Money for Nothin'... But It's Not Risk Free

Laura Li / photos Hsueh Chi-kuang / tr. by Phil Newell

July 2000

It is said that the two hottest subjects in post-martial law Taiwan have been sex and personal money management, which certainly goes to show the degree of openness and pluralism in today's society. Moreover, like sex, personal money management is something that many people only vaguely understand, that they feel uncertain about committing themselves to, and that leaves them feeling tired and empty.

Personal money management is now a national sport. The wealthy hope to roll their money over, while those less well off are trying to make a small pile of their own. But what kind of money management approach is best suited to the current era? How can one win in the investment game without losing the game of life in the process?

"Earning money is the first priority, spending money is a sin, long live personal money management!" Thus declares a poster on the wall of a certain "Miss Chen," a secretary in a trucking company in Pingtung. Every night before going to sleep she turns on her computer to check out the closing share prices for the Taiwan Stock Exchange and the opening figures for the US exchanges, and then makes a quick calculation in her head of her total wealth.

This woman, who is nearing 30 and has been working for seven years, has a "personal value" which is still less than NT$600,000, so in order to build up a fund for investing, she will not buy a house or go abroad for travel, and she's becoming a Scrooge in the eyes of her friends. Yet, all her discipline and her enthusiasm cannot guarantee that she makes money. And sometimes when she looks at the poster on her wall, she feels as if she is being mocked.

If I knew then what I know now...

Liu Li-chih, a 25-year-old teacher, is another e-generation personal money management enthusiast. Even before he did his compulsory military service, he began making investments of NT$3,000 per month in a Japan technology fund. Over three years, the fund has gone from taking losses to taking off; though it has levelled off somewhat lately, the returns have been excellent.

Liu declares himself to be "a faithful believer" in all manner of personal money management books, and when he has free time in summer vacation, he spends an average of 20 hours a week looking at investment information. His greatest regret is that he began his financial career too late. He says: "If I had used my allowance every year from the time I was small to invest in a fund, at the rate of NT$30,000 per year, after 20 years, there would be quite a lot of money right now." Becoming increasingly agitated, he adds that if he had understood money management early on, he could have invested right after the big stock market collapse in 1990, and he would be rich today instead of regretful.

It looks like more and more of the e-generation are getting into investing. But do they know what they are doing? Dennis Chien of the money management website called JP Investment Clinic strikes a cautionary note: "I don't think the education system has fulfilled its responsibility to teach people how to manage their money."

Chien points out that school textbooks only teach moral lessons like "a penny saved is a penny earned," which are not exactly what the real world demands these days. In contrast, many American children understand a bit about money management from early on. For example, a child in her early teens might babysit for the neighbors or cut lawns, and then put the money in a mutual fund. Some investment websites have games for children to teach them about various investment instruments and portfolios. These treat personal money management as a serious life skill that all modern people should know.

Chien says that the situation is just like sex education in the past. They give it only the most cursory treatment in schools, but most people have a strong desire to find out about it, so as a result they have to pick up what they can from the newspapers or cable TV. The result of the lack of a proper investment outlook is that speculation is rampant.

According to statistics of the Ministry of Finance, 87.5% of the trading volume on the Taiwan stock exchange comes from individual investors. In 1999 turnover was 288% (that is, total trading volume was 2.88 times the total value of the market), which, though considerably down from nearly 600% ten years before, remained four times higher than the New York stock exchange. Despite numerous painful lessons in the past, the habit of chasing a rising market and cutthroat selling in a falling market has proven difficult to change.

A new climate for the e-generation

Fortunately, over the last three years foreign investors have brought some new ideas into the country. Although they still engage in "hit-and-run" high-volume trading for quick gains, at least most foreign investors ignore gossip and don't touch the more speculative stocks. Rather, they put more emphasis on the fundamentals of a given company or industry. Dennis Chien notes that foreign firms have also introduced risk management ideas like "having a well-rounded portfolio" (i.e. "don't put all your eggs in one basket"). These have had a positive impact on the local stock market, and have given the investment activities of the e-generation a more rational foundation than those of their parents.

