Last year (1995), the high-profit industry which people worldwide looked upon with most envy was without a doubt the semiconductor industry, in which one could recoup one's investment in only a year. But in 1996, the industry which has suffered the biggest setbacks, giving a slap in the face to investment analysts everywhere, has also been the semiconductor industry.

Taiwan's semiconductor industry first grew up around the Electronics Research and Service Organization (ERSO), one of the organizations under the umbrella of the Industrial Technology Research Institute (ITRI). At every stage in its history, from the early days when it was laughed at as an "I try" (I-TRI) industry, to the dazzling profits it earned when it seized its opportunity to take off, to today when people are saying: "Semiconductors? Half the companies are sure to fail!" (a pun on the word "semiconductor" in Chinese), the industry has without exception proven the rule that high-tech industries are also "high-risk, high-profit." After its "miracle," how is Taiwan's semiconductor industry faring in less favorable times?

Lumps of hard black stuff with metal legs, containing many tiny crystals. For a number of years now, these unlikely looking little objects-integrated circuits (ICs), the most typical of semiconductor products-have surpassed petroleum and gold to rank firmly in first place by total value among products imported into Taiwan.

But one day the tables may be turned, for these little items may in future become a major export product for Taiwan. Compared with other sectors which have been singled out for promotion as key industries but which have not so far got off the ground, such as aerospace, optoelectronics and biotechnology, semiconductors-and ICs in particular-have seen a meteoric rise, making the semiconductor industry Taiwan's most dazzling new industrial sector.

4, 5, 6, 8. . . . as the silicon wafers grow larger to accommodate more chips, production becomes more economic. The explosion in the number of eight-inch wafer plants worldwide is the main reason for the collapse in semiconductor prices in 1996.

1995-the key year for ICs in Taiwan

Twenty years ago the idea of manufacturing ICs in Taiwan was no more than a far-off dream. Sixteen years ago, Taiwan's first IC-a chip to control the display of digital watches-was successfully manufactured. However, simple watch display chips cannot meet the needs of Taiwan's information industry companies, and Taiwan spends enormous amounts of foreign exchange on dynamic random access memory (DRAM), static random access memory (SRAM), central processing units (CPUs) and all kinds of other integrated circuits, which are assembled into computers and motherboards for export. When shortages in international markets make ICs hard to find, Taiwan's IT companies have no choice but to run all around the world in search of them.

With the help of such powerful demand, Taiwan's semiconductor industry has gradually grown. Sixteen years ago, United Microelectronics Corporation (UMC), a company set up by the ERSO, was Taiwan's first attempt to break into the semiconductor industry. Nine years ago the Taiwan Semiconductor Manufacturing Company (TSMC), which was set up in the same way, built the world's first specialist "wafer foundry" (an IC fabrication plant producing entirely to clients' orders without doing its own design work or having its own brands), which vastly raised productivity and profitability over existing plants. From then on the number of semiconductor makers in Taiwan gradually grew, and each of them is now quickly growing in capability and size.

Last year was a crucial year, in which the ROC's semiconductor industry took off on the springboard of its accumulated experience. Taking advantage of the worldwide surge in demand for semiconductors and particularly ICs, ROC manufacturers' net profits reached the high average of 47% of turnover. Hoping to follow up on this success, under the watchful gaze of large multinational companies many ROC manufacturers, undaunted by their relative youth and inexperience, embarked on the same rush to build eight-inch silicon wafer plants which was sweeping the world.

For example, in the Hsinchu Science-Based Industrial Park, where the largest number of Taiwan's semiconductor makers are concentrated, before 1995 there were only four eight-inch wafer plants, but in 1997 this figure will rise to 19. Added to the existing four-, five- and six-inch wafer plants, they will make the park one of the world's major centers of semiconductor production. Today, Taiwan's production capacity is equal to some 3% of global supply, making it the world's fourth largest supplier.

