Househunting Blues--Young People in a Daunting Property Market

Lin Hsin-ching / photos Chuang Kung-ju / tr. by Scott Williams

July 2008

To people in their 20s and 30s,owning a home represents autonomy and fulfillment. Most dream of emerging from under their parents' wings and building their own nests.

However, soaring property prices have made it ever harder for young people of limited means to find a place of their own. Should they bite the bullet and buy, taking on a heavy mortgage and becoming a "slave" to their homes? Or should they lower their expectations and rent until they are better able to afford their own home? Today's young people are now wrestling with this very question.

One month after the presidential election, Taiwanese society was looking forward to things improving under President Ma. Consequently, when nine mainland Chinese tycoons worth a collective NT$500 billion arrived Taiwan on April 21 to check out the booming local real estate market, they attracted enormous amounts of attention from the media in Taiwan, mainland China, and Hong Kong.

The tycoons visited the Neihu Technology Park, Taoyuan International Airport, Taichung's Seventh Redevelopment Zone and Shuinan Trade Zone, and Pingtung County's Dapeng Bay National Scenic Area on their whirlwind four-day tour, and created a stir everywhere they went. Seeking major investments, builders and local government officials vied with one another to be hospitable to the tycoons.

But more people were concerned that the tycoons might just "flip" properties for a quick buck, thereby kicking off another round of unreasonable increases in real estate prices and leaving still more Taiwanese unable to buy homes.

Cross purposes

During the tycoons' visit, Taipei City councilor Wu Su-yao held a press conference accompanied by nine 30ish Taipei residents. He urged the government to address the issues of Taipei's soaring real-estate prices and the increasing difficulty young people are having purchasing housing before it opens up Taiwan's real-estate market to mainland investors.

"Chinese tycoons will be flipping buildings, while Taiwan's young people will be jumping from them!" exclaimed the nine young people at the press conference. Wu noted that their salaries, which ranged from NT$28,000 to NT$60,000 per month, weren't bad, but then presented figures from My Housing magazine showing that new housing in Taipei costs an average of NT$620,000 per ping (about 33 square feet) when purchased prior to construction. In other words, an average, moderately sized apartment of about 32 ping (1,000 square feet) costs nearly NT$20 million. At that price, the nine young people at the press conference would have to save every penny of their salaries, never buying so much as a cup of tea or a bowl of noodles, for 46 years to have enough money for a home.

But it's not like Taiwanese real-estate prices weren't rising before the mainlanders visited. In fact, they've been soaring for the last several years, and the increase has been particularly precipitous in Taipei.

According to the Taiwan Real Estate Research Center at National Chengchi University (NCCU), the average pre-construction price for new housing in Taipei City has risen 50% in the three years since 2005. Yet over the same period, Taipei's average household income has risen only 2%. Incomes simply aren't keeping up with real estate prices. The situation is even worse for young people, who tend to be at the low end of the income spectrum; the would-be homebuyers among them are being priced out of Taipei City.

Homes are incredibly expensive. Young people shouldn't let a moment's excitement or social pressures make them feel they have to buy. They should instead take careful stock of their means to put themselves on a realistic path to realizing their dreams.

Four bull markets

If we are to understand whether the price increases have been reasonable, we have to begin by looking at the changes in the Taiwan market over the last 30 years.

According to Chang Chin-oh, a professor with NCCU's Department of Land Economics, Taiwanese real-estate prices began fluctuating in the 1970s with the first global oil shock. The market rose strongly twice, first in 1973-74 and again in 1979-80. But Taiwan's economy and per-capita incomes also soared during this period, reducing the impact of the increase on homebuyers.

In the 1987-90 period, there was another across-the-board increase in real-estate prices. This time, it wasn't a global crisis that sparked the rise, but a loose-money policy aimed at enabling the government to acquire the funds to buy land for infrastructure projects. During this period, Taiwan's central bank was also attempting to protect Taiwanese exporters by preventing the NT dollar from appreciating strongly against the US dollar. To that end, it sold NT dollars and bought US dollars, effectively injecting liquidity into the market. Meanwhile, international hot money had discovered Taiwan and begun speculating in its stock market. The end result was that the currency rose sharply, the stock market skyrocketed to 12,000 points, and property prices increased by two to four times in just three years.