The chief characteristics of the current wave of e-generation personal money management are great ambition, reliance on expert analysis, and diversification of investment targets. Nevertheless, the hottest investments are always changing, and perhaps no amount of rational analysis or detailed information will be able to change this.

Chia Chen-i, senior executive vice president of the Individual Banking Sector at Bank Sinopac (which earlier this year created a stir in the industry by introducing the world's first five-in-one money management account) has been observing the evolution of the financial environment in Taiwan for many years, and offers the following thoughts about trends in money management.

Chia recalls that in the 1960s, people were too poor to have any money to manage; there were also fears of war, and so any money people did have they quickly exchanged for gold or US dollars on the black market. In the 1970s, faced with two oil crises and inflation, the idea of buying property to preserve value became widespread, and those who could afford it bought land and houses. At that time, the stock market had only a hundred or so listed companies, and its fate depended on a few manipulators behind the scenes. It was seen as a "cannibalistic market" which scared off most citizens.

The past is gone

The real fad for personal money management only hit Taiwan in the mid-1980s. It was then that the country's accumulated economic resources began to come to the surface. The huge trade surplus built up over many years caused the NT dollar to appreciate, and attracted a huge amount of speculative foreign money into Taiwan. The stock market index rose from 600 or so in 1985 to more than 12,000 by 1990. Meanwhile, the price of property rose from an average of NT$71,800 per ping (about 3.3 square meters) in 1986 to NT$284,500 per ping in 1989.

At that time, great opportunities for making money stared one right in the face. In pursuit of overnight wealth, many people mortgaged their property to buy stocks, and then used their stocks as collateral to borrow more money, creating a vicious cycle that laid the foundation for the burst bubble and huge debts of later years.

But, having reviewed the past, Chia Chen-i declares: "In money management, you can only look to the future; there's no point in regretting what's gone." Indeed, in the era of the Internet, with everything moving much faster, investment indicators like product popularity and employment trends can change overnight. Those who cannot see the trends or who cannot react fast enough are doomed to be the losers in the wealth game.

Take for example the case of Mrs. Chang. Widowed at an early age, for over 20 years she supported her family as an independent real estate broker. Her success made her very confident about her understanding of the property market. Six years ago, she decided to help the family of her younger brother, who contracted a terminal illness, to buy a new house. At the time, the price of high-rise apartments in the Tanshui New Town had fallen from NT$220,000 per ping to NT$150,000. Congratulating herself on getting a low price, and confident that the market would rebound, Mrs. Chang happily put down the first payment and watched her brother's family move in.

However, it was about this time that many new projects-started earlier by construction firms hoping to take advantage of peak prices-came on the market. The number of empty units rose to over one million. Next, increased cross-strait tensions put a further damper on the property market. The September 21 earthquake last year was the final straw. Today you can find high-rise apartments in Tanshui New Town for as little as NT$110,000 per ping. Mrs. Chang's brother's family is stuck with a heavy mortgage, and there are constant recriminations between Mrs. Chang and her nieces and nephews.

Will the Taiwan property market inevitably recover? Not necessarily. Looking around the world, at the US, Japan, Hong Kong, and even mainland China, there are countless examples of long-term downturns in the housing market. The popular book Die Broke notes that the sharp rise in housing prices in the US in the 1960s and 1970s was due to underlying structural factors: The large generation of "baby boomers" were starting careers and families, thereby increasing demand for housing. At that time, some of the older generation about to retire happily sold their houses to the younger at high prices. The large profits they earned attracted numerous speculators into the market, and prices were driven even higher, encouraging construction of ever more homes. But now that most of the baby boomers have their own homes, and the current "e-generation" is smaller, who are all those extra homes going to be sold to?