Of course, semiconductors were first developed in the USA, and after 30 years of the industry's existence, whether in terms of design capability or process technology the US's dominant position is unassailable. The heart of a computer, the CPU, has long been the virtual monopoly, in the personal computer market, of the US company Intel. In terms of demand, the USA also accounts for one third of the global market, putting it in first place by a wide margin.

Close behind in supply terms is Japan, which has never made a secret of its ambition to take first place. Meanwhile South Korea ships 10% of the world supply. Although Taiwan still trails far behind the USA, Japan and South Korea, judging by the high speed at which its production capacity is expanding, by the year 2000 the island could be in a position to supply 5% of the world market for semiconductors, and thus become one of the few key players.

Meanwhile the construction of one eight-inch wafer plant after another in Taiwan has brought business opportunities worth over NT$100 billion for semiconductor device manufacturing equipment, and worth tens of billions of NT dollars for silicon wafer material and downstream operations such as chip packaging and testing. Attracted by this prospect, the major US and Japanese equipment and materials manufacturers are trying their best to "squeeze" their way into the Hsinchu Science Park, in order to be close at hand to service their customers.

Wu Hung-jen, a senior vice-president at UMC, recalls that a few years ago, to buy a piece of machinery one would have to go all the way to the USA to try it out. Today, however, equipment suppliers are setting up shop on manufacturers' doorsteps, at their beck and call, and constantly show up unbidden to demonstrate new equipment. This contrast tells more plainly than words how the international status of Taiwan's semiconductor manufacturing industry has risen.

In September 1996 the US company Semi-Con held its information exhibit i n Taipei for the first time, symbolizing that Taiwan's semiconductor industry has arrived on the world stage.

Unlimited technological advance

The importance of semiconductors on the ROC's industrial map has also been growing by the day.

"Last year the turnover of the 12 companies in Taiwan's integrated circuit manufacturing industry totalled NT$120 billion, of which over 60% went to export. The IC industry as a whole accounted for 4% of Taiwan's total export earnings," says Tung Lian-shen, director of the Division of Investment Services at the Hsinchu Science-Based Industrial Park Administration. Pointing out the sites of new factories on a map of the park, he adds: "Taiwan's industrial future will depend on semiconductors."

Walking through the southeast corner of the park, where the semiconductor factories are concentrated, it is hard to imagine that these plants, built at a cost of at least NT$10 billion each, are hidden inside these sleek-exteriored office buildings. Although semiconductors are very expensive to produce, they do not consume much in the way of resources. TSMC's new plant even saves land by placing one production line above another in a multi-storey factory building.

Compared with the petrochemicals industry, "for the same value of production, the semiconductor industry only uses one-sixteenth as much water and electricity, and occupies only one-thirty-second as much land," says Hwang Chin-yeong, director of the Institute for Information Industry's Market Intelligence Center. "In Taiwan, which lacks natural resources, what industries should we give priority to helping develop? The answer is very clear."

To build on its success, Taiwan's semiconductor industry needs not only to increase its "quantity," it is also pressing hard in pursuit of technological advance. Do you still remember the "prehistoric" age of the information industry 20 years or so ago? In those days, personal computers had not yet hit the market, and for data to be read into the outsized computers of the day they had to be fed with stacks of punched cards. Back then, UMC began manufacturing using 7.6 micron process technology (the micron figure or "process dimension" expresses the smallest achievable gap between lines of metal on a chip).

Since then, with the headlong advance of IC manufacturing technology, "die shrinking" and "high density" have become the endlessly pursued goals, and technology has progressed rapidly from five microns, to three, to one, and to today's new global standard of 0.25 microns.

As the process dimension is reduced, the same area of chip can hold a larger number of circuits, and memory capacity increases as a result. The capacity of one DRAM memory chip has also risen from one megabit (Mb) to 4Mb, then 16Mb, and today some overseas plants are already mass-producing 64Mb chips (see "A Submicron Journey"). "They say IC technology doubles in capacity and halves in price every 18 months," says Hwang Chin-yeong, who observes that with such rapid change, it is a remarkable achievement for Taiwan to have caught up from being many generations behind the rest of the world to reach its current position. To take DRAM as an example, UMC has developed its own 0.35 micron technology and is mass-producing 16Mb DRAM chips, which one can say are only "three-quarters of a generation" behind the next goal (producing 64Mb DRAM chips at a process dimension of 0.25 microns).

