Reflections after the Default Crisis

Laura Li / photos Diago Chiu / tr. by Scott Williams

January 1999

How many of the mighty have fallen? Business groups involved in major defaults in 1998:.

The aftermath of the Asian economic crisis made 1998 a rough year around the world. Of all the nations of the East Asian "disaster area," only Taiwan has maintained nearly 5% economic growth. When compared to the negative growth rates seen in Japan, Korea and Hong Kong, this is a noteworthy achievement.

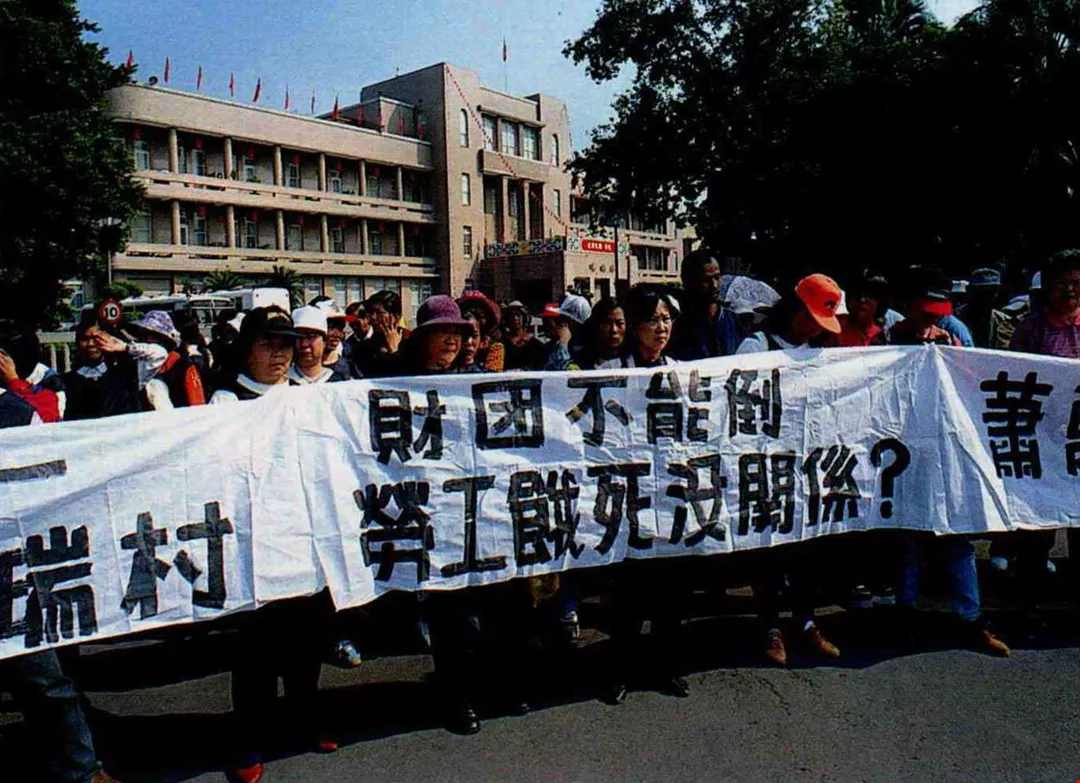

There is no question that the government's financial relief policies have eased the effects of the crisis. However, they have also unexpectedly stirred up labor protests. (photo by Pu Hua-chih)

However, just as the world's media is lauding Taiwan for this economic success, news is beginning to emerge of defaults and bankruptcies at local firms. The local business community has become anxious, and firms are trying to protect themselves. Is the strength of Taiwan's economy just an illusion? Has the regional financial crisis caught up with us?

At the end of last September, Tong Lung Metal, the manufacturer of world-renowned Lucky brand locks, was reported to have defaulted on stock transactions. Within a few days, it was also reported that Chou Chi-rui, the chairman of the U-Land Group , which owns Air Philippine, the second largest airline in the Philippines, bounced a large check.