Snafu

The upshot of all this is, as Hsu Yen-shan, chairman of the Department of Finance at National Chengchi University, cautions: "There are no absolute experts at money management." So-called experts are simply those who have particular knowledge about a certain sector in a certain place at a certain time. But you know the old saying: "People have two feet, but money has four." Trends change faster than most people can anticipate. No wonder the "stock masters" featured on cable TV usually disappear from view after a brief reign, only to be replaced by equally short-lived successors.

In the past two years, perhaps brainwashed by money management dogma that says "the early bird gets the worm," investors have swarmed like bees for the latest fads, sometimes jumping in even before the true value is known. The US NASDAQ index, which has a history of 29 years behind it, suddenly surged from 2800 in October of last year to more than 5000 by March of this year. Telecommunications, Internet, and biotechnology stocks soared. The price-to-earnings ratio of some individual stocks reached 500, which some ridiculed as the "price-to-dream ratio."

"Investors sometimes act as if they don't care about a company's current losses, but simply put all their faith in the distant future. Unfortunately, the farther in the future something is, the more likely it is that expectations will be wrong," points out Chiu Shean-bii, a professor of finance at National Taiwan University. Beginning in mid-March of this year, NASDAQ high-tech stocks plummeted. For many investors, earnings accumulated over many years disappeared in a matter of weeks.

The misguided idea that "what is new is better" also has been a problem in Taiwan. A certain "Mr. Wang," who works in the government, last year thought he would jump on the bandwagon for telecom and Internet stocks. He borrowed money to purchase 80 blocks of shares, at NT$13 per share, of fixed-line Internet network stocks, which hadn't yet even been listed. When the price fell to NT$11 per share, he still didn't worry, thinking that "so long as I don't sell, the loss won't be realized." Little did he expect that the new government would clamp down on illegal trading in fixed-line network stocks. Suddenly his whole investment-well over NT$1 million-has been frozen, and all he can do is stand on the sidelines in a state of panic.

To be sure, ignorance of new trends is not recommended, but looking too far into the future can also lead to disappointment. Indeed, in this information era, money management may even be getting more difficult. Strange to say, but the explosion of money management information, which should in theory make investors' lives easier, does not.

As Chiu Shean-bii says: "There's plenty of information out there, and there are so-called experts everywhere. But the result is that investors don't know what to believe, and find it even more difficult to make a decision."

Moreover, often even the best information and analysis is no match for sheer luck. Cabula Chang, editor-in-chief of the money management website SmartNet, describes a case in point. Last year, one of the hottest stocks was Quanta Computers, which reached 800 per share. The story goes that there was an old grandmother who followed the crowd in and out of the stock, earning a huge amount in the process. Afterwards, she asked: "What I still don't understand is, how can selling pork jerky be so profitable?" It turns out that she thought she was investing in a dried-pork company of the same name, and those who heard her question nearly fainted with disbelief.

Money management madness

The fever for money management has in fact disrupted the lives of many people, and brought a lot of headaches. However, Jessica Liu, associate director of the Taipei branch of UBS, who has written a number of books on money management, says that there is no turning back. Whenever some people get ahead, others will follow, and no amount of calls for simpler lifestyles or new value systems can stop them.

The reason is very simple. "The money management fever is a natural product of changing times." According to Liu, individualism and the rise of urban commercial society have broken down the support networks of traditional agricultural society. In addition, since the 1980s Taiwan has been swept up in the globalization of capitalism. Rural society has disintegrated, and traditional industrial sectors have withered, as newly rising electronics and information industries have appeared one after another. These rapid changes have brought the threat of unemployment or early retirement to many individuals. In order to cope with the increasing uncertainty of life, it is necessary for people to build up a nest egg.

Liu says: "If you have NT$30 million in the bank, you don't care whether you have to retire or not. What's important is that you don't have to worry about the future, and live in fear that a sudden loss of your salary could ruin your life."