Memory chips, microprocessors, logic components, analog devices. . . . ICs of every description, hidden away in such products as computers, audio systems and cell phones have brought much comfort and convenience into people's lives.

The dangers of being at the forefront

However, at the crucial moment when Taiwan was thrusting ahead with great expectations towards seemingly unlimited opportunities, the wind of the international market suddenly turned about, and prices collapsed. IC manufacturers around the world, who were still basking in the enormous profits they had been earning, were caught napping.

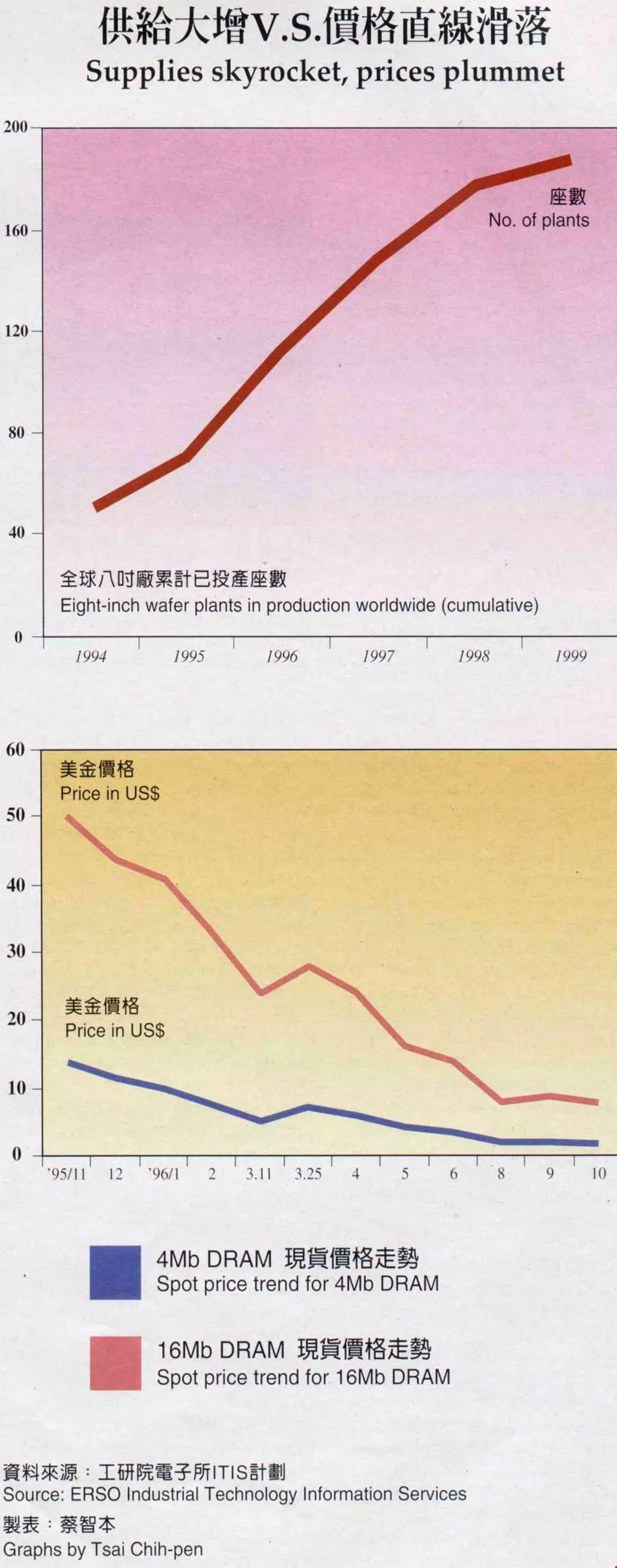

The change began in the fourth quarter of last year, and today, a year later, prices have still not recovered. 4Mb DRAM chips, which are used in huge numbers in computers, are a good example. In the heady days of the middle of last year they were in short supply and would be snapped up immediately even at the price of US$15 each. But they have fallen to a unit price today of US$1.80, only one-tenth of their former price and barely more than their manufacturing cost-not including the depreciation on the multi-billion-dollar factory and equipment.