This brought on Taiwan's first home-buying crisis. Many people were shocked to realize that they could work hard their entire lives and still be unable to afford their own home. The crisis triggered 1989's Snails without Shells protests, in which some 10,000 people camped out overnight on Chunghsiao East Road.

The property bubble finally burst in 1990, and prices plummeted by as much as half in some areas. The market didn't begin to rebound until after the SARS crisis came to an end in the third quarter of 2003. Since then, prices have risen ever more sharply in what has become the Taiwan real-estate market's longest uptrend.

When buying a home, many young people fail to look beyond the three years of interest-only payments many mortgages offer. This kind of loan results in much higher payments from the fourth year as borrowers begin to pay back principal. They may also include provisions to raise the interest rate. Young people who don't have a clear understanding of their means may end up as slaves to their homes.

Highrise pigeon coops

In contrast to previous island-wide rises in housing prices, the current boom is centered largely in the north. The pricey Taipei City market has been especially overheated, while gains in the southern part of the island have been limited.

Hot-selling areas in central and southern Taiwan, such as Taichung's Seventh Redevelopment Zone and the neighborhood around the Kaohsiung Museum of Fine Arts, have seen prices rise to NT$300-400,000 per ping. But spaces in equivalent highrises in Taipei have for some time been selling for upwards of NT$1 million per ping. Elsewhere in the center and south, homes are priced at only NT$100,000-plus per ping in new buildings and frequently as little as NT$50-60,000 per ping in older buildings.

Chang Chin-oh explains that in recent years many Taiwanese traditional manufacturers have moved their operations from southern and central Taiwan to destinations overseas, which has reduced the number of locally available jobs and prompted residents to move elsewhere. It's no wonder then that housing is relatively cheap in these regions. The north, on the other hand, is home to the tech industry and the high-value-added service industries, and has consequently attracted large numbers of workers. The north's speedy, convenient transportation network, which includes Taipei's subway system, makes it even more attractive and exacerbates the "hot north, moribund south" situation that prevails in Taiwan's real-estate market.

Chang believes that the increases seen in the north in 2004-2005 constituted a normal rebound from the steep declines of previous years, but that the gains since 2006 have been the result of overheating as investors have pounced on efficiencies and luxury units. The so-called "luxury-apartment phenomenon" has intensified in the last year as builders have used their inclusion of extravagant amenities and high-tech features into their new projects as an excuse to raise prices still higher.

"Luxury apartments should be rarities designed for those at the top of the wealth pyramid," says Chang. "But there are luxury apartments all over Taipei City and County these days. These not only fail to meet the high standards of top-tier products in terms of materials, design, amenities and location, but are also pumping up the prices of ordinary apartments. These apartments, together with the foreign capital that has poured into the market, account for the abnormal skyrocketing of home prices."

Young people should also consider buying near the terminal stations of subway lines, where housing is less expensive than downtown. The photo shows a street scene in Hsinchuang, Taipei County.

Buying in Taipei not easy

The increases have been most dramatic in Taipei City. There, prices for pre-construction property have risen from an average of about NT$320,000 per ping in the first half of 2003 to nearly NT$540,000 per ping in the first quarter of 2008, an increase of well over 50%. Prices rose still further following President Ma's 20 May inauguration on news that direct links with mainland China and direct investment from the mainland would be permitted. In fact, home prices are up 6-7% just since the election.

A recent survey of the ratio of home prices to incomes of homebuyers found that it had risen to 10.4 in Taipei City from 8.6 in the last quarter of last year. In fact, the Taipei figure is higher than that of several of the world's top cities, including London (7.7), Vancouver (8.4), and Sidney (8.6).

The record high at which the ratio now stands indicates that people are having to save ever longer to be able to purchase a home. Consequently, homebuyers are getting older.

In the first quarter of this year, the average age of a homebuyer in Taiwan was 37.7 years, up 0.7 years from the fourth quarter of 2007. Taipei City homebuyers were, on average, the oldest in the nation at 39.2 years.