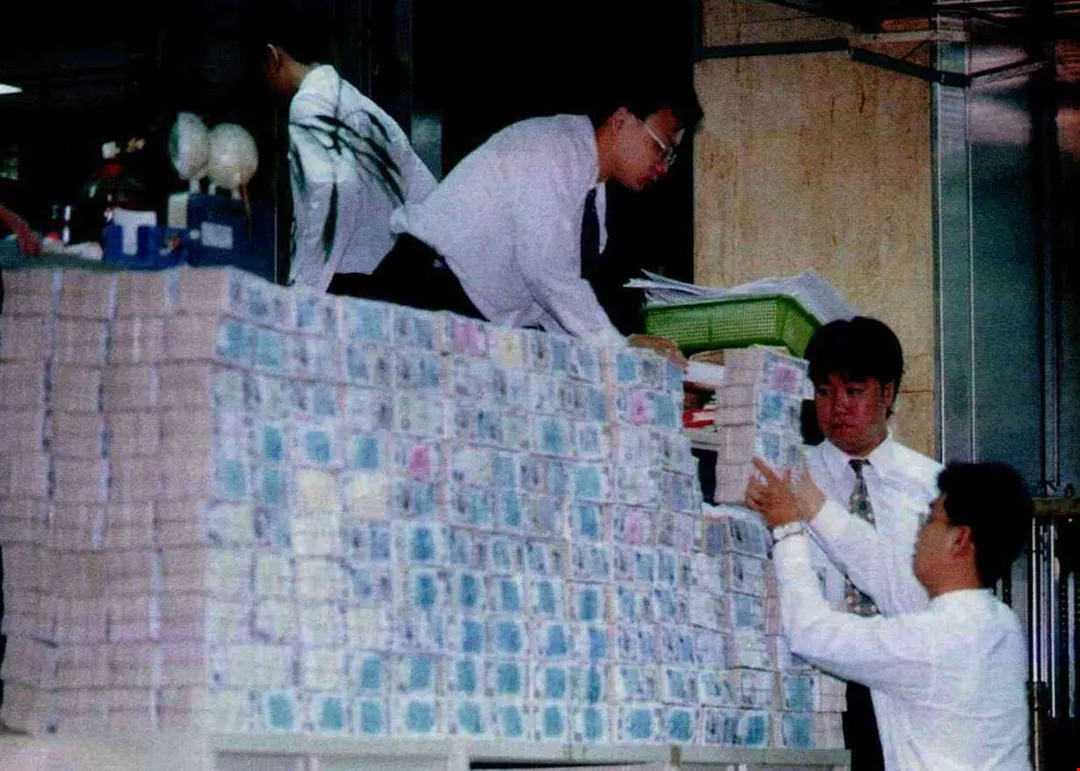

Revelations of improper loans made by the Medium Business Bank of Taichung set off a run on the bank. In just one day, NT$5 billion was withdrawn. Fortunately, a transfer of funds from the Ministry of Finance and the Central Bank of China stabilized the situation. (photo by Tsai Ming-te)

At the end of October, Rajah Construction bounced a check. Then news came out that the well-known New Magnitude Group, which controls several stock-market-listed companies, was having financial difficulties. On the same day, the financial situation at the Panvest Group became tense. . . . In the short space of two months, nearly 10 major business groups experienced troubles, causing share prices and trading volumes in their more than 10 listed affiliates to tumble. It has also led to wide fluctuations in the overall stock market, and distraught wails from investors (see table).A landslide?

This wave of bounced checks and defaults struck suddenly. Ho Hsi-fong, chairman of the Han Yang Construction, wept during a press conference called after crisis had struck his company. He said the difficulties arose so quickly, it was like being caught in a landslide.