Last year, in its first year of business, the Vanguard International Semiconductor Corporation earned operating revenue of NT$5 billion, and was seen as the "star performer" of the industry. This year it expanded its production capacity by 100%, but only saw its turnover grow by around 40%. Vanguard President Tseng Fan-cheng, when talking about this year's difficult operating conditions, cannot help blurting out: "I think prices must have bottomed out-they can't fall any further. If they do, everyone will just have to grit their teeth and shut up shop!" Tseng, formerly a senior vice president at TSMC, took over the running of Vanguard only in June this year. A doyen of the ROC's semiconductor industry, he is a veteran of many campaigns, but his jocular tone today cannot hide a hint of pessimism.

Vanguard is no special case. All the companies in the Hsinchu Science Park are beset with worries. UMC, which saw negative growth in its turnover this year, still expects to turn a profit of NT$8 billion-but this will be down by almost half on last year's more than NT$13 billion. TSMC, which has always performed outstandingly, still paid out bonuses of an extra month's salary in the first and second quarters of this year as usual. But in the third quarter, as the operating climate became more difficult, employees received a much reduced bonus.

Why is the semiconductor market in depression? Will this bring down Taiwan's most dazzling new industrial sector at the first hurdle? In fact, no. "This is a price upset affecting the semiconductor market worldwide, but actually Taiwan has got off rather lightly," say Hwang Chin-yeong of the Institute for Information Industry.