Of course, everyone feels a different sense of urgency about the uncertainties of life. Sometimes, in fact, this can become a source of interpersonal friction. "Miss Chen" of Pingtung worries that her father, soon to retire at age 60, doesn't think much about money, and his expected retirement plus savings will be less than NT$4 million (about US$120,000).

You manage, I benefit?

As Miss Chen does not hesitate to say: "My Mom and Dad still think that it would only mean an extra set of chopsticks on the table for them to live with their daughter. It seems they haven't realized yet that they may live to be 85. They haven't made any preparations for living expenses, vacations, or the enormous medical expenses that can be expected over the next 25 years." She has encouraged her parents to put part of their savings into a mutual fund or the like, but without success. Indeed, the issue has become a sore point between her and her mother.

Meanwhile, the changes in the larger environment that are making people anxious about their economic security are boons to companies trying to market financial products. A certain American bank has recently been doing "carpet bombing" advertising with slogans like "One out of every two people wants to retire ten years early, but hasn't yet begun a financial plan!" or "60% of parents want to send their children abroad to study, but one-third of these don't know how much money they should prepare!" It is said that these ads have been very effective.

Chen Yi-fen, vice president of the Individual Banking Department at Fubon Bank, speaking as someone who has been closely following this problem from the sidelines, reminds consumers that no matter what the source-advertising, websites, or whatever-though advice may be cloaked in a halo of expertise, the motive is to sell products and to earn money from the financial activities of clients. Chen says: "It's like those ads for milk that emphasize how fearful osteoporosis is. The problem is, they don't tell you that milk is by no means the only way to prevent this, or even the most effective."

It ain't over till it's over

Another factor driving "investment anxiety" is peer pressure.

"If a 40-year-old does not have a securities account, he won't be able to engage in conversations with his peers about the market, so naturally he will feel out of touch," says Cabula Chang. Chang admits that he still lives in a rented house in Tanshui. His wife wonders why his colleagues in the financial management community are multi-millionaires, while he still has not had his rendezvous with fortune.

Chang tells his wife that one should not compare oneself to others. Their success may be temporary or even illusory. A number of his friends who had insider information were quite proud of themselves when they profited from the rise of Taiwan Pineapple to more than 200. But within less than two years, the stock collapsed and became worthless paper. Chang recalls an inexperienced reporter who got sucked in to the market two years ago by some irresistible insider information. He even mortgaged his house and persuaded his friends to invest with him. Today, he still has not got his head above water.

Chang says, "The longer I'm in this business, the more I feel that you can't get anywhere by trying to get ahead quickly." Investment options are like churning whirlpools; of course you enjoy the ride as long as you are on top of the water, but currents shift, and eventually you may get sucked down. "In investing, until the final moment, you never know whether you've won or lost."

Jessica Liu, who personally feels little anxiety about money management, points out that one of her core principles for investing is to not compare herself with others. "This is because I know that opportunities to make money come and go. If I don't make a lot this wave, there'll be another wave later." She says that anxiety rises in direct proportion to a person's expectations and desires. The more you want, the more anxiety you feel, and the greater will be the sense of disappointment if you fail. In other words, anxiety derives from greed.

"If you buy TSMC at 150 hoping it will go up to 220 within a couple of months because that's what you need to make your final house payment, then it only goes up to 200, you'll feel dissatisfied," says Liu. This sense of disappointment is completely due to the lack of a proper money management outlook.

People in middle age invest in hopes of finding a sense of personal security. But members of the e-generation often have more specific objectives in mind. Lin Yu-ting, currently a sophomore in the Department of Financial Management at National Chengchi University, puts the money she makes working part-time into the market. She says that she has "a specific plan for each period of time, such as going abroad, or buying a car." So her aim is "to manage my money so that I can spend it!"