Homebuyers who don't have cash face staggering mortgages. The survey revealed that mortgage payments currently account for 33% of homeowners' incomes nationally and a record-high 43.6% in Taipei. In other words, Taipei homeowners are handing over 44 of every 100 dollars they earn, or nearly half their income, to their banks for mortgage payments.

Advertisements for homes for sale may be everywhere, but with prices frequently running as high as several hundred thousand NT dollars per ping, young people with limited incomes can do little more than look.

A house does not make a home

Lee Ming-tsung, a 36-year-old assistant professor of sociology at National Taiwan University, is well acquainted with the problem.

"My salary is in the upper-middle range for people in their 30s," says Lee. "But I can't afford one of Taipei's NT$500-600,000-per-ping homes. My only choice is to just keep on 'nesting' in one of the school's tiny housing units."

Kent is a 32-year-old man working in the media. Once content to rent, Kent is thinking about buying now that he has plans to marry his girlfriend in two years.

"But home prices in Taipei City are so high right now that we'll probably have to rent and continue to save for a while after we marry," he says. "Or see whether the real-estate bubble bursts and grab something cheap then."

Many young people are in much the same boat as Kent-planning marriage and wanting a home of their own in which to live their married life.

Sinyi Realty has sparked online discussion with a TV ad that says: "If he one day brings you here, congratulations! He wants to give you a lifetime of happiness." Stanley Su, director of Sinyi's Real Estate R&D Department, admits that the brokerage's first-hand experience with young clients provided the inspiration for the ad.

He says many Taiwanese still think "land equals wealth." Marriage therefore motivates many young first-time homebuyers to buy. The flip side of this is that the high cost of buying a home is causing many young people to postpone marriage, to remain single, or to live with their parents.

Stanley Su has also noticed that parents now accompany more than half of young homebuyers when they look at homes and also help them with their downpayments. "If young people had to depend entirely on their own resources to buy, it would be very, very hard for them," observes Su.