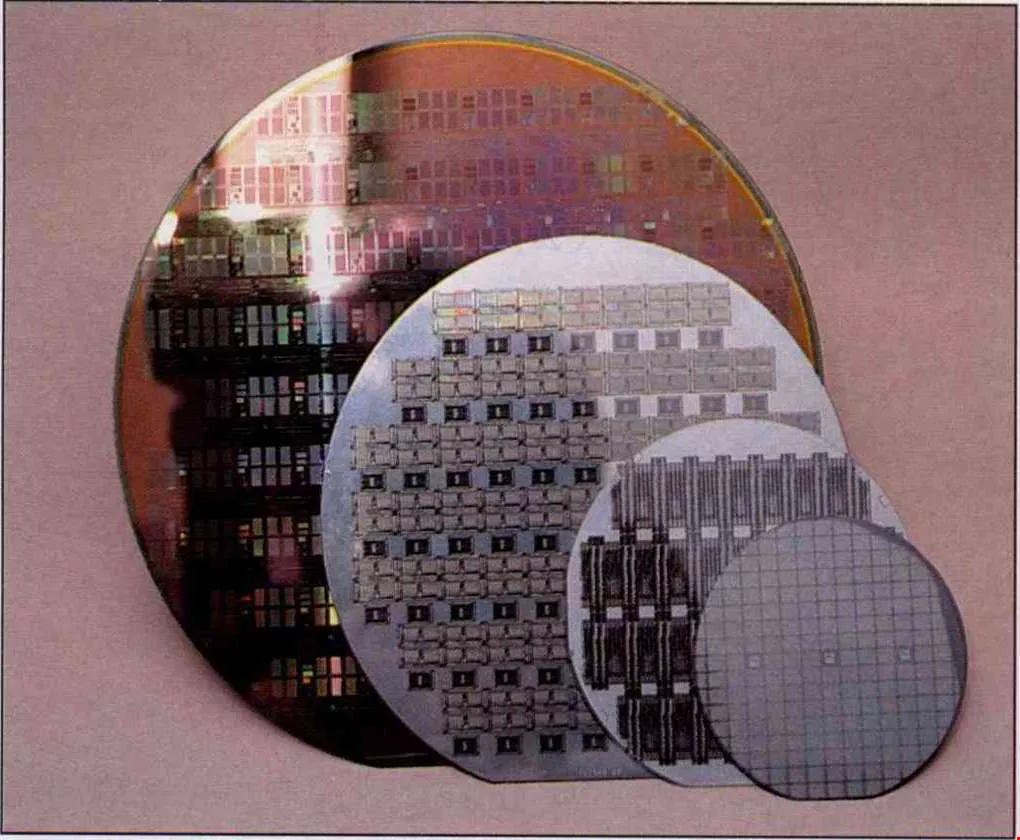

Serried rows of chip dies lined up on silicon wafers; after the circuits are tested the wafers will be sawn up and the dies packaged to make many black, rectangular integrated circuit chips. The wafer on the left in our picture carries 4Mb DRAM chip dies, while the one on the right carries 16Mb DRAM dies. (photo by Diago Chiu)

"Little" Taiwanese firms suffer the least

The main reason for the downturn is an excess of supply over demand. With the global rush to build eight-inch wafer plants, the number of plants worldwide grew from only 46 in 1994 to 73 in 1995, and has leapt again to 170 in 1996. The almost dinner-plate-sized eight-inch wafers carry twice as many chips as the previous six-inch wafers, and four times as many as the old four-inch wafers.

With this surge in production capacity, the former "scarcity value" of silicon chips has disappeared, but at the same time sales in the integrated circuits' main market-personal computers-were not as brisk this year as had been expected, and PC market growth fell back to 15% from last year's 25%. This hit semiconductor sales hard. With supply outstripping demand, in order to try to claw back their multi-billion-dollar investments as fast as possible, all the manufacturers gritted their teeth and began cutting prices to promote sales, just to keep their plants running at full capacity.

In other words, the status of integrated circuits went from being key components with technology concentrated in the hands of a few large manufacturers worldwide, to being freely available products which have entered the mature stage of their life cycle, with "low profits, cheap prices and high volume." Taiwan made no small contribution to this change.

"In any high-tech industry worldwide, if only Taiwan succeeds in capturing a small corner of the market, prices immediately become 'reasonable'!" says Hwang Chin-yeong with a laugh, quoting PCs and notebook computers as examples of this "pernicious" effect. Being aware of the "locust-like, dog-eat-dog" tendencies of Taiwanese businesses, some foreign companies, especially Japanese, were naturally alarmed to see the rapid speed of Taiwan's expansion in semiconductors, and continually warned Taiwan against overinvesting.

"Semiconductors shouldn't be a private game for European, US and Japanese companies. Why shouldn't Taiwan come in and 'play'?" retorts Hwang Chin-yeong. All the more so since foreign reports estimate the operating efficiency of Taiwanese wafer plants as being 20% better than those in Japan and 10% better than South Korea's. If Taiwan really has "overinvested," the companies which may be unable to stand the heat and have to close down may well be the foreign companies with top-heavy organizations, inflexible decision-making structures and less effective cost control than Taiwanese firms.

In fact in 1995, as global capacity rocketed and the prospect of market oversatura-tion loomed, worried market observers warned of an "IC 1997" crash. But to everyone's surprise, the storm arrived even before 1995 was over, and the first spark of price cutting which ignited the explosion came from none other than giant CPU maker Intel.

Originally Intel had planned to produce motherboards itself, so in 1995 it bought in large stocks of ICs in preparation. But later the company decided not to produce motherboards, and began offloading its enormous stocks. For a time rumors were rife, other companies began dumping stock, and the artificially induced crash became unstoppable.