Lin's classmate Ou Chien-ming says that he has always wanted to save money to go traveling with his girlfriend. Last year, after vacillating for quite a while, he finally borrowed NT$80,000 from his mother to invest in stocks, under the assumption that, by putting to use what he was learning in school, it wouldn't be that hard to make a good return. Alas, he put his faith in the predictions of a certain investment adviser, and put everything he had into securities stocks, which stagnated. After the election of Chen Shui-bian as president, he mistakenly assumed that the market would go down, and sold everything without even looking at the share prices. He ended up selling at the low point, and his dream of going abroad is even farther out of reach than it was before.

Healthy money management

Chiu Shean-bii of National Taiwan University was told in a recent meeting with the general manager of certain large American commercial bank: "Asians always ask: 'Is the market going to go up or down tomorrow?' But investment advisors are not weather forecasters, and we don't pretend that we can know the future." This banker says that his money management target is not to make a specific profit within a specific time, but to use a variety of financial instruments-including defensive investments like insurance and reliable ones like savings, as well as an active investment portfolio-to appropriately diversify his assets. He seeks to "build a Noah's ark. When the weather is good, you can make a little more progress, but when storms hit, you can ride them out."

Chen Yi-fen, who comes across all manner of money management plans every day, often wonders about the meaning of it all. She says that today banks are always talking about how they want to provide every individual with tools to "intelligently manage money." For example, they provide credit cards that award bonus points, housing loans with built-in short-term overdrafts for investment, and even mutual fund accounts that will automatically invest a specific amount at fixed times. But how much money is enough? That depends on the values of the individual.

"Each individual should choose a lifestyle and belief system that they feel comfortable with, and not just follow the crowd," says Chen. After all, in a pluralized society, there should be more than one definition of success.

Recently there was a news story about the old author Chang Tuo-wu having to sell lottery tickets on the street. One financial expert took Chang as an object lesson to "warn" people to learn how to manage their money. Yet, looking at this another way, if Chang had spent his youth worrying about accumulating money, he would not have had the experiences he did and made his way from being an ordinary soldier to writing such moving works. In the end, there are no numbers that can validly measure what has been gained in life, and what lost.

It is said that the two biggest causes of family arguments this year have been differences over who to vote for in the presidential election, and over what stocks to buy. As Jessica Liu reminds us, money management, like life itself, is an accumulation of small experiences, a long road with ups and downs, and so should be faced with equanimity. After all, isn't the point of making money to have a better life? But if you lose your sense of fun, your health, or your friends and family in the process, and if you win the money game only at the cost of losing the game of life, what kind of a return on your investment is that?

[Picture Caption]

Credit cards are the new darlings of the e-generation, but this "simple swipe" can be fatal to money management.

Although there are new personal finance channels, such as the Net and personal digital assistants, the traditional securities firm trading floors are still places where investors gather to pick up rumors and gossip.

In the future, through WAP-compatible mobile phones, investors can easily trade their shares without going through brokers.

Real estate was once a "hot property" in Taiwan, but is now generally avoided. In particular, after years of landslides and debris flow in mountain areas, there's little interest in the large number of hillside villas.

People are living longer than ever, and a major motivation for money management is to prepare for an extended post-retirement life.

