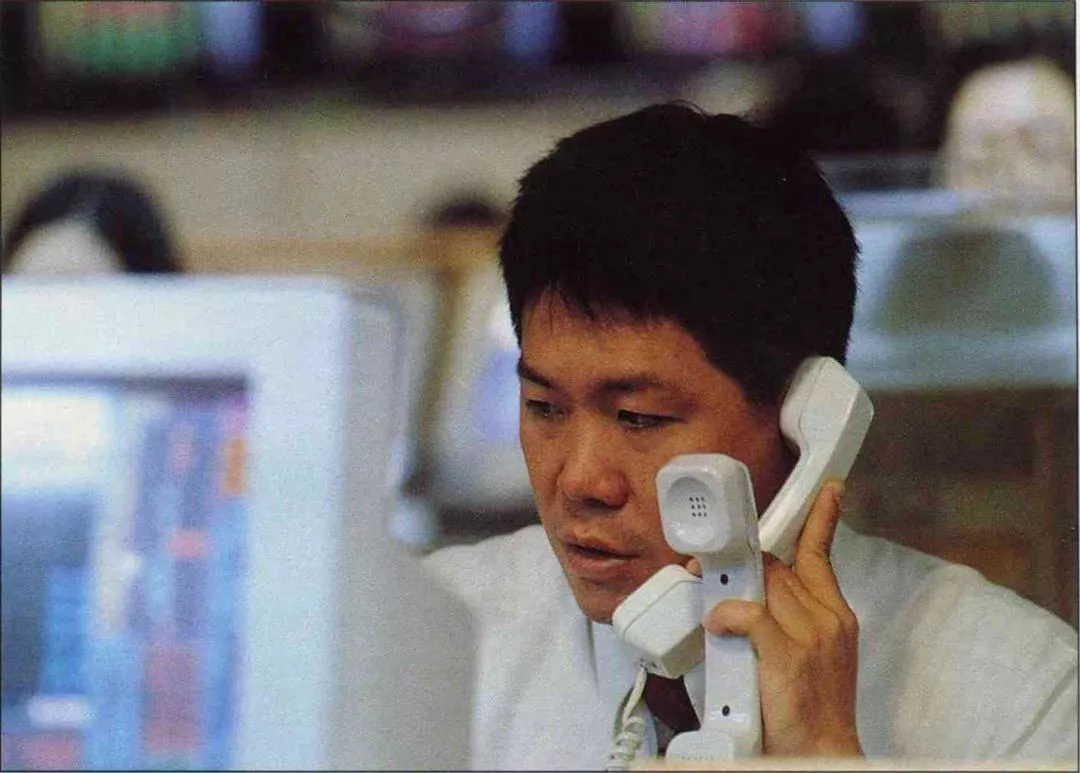

Recently new records have been set for trading volume every day, reaching NT$200 billion. Once again employees at brokerages have their hands full taking orders, while the national treasury is picking up a neat sum in transaction taxes.

P.36

Tension between Taiwan and mainland China is the biggest worry for the local stock market. (photo by Huang Li-feng)

P.39

In the last third of March, when foot-and-mouth disease hit local hogs, causing an estimated loss of NT$200 billion to related industries, the market fell into a trough. The photo shows quarantine personnel burying slaughtered hogs. (photo by Tsai Sen-tien)

Stocks and property are two major targets of local investors. During the last stock boom, property prices followed suit, and builders overbuilt. When stocks fell, so did property demand; many apartments stand empty. (photo by Vincent Chang)

With the bourse booming, bookstores are getting on the bandwagon with sp ecialized shelves of stock-related books. This gives some insight into a special feature o f Taiwan's market--the large number of independent, individual investors.

Recently new records have been set for trading volume every day, reachin g NT$200 billion. Once again employees at brokerages have their hands full taking orders, while the national treasury is picking up a neat sum in transaction taxes.

Tension between Taiwan and mainland China is the biggest worry for the local stock market. (photo by Huang Li-feng)

In the last third of March, when foot- and-mouth disease hit local hogs, causing an estimated loss of NT$200 billion to related industries, the market fell into a trough. The photo shows quarantine personnel burying slaughtered hogs. (photo by Tsai Sen tien)