However, "compared with the big foreign conglomerates, Taiwan's IC makers are smaller, less vulnerable and can respond more flexibly," says Genda Hu, who worked in the US semiconductor industry for nearly two decades before returning to Taiwan in July this year to take up his appointment as general director of the ERSO. The companies which have been hardest hit are probably South Korea's Samsung, Hyundai and Goldstar groups, whose main semiconductor products are memory chips, which account for 80% of their production value. Last year's crash affected memory chips worst, and South Korea has suffered badly. By comparison, Taiwan's semiconductor industry's products are more diverse and it does a higher proportion of contract work, which bears a lower risk. This gives Taiwan's companies greater scope to respond.

Doomed to failure?

When we examine the operating philosophy of the various companies, "keeping a tight rein on costs and reducing defect rates" seems to be the universal formula. Few companies have laid off personnel, but it goes without saying that all have frozen recruitment. Recently many suppliers of "grey-market" machine parts have appeared near the Science Park. Components which were on the verge of being scrapped, but which cost US$3000 or US$5000 new, are taken off machines, reworked and reground; this "belt-tightening" approach, making every penny count, is an effective way of saving money.

The biggest effect seems to have been that new investment plans have been temporarily shelved while companies adopt a wait-and-see attitude. For example, the second plant of TI-Acer, a joint venture between Acer Inc. and the US company Texas Instruments, is currently under construction and was originally due to come on stream early next year. The company hoped the plant would be the first in Taiwan to produce 64Mb DRAM chips. But due to a "very large decline in profitability," the purchase of machinery has been deferred for the time being, although the factory is still being built. "Once the machines are bought, you have a NT$10-20 billion investment sitting there, and this is a tremendous burden. But to install the machines takes only two to three months, so it will not be too late to put them in once the market turns up again," explains Ruth Pao, public relations manager in the president's office at TI-Acer.

On the eve of the crash, UMC, the veteran player in the ROC's semiconductor industry, was in the midst of a large-scale restructuring program. Coming during this painful period, the downturn naturally put the company under heavy pressure.

"In the past, UMC shouldered the mission of implementing the government's industrial policy, and to build up the local semiconductor industry we had to do both circuit design and chip fabrication. Today, with the trend towards specialization and division of labor, UMC naturally has to restructure," says the firm's president, John Hsuan.

Not to do so would be like "a printer trying to write his own books": on the one hand there is enormous scope for development and improvement in printing technology (the manufacture of IC wafers), but on the other, if one also has to concern oneself with the content of what is being printed (the circuit design of every chip), one is almost sure to overreach oneself.

In its restructuring, UMC is following the model of TSMC, to become a specialist IC fabricator which neither designs its own chips nor markets products under its own brands. In order to gain market share, UMC has not only built a third factory, which was finished just last year, but has also set up joint ventures with 11 foreign companies to simultaneously build three eight-inch wafer plants in the Hsinchu Science Park; the plants are to do contract work for these companies. With shareholdings of 25% in the three new joint-venture companies acquired with cash investments and another 15% for technical input, UMC will also have operating control of them.

"Contract work bears a lower risk and brings reasonable profits, and UMC will be able to concentrate on pursuing improvements in manufacturing technology." John Hsuan says it is a mistake to think that "contract work" implies a low status. In fact, in high-technology industries internationalization and a "vertical division of labor" are inevitable trends. Many major design houses have first-class circuit designers, but lack the billions of NT dollars needed for wafer plant investments. Sometimes they have no choice but to use other people's second-rate production facilities. But with UMC's first-class process technology available for contract, and with these 11 design houses as its joint venture partners and basic clientele, the company is not worried that it will be short of business.

DIY computer buffs upgrading their own machines at home rely on adding o r replacing various ICs.

Riding on the wings of "IT"

All the companies have responded to the crisis in their own different ways, but facing the year-long downturn in business, won't the Taiwan semiconductor industry, which has only just got on a firm footing, be hit by a round of failures? Will the punsters' prediction-that semiconductors equal bankruptcy for half the companies in the business-come true?