Personal Money Management

Plan for Life

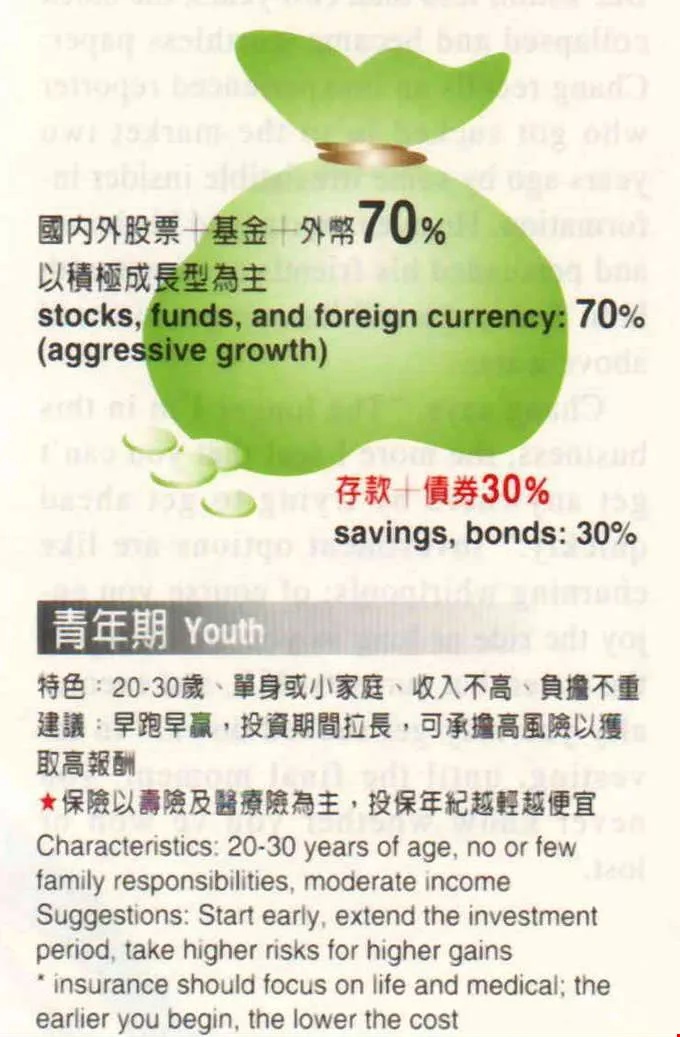

Youth

Characteristics: 20-30 years of age, no or few family responsibilities, moderate income

Suggestions: Start early, extend the investment period, take higher risks for higher gains

* insurance should focus on life and medical; the earlier you begin, the lower the cost