The cross investments and mutual guarantees of credit that exist between these companies and financial institutions mean that there are a large number of companies out there with debts in excess of NT$10 billion. As a result, Central Bills Finance, Hung Fu Bills Finance and the Medium Business Bank of Taichung are all facing write-offs and restructuring.

Just how serious is this recent defaults crisis? The local media has been describing it as Taiwan catching the caboose of the global economic train wreck and feels that the island's financial environment has markedly worsened. The Ministry of Finance (MOF) and the Central Bank of China (CBC) are also taking the situation seriously. They have come up with a number of new policies and approaches to deal with the situation, including prohibiting banks from holding back credit. The MOF and CBC have also announced a relief package aimed at pulling troubled companies through their difficulties.

As of December 16, the relief task force had received 70 applications for aid, most from small- and medium-sized enterprises (SMEs) with only slight problems who hoped to make use of this new resource. With coordination and information provided by the task force, about half of these have already received aid.

In order to provide timely service and prevent the contagion from spreading to "innocent" companies, the MOF has instituted a new "one-stop" service for processing applications and providing aid.

"In the past, firms seeking aid first applied to their primary creditor bank. After a preliminary evaluation by this bank, their application went to the government task force for review. Now, however, firms apply directly to us," says a senior MOF official.

In addition to this aid to firms, the MOF created a stock market stabilization committee in mid-November which was announced to have more than NT$200 billion at its disposal to support the market. It has also implemented unprecedented measures to prevent a collapse of confidence in the market, including the temporary suspension of trading of shares in problem companies and the institution of extra-market trading in such shares. The amount of funding arranged for emergency lending, even greater than that arranged during the 1996 missile crisis with mainland China, reveals the how seriously the government is taking the problem.

But in contrast to the government's marshaling of its forces, most business people are not very concerned. Bert J. Lim, head of the World Economics Society, uses figures to make his point. Lim states that losses resulting from these bounced checks amount to only NT$200 billion or so. This compares to total daily capital turnover of NT$15 trillion in Taiwan. Markets should be able to absorb such a relatively small amount. Lim feels that the media has exaggerated the problem, making it sound as if Taiwan is on the verge of collapse.

Casper Shih, who as head of the Global Chinese Competitiveness Foundation has long been involved in industrial consulting, also feels that this has not been an across-the-board crisis, and thus is not that serious. With the passing of the December elections, the post-election explosions of the so-called "land mine shares" which some predicted has not come to pass. It looks like the situation is under control and will not continue to worsen.

"Don't talk about the tragedy. Stabilize the situation, then take some time to think about what comes next," says Chan Tien-cheng, chairman of Yi Jinn Industrial, giving voice to the unswerving spirit of Taiwan's entrepreneurs.

On the other hand, S.T. De, chairman of the National Association of SMEs and of San Sun Hat and Cap, gives the government a score of 98 out of 100 for its rapid implementation of relief measures. In De's view, it is fortunate that the government acted as quickly as it did. Had it not, rumors flying through the business community would have caused banks to cut off credit and businesses to fear placing orders. A collapse of confidence would have resulted. Real mountains would have grown out of molehills, and the situation would have been difficult to control.Avariciousness?

According to Casper Shih, one thing worth celebrating in the recent crisis is that all the companies that encountered problems were of a similar type. He says that the heads of these groups have similar backgrounds, applied similar methods and failed for the same reasons. Knowing the cause of the problems and their symptoms, you simply need to administer the correct medication; it's not a very difficult situation to deal with.

Looking closely at the chairmen of these various groups, one notes that many began in the construction business and made a killing when housing prices in Taiwan were sky-rocketing 10 years ago. With the extended slump of the Taiwanese housing market over the last few years, they have directed their energies into the stock market. But because the terms by which construction companies can be listed on the stock market are extremely stringent, many of these business people have opted for a shortcut to listing-buying a controlling stake in an already-listed company. Examples include the Han Yang Construction, which got itself listed by purchasing a controlling interest in Kuo Yang Construction; the U-Land Group, which listed via King Textiles (formerly Hwang Dih Lon Textiles); and the Kuang San Group, which used Tai Yu Products to get itself listed.