"For the moment it doesn't look that way," says Tung Lian-shen, director of the Hsinchu Science Park's Division of Investment Services. He assesses the situation thus: "Over the last two years, semiconductor companies earned 'outrageous' profits; this year in fact they have just 'returned to normal.' What's more, when they were earning money, the Taiwanese firms earned more than foreign firms, and this year they lost less than foreign firms." Tung Lian-shen even believes: "A little risk is actually no bad thing, for it can give industry players back their sense of crisis, and give them practice in crisis management. Otherwise if you're earning fat profits every year, where's the challenge? Do you just wait for retirement?"

Vanguard International President Tseng Fan-cheng regrets that his company had the bad luck to be set up too late, "so that the downturn hit us before we had earned enough." But looking around at his colleagues in the Science Park, he too says that while profits are not as good as before, he expects only a very small minority of companies to suffer actual losses. Compared with other industries struggling in the same economic climate, semiconductors are not faring too badly.

A temporary stormy period is no cause for panic, but can Taiwan's semiconductor industry maintain its competitive advantage in the long term? That is really the key question.

"The greatest advantage of Taiwan's semiconductor industry is the powerful information technology industry which stands behind it, observes Hwang Chin-yeong. Last year, production by the ROC's IT industry in its factories both inside and outside Taiwan accounted for a staggeringly large slice of the global market pie. Many of Taiwan's computer and peripheral products, such as motherboards, monitors, image scanners, mice, network cards and graphics accelerator cards, are firmly in the lead in terms of worldwide market share, far ahead of other countries. And semiconductors are the main components used in these IT products.

"In every computer worth US$1500, the most valuable parts, probably adding up to US$800, are all those integrated circuits in their tightly packed, neat rows," says Dieter Chen, a project manager at the Market Intelligence Center.

But Taiwan's semiconductor industry differs from those of Japan and South Korea, whose domestic production capacity exceeds domestic demand. Although Taiwan's IC production capacity expanded sharply last year to reach 2.7% of the global supply, it still remained far below the 6.5% of global supply consumed by Taiwan's market. Today Taiwan mainly makes semiconductors to order for export, and its current rate of self-sufficiency is only 18%. The amount of foreign exchange spent on importing semiconductors is as high as ever.

"High-tech industries are highly internationalized"-Hwang Chin-yeong explains the paradox of Taiwan exporting large quantities of ICs on the one hand, while also importing them in large quantities, thus: with the trend towards vertical division of labor, it is perfectly normal for Taiwan's manufacturers to ship their finished ICs to the USA, from where they are sold back to Taiwan's computer makers.

Many semiconductor companies don't even make a distinction in their sales figures between domestic sales and exports, but include the local Taiwan market under the Asia-Pacific market. "In any event, whether they are sold into Southeast Asia or mainland China, aren't they all sold to Taiwanese companies?!" says one industry executive.

On this point, UMC President John Hsuan says emphatically: "Taiwan's semiconductor industry and IT industry previously made nothing but 'me too' products, and were only able to compete on price in the international market, and follow the specifications of the big global players. But today, both industries have gained a degree of autonomy and amassed some marketing capability, so in the future an ever-closer interdependence is likely to emerge between Taiwan's IT firms and semiconductor makers." It is predicted that by the year 2000, Taiwan's degree of self-sufficiency in semiconductors could rise to 37%, so companies have a great deal of scope to press ahead.

High fidelity, high definition, more intelligent, cheaper . . . . the au dio-visual products on display mostly rely on semiconductors to satisfy consumers' desires.

Indians and Chinese

With Taiwan's own large IT industry, the island's semiconductor industry ought have no need to fear a lack of buyers; and today there is scope for improvement in aspects such as computer processor speeds, graphics processing, speech synthesis, graphic display, and even the amount of heat which IC's generate. The hopes for improvement are placed on higher-precision, smaller, higher-capacity ICs which transfer data faster and consume less power. The demand for a constant stream of new semiconductor products will naturally continue.

This is all the more true because the IT industry is far from being the only one to be asking wishes of this "high-tech genie," the microchip. Wu Hung-jen of UMC points out that in the consumer electronics, telecommunications, automobile and transport industries and in the automation of all kinds of industrial equipment, "wherever computers are used or there is a wish to make products more 'intelligent,' there is a place for semiconductors."