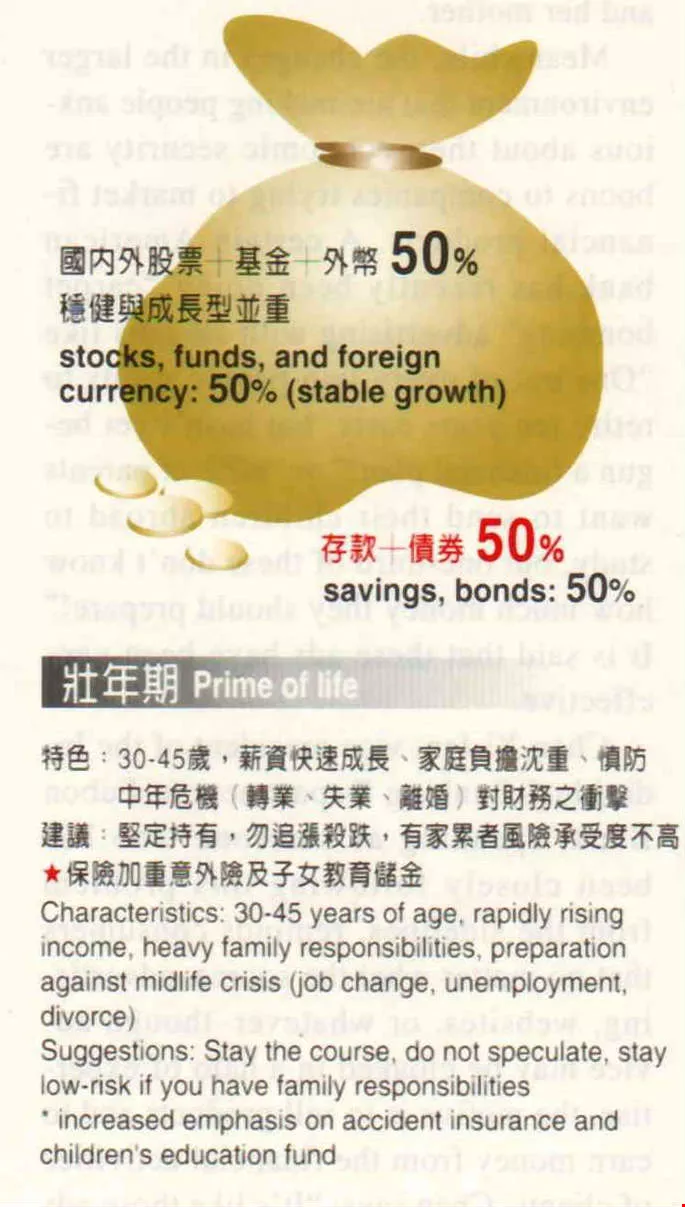

Prime of life

Characteristics: 30-45 years of age, rapidly rising income, heavy family responsibilities, preparation against midlife crisis (job change, unemployment, divorce)

Suggestions: Stay the course, do not speculate, stay low-risk if you have family responsibilities

* increased emphasis on accident insurance and children's education fund

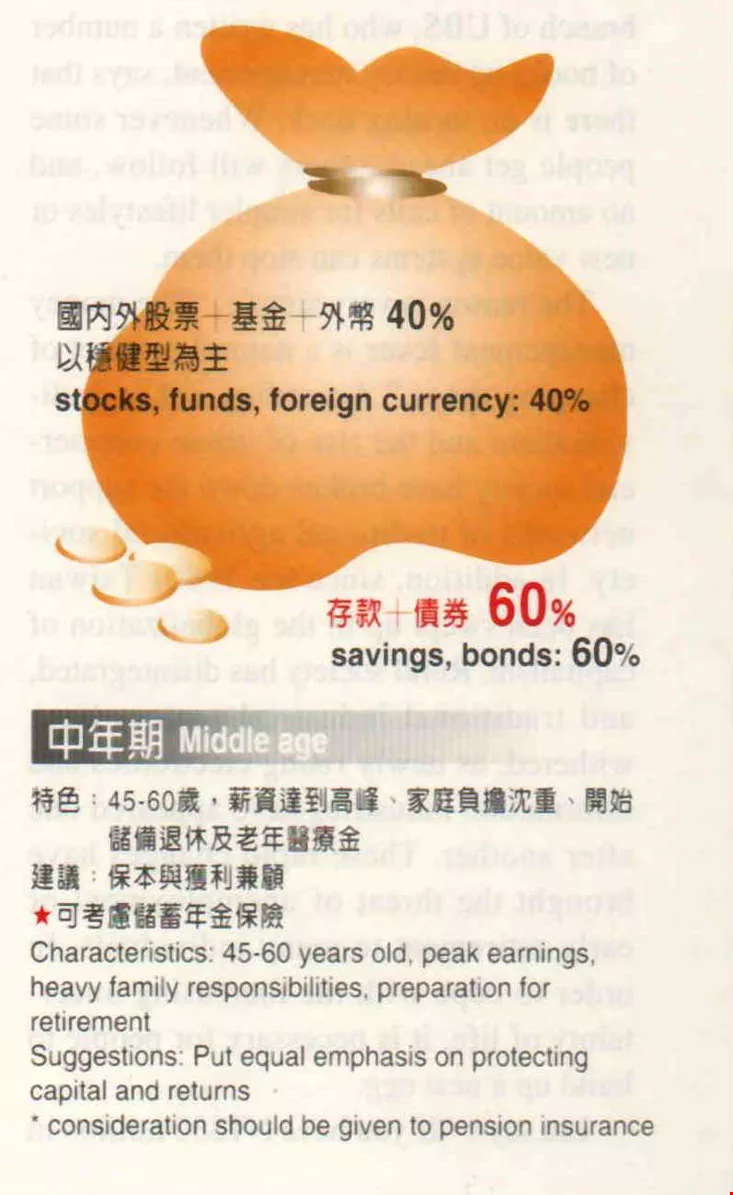

Middle age

Characteristics: 45-60 years old, peak earnings, heavy family responsibilities, preparation for retirement