After acquiring a listed company, the company holds a rights issue, squeezing money out of stock market investors. The money acquired from the rights offering is then used to establish a subsidiary which purchases shares in the parent corporation. Cross-holdings between the parent company and the subsidiary are not only used to raise share prices, but can also be taken to the bank where they are used to secure loans.

Most firms feel that caution and focusing their energies on improving their competitiveness in their core businesses are the only way to truly make it through the financial crisis. The picture shows Formosa Taffeta's Touliu factory, which produces dustresistant, anti-static fabric and reflective fabric.

Joseph Chiu, vice president of research at Taiwan Securities, says that a share with a market value of NT$30 can be used as security for a loan equal to 60-70% of its value, in this case, around NT$20. But if share prices can be pushed up to NT$70, that same share can now be used to borrow more than twice as much money. Eighteen months ago, in the wake of the first wave of the Asian financial crisis, the MOF was very concerned about supporting share prices. It therefore raised the margin lending ratio and lowered the margin maintenance ratio, making it still easier for these companies to raise money. Firms were only too happy to borrow up to the limit of their margin accounts and use the money to rapidly expand the scale of their operations through investment.Living and dying by the stock market

This method of using money to make money and using debt to maintain debt worked fine when the economy was good. But in the wake of the Asian financial storm, the entire world has experienced an economic slowdown. Taiwan, too, has not been immune to its effects. Figures from the Council for Economic Planning and Development show that for seven months during the period from April to November of 1998, the domestic economy was in a period of slowdown, and in October, it was actually in recession.

The economy is struggling and the stock market is down. Returning to the stock-secured loans mentioned above, if the price of shares used to securitize loans drops below 120% of the amount of borrowing which they secure, the lending institution sells the shares. To avoid having their shares sold off, these tycoons, who were such able stock market operators when the economy was sound, had to devote their firm's entire resources to defending their share price. This made it difficult to employ their capital effectively-they lived and died with the market.

The fact that such stock-secured loans are ubiquitous is worrisome. According to data from the Securities and Futures Exchange Commission (SFEC), as of September 1998, a significant percentage of the directors and supervisors at more than 60 of Taiwan's listed companies, or nearly 15% of the companies listed on the main board, have taken loans of this sort: at 17 listed companies more than 90% of the share holdings of directors and supervisors are securing loans of this sort; at another 20 companies 80-90% of the holdings of supervisors and directors secure loans; at a further 30 companies, 70-80% of such holdings secure debt.

"Of course, there will not be a crisis at every firm. But by borrowing so heavily, they have left themselves little room to maneuver. You can imagine how difficult it is for them to keep capital moving quickly to where they need it," says one person in the securities industry familiar with the situation. He says that even a slight slip-up could be the straw to break the camel's back. This is one reason the government must support the market.

The media has been closely following every word and deed of Minister of Finance Paul Chiu, who is in charge of the efforts to provide relief to local businesses. (photo by Wang Hsing-tien)

The MOF has been striving to do this very thing, and has led the relief efforts. And the CBC, which controls monetary policy, has been providing its full cooperation in creating a loose capital market. "Luckily, the US dollar has been softening. Since there are fewer worries about depreciation in the NT dollar, interest rates can fall," says Casper Shih. In Shih's opinion, if the defaults crisis had occurred a few months earlier when the government was struggling to support both the stock market and the exchange rate, Taiwan's situation could have been like that of other East Asian nations, unable to either advance or retreat. If nothing else, the timing of the explosions of these financial "land mines" on Taiwan is worth celebrating."Less investment. Less investment."