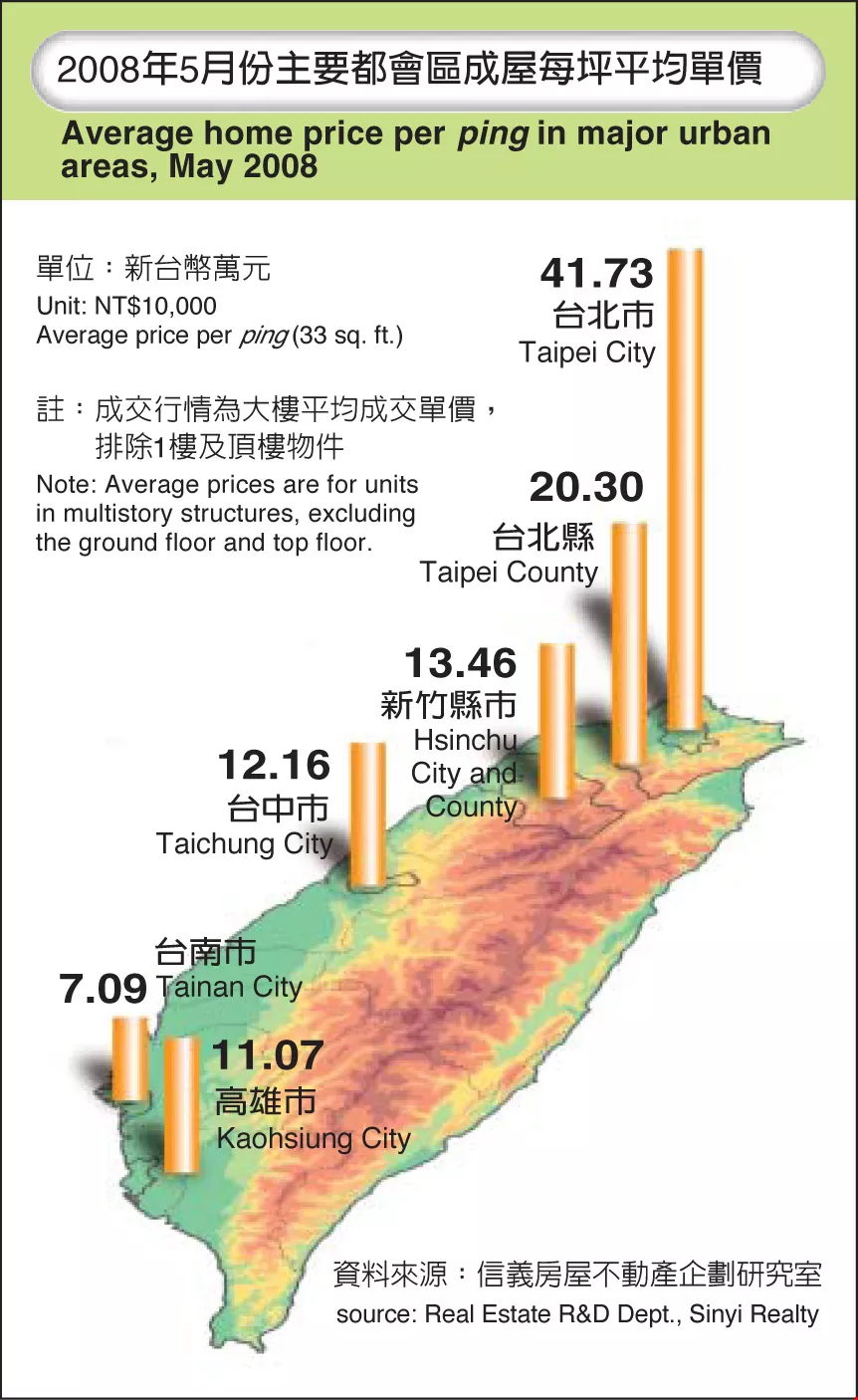

Average home price per ping in major urban areas, May 2008

Peace of mind

Premier Liu's cabinet has therefore put forward a program aimed at alleviating the difficulties young couples face buying a home and enabling them to marry with peace of mind. Under the scheme, people aged 20-39 are eligible to receive a mortgage of up to NT$2 million from the government, and can access the program up to two times. Loans will be offered at zero-percent interest for the first two years of their term, and the government plans to begin implementing the program as early as next year.

The program targets newly married young couples who earn less than Taiwan's median income and are seeking to buy their first home, and people with children who need a larger home. The Ministry of the Interior's Construction and Planning Agency estimates that approximately 40,000 households will qualify every year. The program is expected to save participating households nearly NT$140,000 each in mortgage interest over the interest-free period.

But many scholars have been critical of the timing of the proposal. NCCU's Chang says that with housing prices at historical highs, the government's good intentions are sending the wrong message. He believes the program will just add fuel to the property market fire and encourage young people to fall into the "mortgage slave" trap.

"Young people who make a hasty decision to buy a home in order to get an interest-rate discount, and who then see values plummet when the property bubble bursts, are going to lose a great deal of money," says Chang.

In early June, the MOI rolled out another temporary measure, this one aimed at newlyweds who didn't yet have the means to buy a home. The measure is intended to provide those who are unwilling to gamble on the pricey real-estate market with an equivalent benefit-a rent subsidy of NT$3,000 per month that will have a total value comparable to the NT$140,000 mortgage interest savings.

With prices for gasoline and other goods rising, experts recommend that young people who don't earn a great deal consider renting. Choosing not to buy may offer them fuller, richer lives.

The market will cool

And how will the government plan to slow the unnaturally high rate of increase of Taipei City's real-estate prices? Lin Chu-chia, a professor at NCCU and member of President Ma's economic braintrust, suggests that Taiwan take a look at the US's approach, which involves using property taxes to prevent investment from driving real-estate prices too high. The policy encourages apartments and houses to be used to actually house families rather than as commodities on which the wealthy turn profits.

He says that in New York and Boston, the US's most expensive property markets, property taxes run as high as 1.5% of the market value of the property. Under these circumstances, the owner of a US$100 million house pays US$1.5 million per year in taxes. In Taiwan, on the other hand, property taxes are just 0.15% and are based on the property's declared land value, which amounts to about one-fifth of the market value. In Taiwan, therefore, the owner of a NT$100 million home pays only about NT$30,000 per year in property taxes. The cost of holding a home is so low that investors have an incentive to grab as many as they can. In some cases, wealthy investors are content even to let their properties sit vacant while they wait for their values to climb.