Suggestions: Put equal emphasis on protecting capital and returns

* consideration should be given to pension insurance

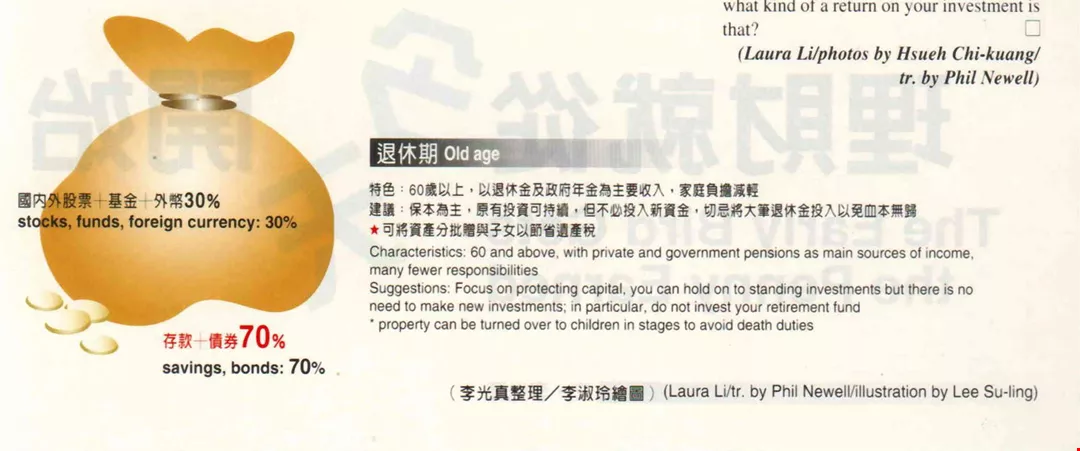

Old age

Characteristics: 60 and above, with private and government pensions as main sources of income, many fewer responsibilities

Suggestions: Focus on protecting capital, you can hold on to standing investments but there is no need to make new investments; in particular, do not invest your retirement fund

* property can be turned over to children in stages to avoid death duties

Although there are new personal finance channels, such as the Net and personal digital assistants, the traditional securities firm trading floors are still places where investors gather to pick up rumors and gossip.

In the future, through WAP-compatible mobile phones, investors can easily trade their shares without going through brokers.

Real estate was once a "hot property" in Taiwan, but is now generally avoided. In particular, after years of landslides and debris flow in mountain areas, there's little interest in the large number of hillside villas.

People are living longer than ever, and a major motivation for money management is to prepare for an extended post-retirement life.

Youth Characteristics: 20-30 years of age, no or few family responsibilities, moderate income Suggestions: Start early, extend the investment period, take higher risks for higher gains * insurance should focus on life and medical; the earlier you begin, the lower the cost.

Prime of life Characteristics: 30-45 years of age, rapidly rising income, heavy family responsibilities, preparation against midlife crisis (job change, unemployment, divorce) Suggestions: Stay the course, do not speculate, stay low-risk if you have family responsibilities * increased emphasis on accident insurance and children's education fund.

Middle age Characteristics: 45-60 years old, peak earnings, heavy family responsibilities, preparation for retirement Suggestions: Put equal emphasis on protecting capital and returns * consideration should be given to pension insurance.

Old age Characteristics: 60 and above, with private and government pensions as main sources of income, many fewer responsibilities Suggestions: Focus on protecting capital, you can hold on to standing investments but there is no need to make new investments; in particular, do not invest your retirement fund * property can be turned over to children in stages to avoid death duties (Laura Li/tr. by Phil Newell/illutration by Lee Su-ling)

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)