In comparison with East Asia, especially Japan and Korea, Taiwan has another ace in the hole-its numerous strong and vigorous SMEs. Although several dozen SMEs have applied to the government for aid, when one considers that there are around one million SMEs on the island, the percentage experiencing problems is quite small. With the current crisis afflicting mostly large firms, SMEs-"Taiwan's treasure"-are being looked at once again.

"These large groups have always laughed at us SMEs for not having any idea about financial legerdemain," says C.J. Lin, head of Proton Electronics. But now, not having huge ambitions and not having the power to do whatever they like are looking like assets for these SMEs.

Returning to the large firms, the groups affected by this current crisis account for about 3% of the Taiwan Stock Exchange's total capitalization. Have the companies with which they do business also been affected? What view should producers take?

"All the 'land mine' shares that should have blown up have pretty much done so. If those that are left pull back, if they stop before it's too late, they should be able to avoid misfortune," says Chan Cheng-tien, chairman of Yi Jinn Industrial and of the Taiwan Synthetic Texturized Industry Association. Chan laughingly says that whenever the chairmen used to get together, their conversation revolved around investment. But when they see each other now, they remind each other, "Less investment. Less investment."

Chan says that the U-Land Group's King Textiles is a customer of his Yi Jinn Industrial. Fortunately, although King Textiles is facing financial losses, its operations are sound and it is still making shipments as usual. But King Textiles doesn't have the cash to make debt payments. "It is selling the us fabric it produces to repay debt. Besides, we have a textile plant that can absorb their production, so there is no loss to us," says Chan.Cooperating to get through the crisis

Ching-tai Resins Chemical, a company which holds 20% of the domestic water-proofing materials market, was also affected by the financial crisis at U-Land Construction. U-Land stopped work on a project, so one of Ching-tai's clients, a contractor specializing in water-proofing projects, was forced to return a shipment of materials to Ching-tai. Although the cost of water-proofing materials at one construction site may only amount to something under NT$1 million, to an SME capitalized at only NT$200 million, this is not small change.

"Fortunately the materials hadn't been used yet. Our only losses were personnel and transportation costs," says Liao Ta-shang, president of Ching-tai. He notes that compared to big contractors and steel structures firms which rely on one or two large jobs a year to make their money, their losses weren't bad at all.

"The links between Taiwan's upstream and downstream firms are very solid, and everyone tends to stick together," say Liao. He further states that in the case of this kind of sudden crisis which causes firms to return goods or be late with payments, everybody tends to yield a little and distribute the losses to get through. Everyone hopes for long-term cooperation, and forcing the collapse of a downstream client certainly isn't in your own interest.

What makes the current crisis more of a headache is that the firms most affected are big ones which have no history of bouncing checks. Most companies don't have the resources to conduct credit checks on their customers. Liao says that in facing the likelihood of further bad orders and returned shipments in the future, you can only accept that you can't cover every contingency.

C.J. Lin, however, states, "This current wave [of troubles] is no storm." Lin, accustomed to the rapid changes and high risks of the electronics business, says that in running a business, you can't expect every year to be a banner year. The smooth sailing of recent years has allowed people to forget that the usual situation in the market is that the strong succeed and the weak fail. He offers the following words of advice to his fellow business people, "Be conservative with your finances and aggressive with your core operations." Lin expresses the hope that everyone has learned something from these recent troubles.

William B. Lin is deputy managing partner of Deliotte Touche Tohmatsu International, a firm which currently provides auditing services to 80-90 listed companies. Lin states that although there is a never-ending supply of rumors on the market, difficult financial straits are not the norm at the 1,000 or so large and small firms his company has audited.