Wu observes that the range of applications is becoming ever broader, and the quantities of ICs used in each of them are also rising rapidly. Semiconductors' unlimited potential has hardly begun to be exploited, so how could the industry "fail"?

In terms of technical development, Taiwan's semiconductor industry also has an advantage.

"In the USA, ICs have a nickname: 'Indian-Chinese.' If you look around Silicon Valley in California, engineers of Chinese extraction are an influential group," observes ERSO general director Genda Hu. Over the last few years there has been a constant stream of highly educated people "deserting with their weapons"-experience and skills-and returning to Taiwan, and this has provided the greatest impetus to Taiwan's semiconductor industry. It is also one of the reasons why large US and Japanese companies take the attitude that "secrets can't be kept anyway" and come to Taiwan in search of partners to work with.

However, Genda Hu points up one worry: the semiconductor industry in Taiwan is after all still very young, and it is hampered by a severe shortage of skilled personnel, especially experienced personnel. "The engineers at overseas IC fabrication plants have at least seven or eight years' experience, but in Taiwan they have less than five years' experience on average. Those two years make a big difference," says Genda Hu.

The ERSO, which single-handedly created the ROC's semiconductor industry 16 years ago, has been the ROC's biggest source of qualified staff in the field, and it successfully set up three of the industry's companies: UMC, TSMC and Vanguard. But most private-sector companies do not have such a solid research team, and if they wish to join the fray, they have no choice but to directly form joint ventures with foreign companies, or buy technology from abroad. The earliest joint venture was TI-Acer, followed by Winbond Electronic Corporation (with Toshiba of Japan), Powerchip Semiconductor Corporation (with Mitsubishi of Japan) and ProMOS Technologies Inc. (Mosel Vitelic of Taiwan with Siemens of Germany), for which the contract was signed only in November. All of them follow the same model.

Tseng Fan-cheng, formerly a senior vice president at the Taiwan Semiconductor Manufacturing Company and now president of Vanguard International Semiconductor Corporation, is a doyen of the ROC's semiconductor industry. (photo by Diago Chiu)

A great leap forward

Although forming joint ventures with large companies from around the world is a shortcut which has the disadvantage that technical autonomy is relinquished to others, it really is enabling the process technology of Taiwan's semiconductor industry to be rapidly upgraded. However, Dieter Chen reminds industry members that in fact Taiwan's previous technical level was not bad-it's just that the industry "grew up on relatively low-profit products which advanced countries didn't want to make," such as ICs for musical greetings cards, video games or pocket calculators, none of which where very challenging. Now that companies are upgrading and planning to tackle the DRAM market, their abilities will be tested to the full.

John Hsuan, president of UMC, which, like other companies around the world is working to master the latest 0.18 micron technology, observes that previously, when Taiwan followed in others' footsteps, "the risks were small, and profits were small too." Now that companies are attempting to catch up and overtake the competition, the risks are much greater.

"If you want to earn easy money, you really don't have to go to all the trouble of trying to lead the field." But it is that streak of enthusiasm in scientists and engineers to "pursue subjective perfection and develop their ideals to the utmost" which makes John Hsuan grit his teeth and soldier on.

Tiny semiconductors have set off a storm of technological development of a kind rarely seen in human history. Taiwan has had the good fortune to jump on this high-profit bandwagon and has been able to snatch a substantial lead over countries like Malaysia and mainland China, which have just started in this industry. However, faced with large, powerful competitors and unpredictable, risky markets, Taiwan must still walk cautiously on the road towards realizing semiconductors' unlimited potential.

In November 1996, Mosel Vitelic Inc. of Taiwan signed an agreement with Siemens of Germany to set up a new company which is due to start fabricating 64Mb D RAM chips early in 1997. Taiwan Provincial Governor James Soong (second from left) and Minister of Economic Affairs Wang Chih-kang (far left) were both invited to attend.

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)