Expanding transportation infrastructure is another means of keeping property prices under control. Chuang Mong-han, an associate professor in Tamkang University's industrial economics department, says that the government ought to build the so-called "Greater Taipei Life Circle," an initiative aimed at tying Keelung, Taoyuan and more distant parts of Taipei County into the rapid transit system, as quickly as possible. Such a project would enable first-time homebuyers who can't afford the pricey downtown Taipei area to purchase less expensive homes at the ends of the rapid transit lines.

Tip 1: Don't buy, rent!

It remains to be seen whether the preferential mortgage interest rates and rent subsidies from the new administration will enable young people to marry with peace of mind. Given the number of uncertainties in the housing market, what kind of plans should young people make to realize their nest-building dreams?

In his bestseller Lower-Middle No Shougeki, Japanese economist Kenichi Ohmae urged young people not to buy into the fantasies of the middle class by pouring their money into the housing market. He argued that in this era of low salaries and high prices young people should save their money rather than spend it on a home, and should shorten their commutes by renting downtown housing near their workplaces. Ohmae believes that this will provide them with fuller, richer lives.

NCCU's Chang Chin-oh strongly approves of the idea that young people should rent instead of buy.

"Thirty-somethings are highly mobile, and haven't yet fully settled into their careers," he says. "If they act too soon in putting all their resources into a home that they can't move out of, they'll limit their opportunities to advance their careers."

"If young people feel they really must buy a home, they should first rent a place near their workplace and accumulate some capital," recommends Tamkang's Chuang Mong-han. "When supply again exceeds demand in the real-estate market, prices will come down. That's when they should think about buying. That's a more intelligent and pragmatic approach than blindly bidding up prices."

Tip 2: Don't overextend

Experts recommend that those who have scraped together enough for a downpayment and have the opportunity to at last become "snails with shells" carefully consider issues before buying, including the size, location, and functionality of the home they need, as well as the size of the mortgage they can afford. After all, they don't want to become slaves to their home and mortgage.

Sinyi's Su says that bank rates for mortgages are still low at about 3.3%. Such mortgages often also include a three-year grace period in which borrowers need only pay the interest on their note, not the principal. Egged on by brokers, many young people are being sucked in by the low payments they'll have for the first few years, forgetting about the much larger payments they'll be making in the future when they have to start repaying the principal as well. As a result, they're jumping into homes and mortgages they can't really afford, and may ultimately have little choice but to declare bankruptcy. In fact, this is one of the underlying causes of the current subprime mortgage crisis in the US.

With the cost of goods rising, the government is likely to raise interest rates to rein in inflation. When they do, homebuyers will face higher mortgage payments. "Young people need to be conservative when they estimate what they can afford or they may end up regretting their decision," says Su.

Su also notes that while young people's salaries are likely to grow over time, childrearing expenses, including daycare and education, are very high. He recommends that homebuyers keep their mortgage payments (interest and principal) to less than 40% of household income to avoid sacrificing too much of their standard of living.

Su also recommends that young people "do a lot of looking, listening, and comparing" before buying. He further suggests that buyers give preference to smaller, older homes, arguing that they can move into something bigger later, when they have more money. This, he says, is the slower, steadier approach to home ownership.

With gasoline prices soaring, those buying less expensive homes far from the urban core must also consider commuting expenses when evaluating affordability. A cheaper place may not be quite the deal they imagine.

In times such as these, when prices are rising and salaries are not, young people must above all avoid falling into the trap of buying a home in a moment of exuberance or for reasons of "face." Whether they ultimately choose to buy or rent, they must carefully evaluate their circumstances and their dreams if they don't want to awaken alone and disoriented.

Ratio of housing prices to income in major cities worldwide (Q3 2007)

| City | Housing price as multiple of income |

| Los Angeles, USA | 11.5 |

| San Francisco, USA | 10.8 |

| Taipei, Taiwan | 10.4(Q1 2008) |

| Honolulu, USA | 10.3 |

| Sidney, Australia | 8.6 |

| Vancouver, Canada | 8.4 |

| London, UK | 7.7 |

| Auckland, New Zealand | 6.9 |

@List.jpg?w=522&h=410&mode=crop&format=webp&quality=80)