Lin believes that Taiwan's businesses are very responsive and capable of making adjustments. For example, when the Tuntex Group encountered troubles, chairman Chen You-hao called a press conference. He both put an end to the rumors and took the necessary actions to keep his company afloat, announcing that it would eliminate its construction division and focus on its core businesses-textiles and petrochemicals. Another example involves Yang Tien-sheng, the chairman of Pan Asia Bank, also known for his political connections. Under pressure as the bad debt ratio at his bank crept upward, Yang has announced that he is willing to allow another entity to take over the ownership and operations of Pan Asia. If the chairmen of these business groups can break away from the mistaken idea that they must blindly expand and can pull themselves out of trouble, the current situation should be manageable.A personal philosophy

But many people in business say that resolving the "land mine" problem is just an initial step. Changing the business climate by persuading businesses to refocus themselves on their fundamentals is the long-term task.

S.T. De says that many firms have gotten caught up in the enthusiasm for the stock and foreign exchange markets over the last few years. The reason is that a finance department with a staff of only 10 or so can add hundreds of millions of dollars a month to a company's income. This is more than the more than 100 persons working in production, sales, and research and development earn for the company in a year. That being the case, what company wants to work hard for its money?

De, who claims to have been involved in only one stock transaction in the last 10 years, experienced a lot of pressure last year when the government was struggling to hold the NT dollar-US dollar exchange rate at 28 to 1. He himself stated to the media that the NT dollar was about to undergo a large depreciation. With this kind of foresight, all he had to do was sell NT dollars-essentially just hold out his hands-to reap a foreign exchange windfall. But he didn't and was called an idiot by his friends because he didn't.

"It just wasn't worth it to let financial manipulations take precedence over the hard work of my entire staff to make a few hundred million dollars. It would have destroyed the company's structure and its development of its fundamentals," says Tai. But his "stupid" personal philosophy has now been proven correct.

Just as a company must build sound ideas and practices within itself, so must the national economy.

Over the last few years, market players have bought access to the stock market through shell companies and taken on a "heroic" aspect. An example is the Han Yang Construction's Ho Hsi-fong, who in just a few short years accumulated a personal fortune of more than NT$100 billion. Or the New Magnitude Group, whose companies, because their share prices seemed to defy gravity, became a target for retail investors' purchases just before the group ran into trouble. Almost without exception, the chairmen of those companies which have recently encountered problems-Panvest, the An Feng Group, Hung Fu Bills Finance-were famed for their excellent political connections.

William Lin says that the "heroic" style of a few business groups has caught the attention of the media, but very few people have actually thoroughly investigated or been critical of this style of doing business. This abnormal situation has swayed the hearts of many business people. The many who stuck to the slim margins of their core businesses were viewed as fools. As a result, seemingly everybody then jumped on the "play the market in the morning, play golf in the afternoon" bandwagon, competing to see who had the least to do and who had the most money.Why not let the weak ones fail?

Taiwan Securities' Joseph Chiu observes that in this defaults crisis, the government has tended to focus on how to provide relief to companies, rescue the stock market and keep liquidity in the capital markets. But in fact, capital markets are not tight right now. It's just that financial institutions are unable to find good companies to which to lend money.

Chiu says that this defaults crisis wasn't caused by mainland China launching missiles or by an implosion of currency exchange rates. Instead, it was caused by the poor management of domestic companies. He wonders why the government doesn't take it in stride and let market forces do their work. "If the government wants to exert itself by propping up the stock market, how is this any different from these big groups supporting their own share prices? They will get themselves into a position where they have to keep on doing it," states Chiu.

Facing these kinds of doubts, an official at the MOF states that these relief measures are aimed at "firms whose operations are normal but are facing short-term capital flow problems." Firms whose operations are abnormal are not receiving assistance from the government. Their losses cannot be turned over to the government, nor can they be borne by the public. The cases of Chinese Automobile and Kuoyang Construction, both of which have excellent political connections but nonetheless saw their applications for aid denied, demonstrate his point.

Looking more closely, the MOF's efforts to provide aid to firms and support the stock market are only rescue missions. In the long term, only adjustments to industrial policy will be effective.

"Sometimes policy doesn't need to be nice. The government could take this opportunity to make it clear that businesses must stand on their own two feet, and to list those points which are important to the development of strong industries in the future." Chiu uses the four industries which the financial community views as high-risk-construction, steel, textiles and food-to make his point. He says that these four industries have over-invested and profits are very thin. If they cannot come up with some way to add value, they face extinction.

Taiwan's resources are limited, and over the last few years we have been fortunate that the new information technology and semiconductors industries have been able to support the economy. Capital from the banking system needs to continue to flow to such outstanding industries to distribute the risk of bad loans. In the future, Taiwan must continue to strengthen these stronger industries while also developing new "star" industries. It is only in this way that Taiwan's economy can continue to move forward.Anticipating a rebirth

Looking at corporate structures, Lin observes that Taiwan's businesses are largely family-run. Boards of directors are usually controlled by a few members that the families of the major shareholders feel they can trust. As a result, they can do anything that they want to. The Kuang San Group's Tai Yu Foods is one of Deliotte Touche Toh-matsu's auditing clients. Between the company's quarterly review of the books, Tai Yu spent more than NT$9 billion to buy shares in other firms belonging to its parent company. However Tai Yu was not able to pull off the transactions smoothly, and when the news came out, the business community was shocked.

"In theory, shares of listed companies are distributed, and the company belongs to all its shareholders. In reality, these entrepreneurial families operate behind the scenes. Small shareholders only have the right to be ripped off," sighs Lin.

Chiu Shean-bii, a professor in the Department of Finance of National Taiwan University's College of Management, feels the same way. He says that there is no way the government can make daily checks on the books and finances of these companies. Hence, he recommends that it import the "outside director" concept long used overseas. In many nations, the law stipulates that the board of a company must contain some given ratio of "outside directors." These persons are well-known professionals who are not necessarily shareholders in the company on whose board they sit, but who nonetheless have the power to speak on and check the company's major policy decisions.

In Chiu Shean-bii's opinion, although the relief measures put forward by the government in this current crisis are not exactly legal, because they seem the best solutions to a no-win situation, no one is really blaming them. But emergency relief measures always have damaging aftereffects on the economy in the long term. If we are to both rescue these companies and put them on a sound foundation, the current problem is building a more comprehensive system of financial regulation.

Measures are being taken to fix the system. The Securities and Futures Exchange Commission is currently looking into regulations on cross holdings between parent companies and their subsidiaries, and is cracking down on insider trading and trading by friends and relatives of insiders. At the same time, financial institutions are reviewing their lending procedures.

"Everybody knows the direction we need to take to put things in order. It's just a matter of whether the government has the determination," says Chiu Shean-bii.

For the moment, the wave of defaults seems to have come to a halt. Looking to the future, getting through this downturn will not be easy. And rebuilding a proper attitude towards business is the only way to secure the soundness and stability of Taiwan's economy.

|

Groups hit by the crisis |

Date of crisis |

Related firms |

| An Feng Group | Late July | An Feng Steel, Feng An Metal |

| Van Yu Paper | Late August | Van Yu Paper |

| Tong Lung Metal | Late September | Tong Lung Metal |

| U-Land Group | Late September | King Textiles, U-Land Air |

| Rajah Construction | Late October | Ace Union Foods |

| Central Bills Finance | Early November | --- |

| Panvest Group | Early November | Chinese Automobile, Lei-Chu Enterprises, Chaplet System |

| New Magnitude Group | Early November | Pony and Goldenway, S&T Copper Industrial, CIS Technology, Taifang Development, Tycoons Group |

| Hung Fu Bills Finance | Early November | Hung Fu Construction |

| Han Yang Construction | Early November | Kuoyang Construction, Pan International |

| Taichung Machinery Works | Mid November | Taichung Machinery Works |

| Kuang San Group | Late November | Medium Business Bank of Taichung, Tai Yu Foods, Kuang San Construction |

(data collated by Laura Li/graphic by Tsai Chih-pen)